Unit 8 Supply and demand: Price-taking and competitive markets

Themes and capstone units

How markets operate when all buyers and sellers are price-takers

- Competition can constrain buyers and sellers to be price-takers.

- The interaction of supply and demand determines a market equilibrium in which both buyers and sellers are price-takers, called a competitive equilibrium.

- Prices and quantities in competitive equilibrium change in response to supply and demand shocks.

- Price-taking behaviour ensures that all gains from trade in the market are exhausted at a competitive equilibrium.

- The model of perfect competition describes idealized conditions under which all buyers and sellers are price-takers.

- Real-world markets are typically not perfectly competitive, but some policy problems can be analysed using this demand and supply model.

- There are important similarities and differences between price-taking and price-setting firms.

Students of American history learn that the defeat of the southern Confederate states in the American Civil War ended slavery in the production of cotton and other crops in that region. There is also an economics lesson in this story.

At the war’s outbreak on 12 April 1861, President Abraham Lincoln ordered the US Navy to blockade the ports of the Confederate states. These states had declared themselves independent of the US to preserve the institution of slavery.

As a result of the naval blockade, the export of US-grown raw cotton to the textile mills of Lancashire in England came to a virtual halt, eliminating three-quarters of the supply of this critical raw material. Sailing at night, a few blockade-running ships evaded Lincoln’s patrols, but 1,500 were destroyed or captured.

- excess demand

- A situation in which the quantity of a good demanded is greater than the quantity supplied at the current price. See also: excess supply.

We will see in this unit that the market price of a good, such as cotton, is determined by the interaction of supply and demand. In the case of raw cotton, the tiny quantities reaching England through the blockade were a dramatic reduction in supply. There was large excess demand—that is to say, at the prevailing price, the quantity of raw cotton demanded exceeded the available supply. As a result, some sellers realized they could profit by raising the price. Eventually, cotton was sold at prices six times higher than before the war, keeping the lucky blockade-runners in business. Consumption of cotton fell to half the prewar level, throwing hundreds of thousands of people who worked in cotton mills out of work.

Mill owners responded. For them, the price rise was an increase in their costs. Some firms failed and left the industry due to the reduction in their profits. Mill owners looked to India to find an alternative to US cotton, greatly increasing the demand for cotton there. The excess demand in the markets for Indian cotton gave some sellers an opportunity to profit by raising prices, resulting in increases in the prices of Indian cotton, which quickly rose almost to match the price of US cotton.

Responding to the higher income now obtainable from growing cotton, Indian farmers abandoned other crops and grew cotton instead. The same occurred wherever cotton could be grown, including Brazil. In Egypt, farmers who rushed to expand the production of cotton in response to the higher prices began employing slaves, captured (like the American slaves that Lincoln was fighting to free) in sub-Saharan Africa.

There was a problem. The only source of cotton that could come close to making up the shortfall from the US was in India. But Indian cotton differed from American cotton, and required an entirely different kind of processing. Within months of the shift to Indian cotton, new machinery was developed to process it.

As the demand for this new equipment soared, firms like Dobson and Barlow, who made textile machinery, saw profits take-off. We know about this firm, because detailed sales records have survived. It responded by increasing production of these new machines and other equipment. No mill could afford to be left behind in the rush to retool, because if it didn’t, it could not use the new raw materials. The result was, in the words of Douglas Farnie, a historian who specialized in the history of cotton production, ‘such an extensive investment of capital that it amounted almost to the creation of a new industry.’

The lesson for economists: Lincoln ordered the blockade, but in what followed, the farmers and sellers who increased the price of cotton were not responding to orders. Neither were the mill owners who cut back the output of textiles and laid off the mill workers, nor were the mill owners desperately searching for new sources of raw material. By ordering new machinery, the mill owners set off a boom in investment and new jobs.

All of these decisions took place over a matter of months, by millions of people, most of whom were total strangers to one another, each seeking to make the best of a totally new economic situation. American cotton was now scarcer, and people responded, from the cotton fields of Maharashtra in India to the Nile delta, to Brazil, and the Lancashire mills.

To understand how the change in the price of cotton transformed the world cotton and textile production system, think about the prices determined by markets as messages. The increase in the price of US cotton shouted: ‘find other sources, and find new technologies appropriate for their use.’ Similarly, when the price of petrol rises, the message to the car driver is: ‘take the train’, which is passed on to the railway operator: ‘there are profits to be made by running more train services’. When the price of electricity goes up, the firm or the family is being told: ‘think about installing photovoltaic cells on the roof.’

In many cases—like the chain of events that began at Lincoln’s desk on 12 April 1861—the messages make sense not only for individual firms and families but also for society: if something has become more expensive then it is likely that more people are demanding it, or the cost of producing it has risen, or both. By finding an alternative, the individual is saving money and conserving society’s resources. This is because, in some conditions, prices provide an accurate measure of the scarcity of a good or service.1

In planned economies, which operated in the Soviet Union and other central and eastern European countries before the 1990s (discussed in Unit 1), messages about how things would be produced are sent deliberately by government experts. They decide what will be produced and at what price it will be sold. The same is true, as we saw in Unit 6, inside large firms like General Motors, where managers (and not prices) determine who does what.

The amazing thing about prices determined by markets is that individuals do not send the messages, but rather the anonymous interaction of sometimes millions of people. And when conditions change—a cheaper way of producing bread, for example—nobody has to change the message (‘put bread instead of potatoes on the table tonight’). A price change results from a change in firms’ costs. The reduced price of bread says it all.

8.1 Buying and selling: Demand and supply

- willingness to pay (WTP)

- An indicator of how much a person values a good, measured by the maximum amount he or she would pay to acquire a unit of the good. See also: willingness to accept.

In Unit 7 we considered the case of a good produced and sold by just one firm. There was one seller with many buyers in the market for that product. In this unit, we look at markets where many buyers and sellers interact, and show how the competitive market price is determined by both the preferences of consumers and the costs of suppliers. When there are many firms producing the same product, each firm’s decisions are affected by the behaviour of competing firms, as well as consumers.

For a simple model of a market with many buyers and sellers, think about the potential for trade in second-hand copies of a recommended textbook for a university economics course. Demand for the book comes from students who are about to begin the course, and they will differ in their willingness to pay (WTP). No one will pay more than the price of a new copy in the campus bookshop. Below that, students’ WTP may depend on how hard they work, how important they think the book is, and on their available resources for buying books.

Often when you buy something you don’t need to think about your exact willingness to pay. You just decide whether to pay the asking price. But WTP is a useful concept for buyers in online auctions, such as eBay.

If you want to bid for an item, one way to do it is to set a maximum bid equal to your WTP, which will be kept secret from other bidders: this article explains how to do it on eBay. eBay will place bids automatically on your behalf until you are the highest bidder, or until your maximum is reached. You will win the auction if, and only if, the highest bid is less than or equal to your WTP.

- willingness to accept (WTA)

- The reservation price of a potential seller, who will be willing to sell a unit only for a price at least this high. See also: willingness to pay.

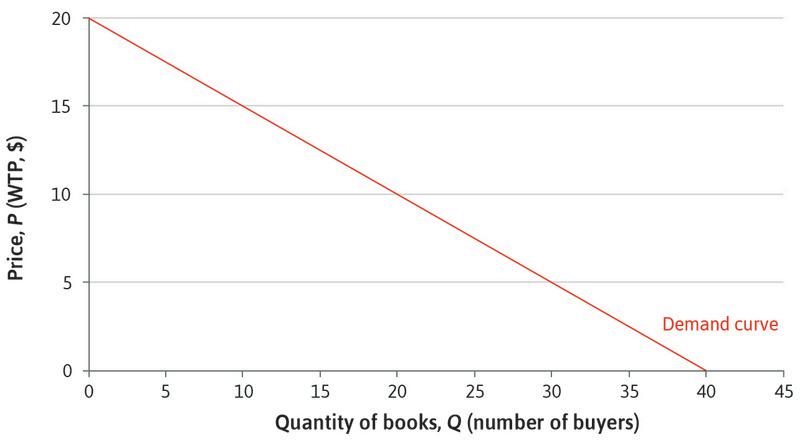

Figure 8.1 shows the demand curve. As in Unit 7, we line up all the consumers in order of willingness to pay, highest first. The first student is willing to pay $20, the 20th $10, and so on. For any price, P, the graph tells you how many students would be willing to buy: it is the number whose WTP is at or above P.

The market demand curve for books.

The market demand curve for books.

Figure 8.1 The market demand curve for books.

The demand curve represents the WTP of buyers; similarly, supply depends on the sellers’ willingness to accept (WTA) money in return for books.

- reservation price

- The lowest price at which someone is willing to sell a good (keeping the good is the potential seller’s reservation option). See also: reservation option.

The supply of second-hand books comes from students who have previously completed the course, who will differ in the amount they are willing to accept—that is, their reservation price. Recall from Unit 5 that Angela was willing to enter into a contract with Bruno only if it gave her at least as much utility as her reservation option (no work and survival rations); here the reservation price of a potential seller represents the value to her of keeping the book, and she will only be willing to sell for a price at least that high. Poorer students (who are keen to sell so that they can afford other books) and those no longer studying economics may have lower reservation prices. Again, online auctions like eBay allow sellers to specify their WTA.

If you sell an item on eBay you can set a reserve price, which will not be disclosed to the bidders. This article explains eBay reserve prices. You are telling eBay that the item should not be sold unless there is a bid at (or above) that price. So the reserve price should correspond to your WTA. If no one bids your WTA, the item will not be sold.

- supply curve

- The curve that shows the number of units of output that would be produced at any given price. For a market, it shows the total quantity that all firms together would produce at any given price.

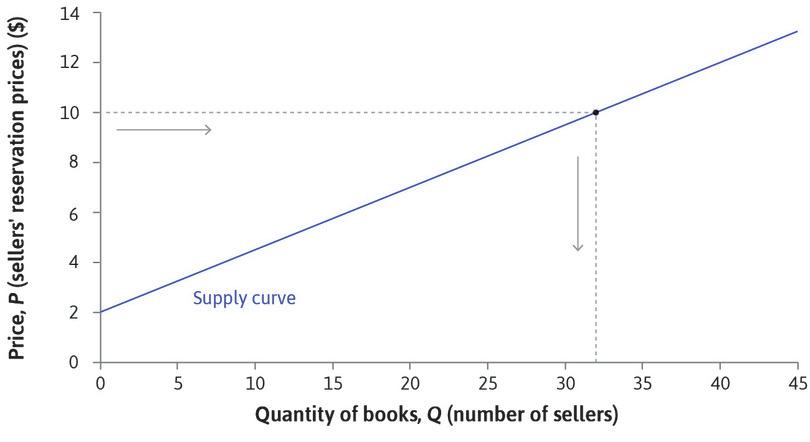

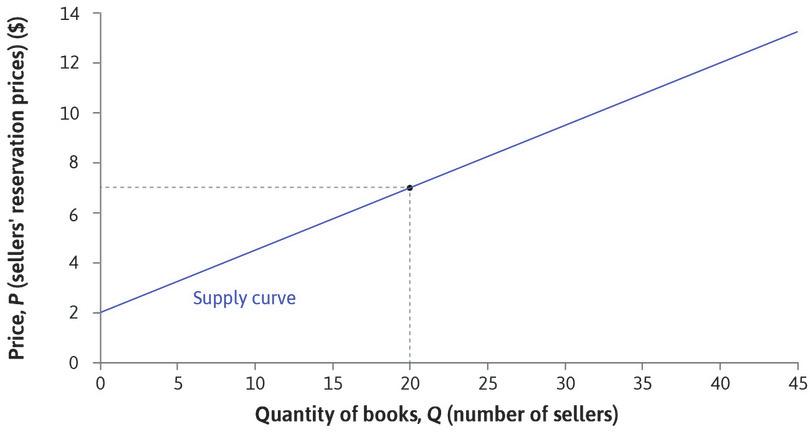

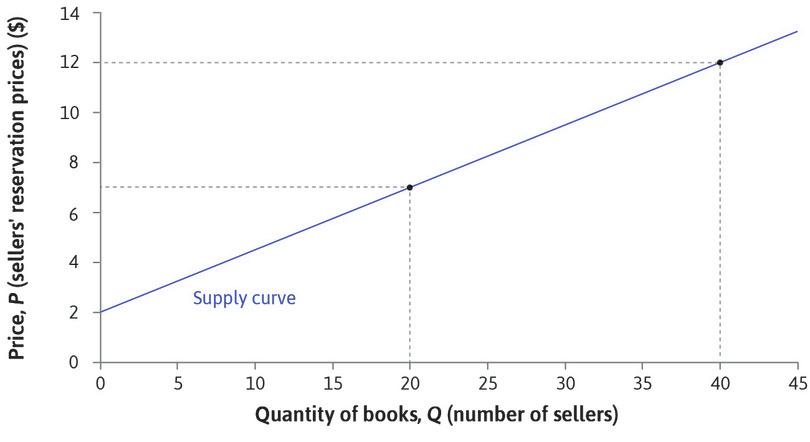

We can draw a supply curve by lining up the sellers in order of their reservation prices (their WTAs): see Figure 8.2. We put the sellers who are most willing to sell—those who have the lowest reservation prices—first, so the graph of reservation prices slopes upward.

The supply curve for books.

The supply curve for books.

Figure 8.2 The supply curve for books.

Reservation price

The first seller has a reservation price of $2, and will sell at any price above that.

Figure 8.2a The first seller has a reservation price of $2, and will sell at any price above that.

The 20th seller

The 20th seller will accept $7 …

Figure 8.2b The 20th seller will accept $7 …

The 40th seller

… and the 40th seller’s reservation price is $12.

Figure 8.2c … and the 40th seller’s reservation price is $12.

Supply curves slope upward

If you choose a particular price, say $10, the graph shows how many books would be supplied (Q) at that price: in this case, it is 32. The supply curve slopes upward: the higher the price, the more students will be willing to sell.

Figure 8.2d If you choose a particular price, say $10, the graph shows how many books would be supplied (Q) at that price: in this case, it is 32. The supply curve slopes upward: the higher the price, the more students will be willing to sell.

For any price, the supply curve shows the number of students willing to sell at that price—that is, the number of books that will be supplied to the market. Notice that we have drawn the supply and demand curves as straight lines for simplicity. In practice they are more likely to be curves, with the exact shape depending on how valuations of the book vary among the students.

Question 8.1 Choose the correct answer(s)

As a student representative, one of your roles is to organize a second-hand textbook market between the current and former first-year students. After a survey, you estimate the demand and supply curves. For example, you estimate that pricing the book at $7 would lead to a supply of 20 books and a demand of 26 books. Which of the following statements is correct?

- The rumour would make the former first-year students less willing to sell. Their WTAs would rise, shifting the supply curve upwards. Equivalently, the number of students willing to supply their book at each price would be lower.

- From the supply curve, we can see that supply would double to 40 if the price were increased to $12.

- The rumour would shift the demand curve downwards.

- The maximum demand attainable is 40 at zero price.

Exercise 8.1 Selling strategies and reservation prices

Consider three possible methods to sell a car that you own:

- Advertise it in the local newspaper.

- Take it to a car auction.

- Offer it to a second-hand car dealer.

- Would your reservation price be the same in each case? Why?

- If you used the first method, would you advertise it at your reservation price?

- Which method do you think would result in the highest sale price?

- Which method would you choose?

8.2 The market and the equilibrium price

What would you expect to happen in the market for this textbook? That will depend on the market institutions that bring buyers and sellers together. If students have to rely on word-of-mouth, then when a buyer finds a seller they can try to negotiate a deal that suits both of them. But each buyer would like to be able to find a seller with a low reservation price, and each seller would like to find a buyer with a high willingness to pay. Before concluding a deal with one trading partner, both parties would like to know about other trading opportunities.

Traditional market institutions often brought many buyers and sellers together in one place. Many of the world’s great cities grew up around marketplaces and bazaars along ancient trading routes such as the Silk Road between China and the Mediterranean. In the Grand Bazaar of Istanbul, one of the largest and oldest covered markets in the world, shops selling carpets, gold, leather, and textiles cluster together in different areas. In medieval towns and cities it was common for makers and sellers of a specific type of good to set up shops close to each other, so customers knew where to find them. The city of London is now a financial centre, but evidence of trades once carried out there can be found in surviving street names: Pudding Lane, Bread Street, Milk Street, Threadneedle Street, Ropemaker Street, Poultry Street, and Silk Street.

With modern communications, sellers can advertise their goods and buyers can more easily find out what is available, and where to buy it. But in some cases it is still convenient for many buyers and sellers to meet each other. Large cities have markets for meat, fish, vegetables or flowers, where buyers can inspect and compare the quality of the produce. In the past, markets for second-hand goods often involved specialist dealers, but nowadays sellers can contact buyers directly through online marketplaces such as eBay. Websites now help students sell textbooks to others in their university.

At the end of the nineteenth century, the economist Alfred Marshall introduced his model of supply and demand using a similar example to our case of second-hand books. Most English towns had a corn exchange (also known as a grain exchange)—a building where farmers met with merchants to sell their grain. Marshall described how the supply curve of grain would be determined by the prices that farmers would be willing to accept, and the demand curve by the willingness to pay of merchants. Then he argued that, although the price ‘may be tossed hither and thither like a shuttlecock’ in the ‘higgling and bargaining’ of the market, it would never be very far from the particular price at which the quantity demanded by merchants was equal to the quantity the farmers would supply.

- excess supply

- A situation in which the quantity of a good supplied is greater than the quantity demanded at the current price. See also: excess demand.

- Nash equilibrium

- A set of strategies, one for each player in the game, such that each player’s strategy is a best response to the strategies chosen by everyone else.

- equilibrium (of a market)

- A state of a market in which there is no tendency for the quantities bought and sold, or the market price, to change, unless there is some change in the underlying costs, preferences, or other determinants of the behaviour of market actors.

Marshall called the price that equated supply and demand the equilibrium price. If the price was above the equilibrium, farmers would want to sell large quantities of grain. But few merchants would want to buy—there would be excess supply. Then, even the merchants who were willing to pay that much would realize that farmers would soon have to lower their prices and would wait until they did. Similarly, if the price was below the equilibrium, sellers would prefer to wait rather than sell at that price. If, at the going price, the amount supplied did not equal the amount demanded, Marshall reasoned that some sellers or buyers could benefit by charging some other price (in modern terminology, we would say that the going price was not a Nash equilibrium). So the price would tend to settle at an equilibrium level, where demand and supply were equated.

Marshall’s argument was based on the assumption that all the grain was of the same quality. His supply and demand model can be applied to markets in which all sellers are selling identical goods, so buyers are equally willing to buy from any seller. If the farmers all had grain of different qualities, they would be more like the sellers of differentiated products in Unit 7.

Great economists Alfred Marshall

- marginal cost

- The effect on total cost of producing one additional unit of output. It corresponds to the slope of the total cost function at each point.

- marginal utility

- The additional utility resulting from a one-unit increase of a given variable.

Alfred Marshall (1842–1924) was a founder—with Léon Walras—of what is termed the neoclassical school of economics. His Principles of Economics, first published in 1890, was the standard introductory textbook for English speaking students for 50 years. An excellent mathematician, Marshall provided new foundations for the analysis of supply and demand by using calculus to formulate the workings of markets and firms, and express key concepts such as marginal costs and marginal utility. The concepts of consumer and producer surplus are also due to Marshall. His conception of economics as an attempt to ‘understand the influences exerted on the quality and tone of a man’s life by the manner in which he earns his livelihood …’ is close to our own definition of the field.2

Sadly, much of the wisdom in Marshall’s text has rarely been taught by his followers. Marshall paid attention to facts. His observation that large firms could produce at lower unit costs than small firms was integral to his thinking, but it never found a place in the neoclassical school. This may be because if the average cost curve is downward-sloping even when firms are very large, there will be a kind of winner-takes-all competition in which a few large firms emerge as winners with the power to set prices, rather than taking the going price as a given. We return to this problem in Unit 12 and Unit 21.

Marshall would also have been distressed that homo economicus (whose existence we questioned in Unit 4) became the main actor in textbooks written by the followers of the neoclassical school. He insisted that:

Ethical forces are among those of which the economist has to take account. Attempts have indeed been made to construct an abstract science with regard to the actions of an economic man who is under no ethical influences and who pursues pecuniary gain … selfishly. But they have not been successful. (Principles of Economics, 1890)

While advancing the use of mathematics in economics, he also cautioned against its misuse. In a letter to A. L. Bowley, a fellow mathematically inclined economist, he explained his own ‘rules’ as follows:

- Use mathematics as a shorthand language, rather than as an engine of inquiry

- Keep to them [that is, stick to the maths] till you have done

- Translate into English

- Then illustrate by examples that are important in real life

- Burn the mathematics

- If you can’t succeed in 4, burn 3: ‘This I do often.’

Marshall was Professor of Political Economy at the University of Cambridge between 1885 and 1908. In 1896 he circulated a pamphlet to the University Senate objecting to a proposal to allow women to be granted degrees. Marshall prevailed and women would wait until 1948 before being granted academic standing at Cambridge on a par with men.

But his work was motivated by a desire to improve the material conditions of working people:

Now at last we are setting ourselves seriously to inquire whether it is necessary that there should be any so called lower classes at all: that is whether there need be large numbers of people doomed from their birth to hard work in order to provide for others the requisites of a refined and cultured life, while they themselves are prevented by their poverty and toil from having any share or part in that life. … The answer depends in a great measure upon facts and inferences, which are within the province of economics; and this is it which gives to economic studies their chief and their highest interest. (Principles of Economics, 1890)

Would Marshall now be satisfied with the contribution that modern economics has made to creating a more just economy?

To apply the supply and demand model to the textbook market, we assume that all the books are identical (although in practice some may be in better condition than others) and that a potential seller can advertise a book for sale by announcing its price on a local website. As at the Corn Exchange, we would expect that most trades would occur at similar prices. Buyers and sellers can easily observe all the advertised prices, so if some books were advertised at $10 and others at $5, buyers would be queuing to pay $5, and these sellers would quickly realize that they could charge more, while no one would want to pay $10 so these sellers would have to lower their price.

- market-clearing price

- At this price there is no excess supply or excess demand. See also: equilibrium.

- equilibrium

- A model outcome that is self-perpetuating. In this case, something of interest does not change unless an outside or external force is introduced that alters the model’s description of the situation.

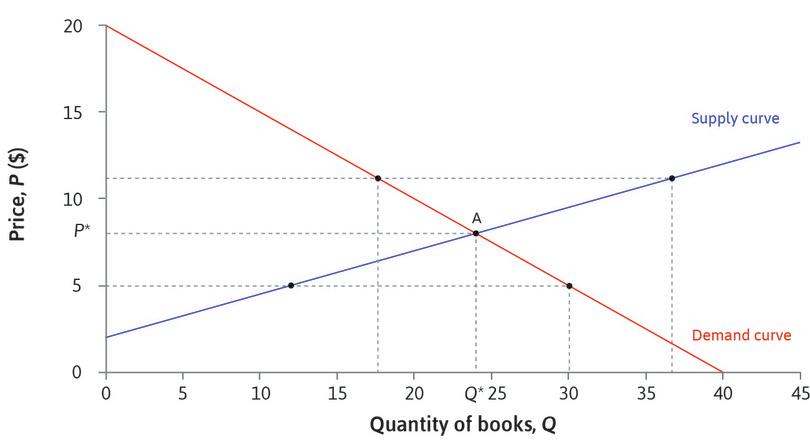

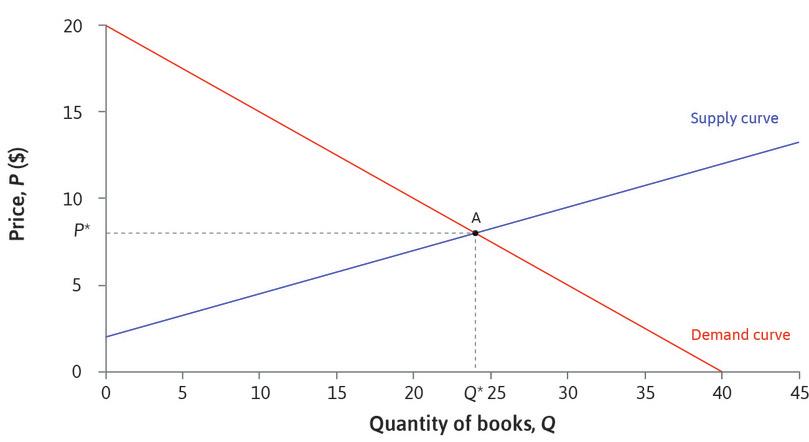

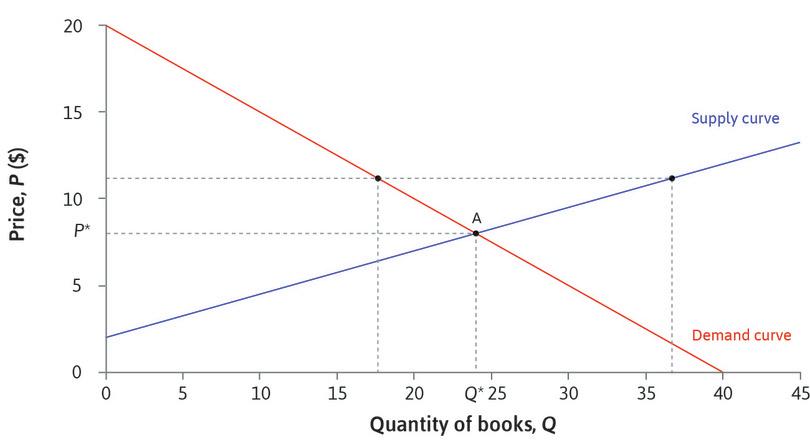

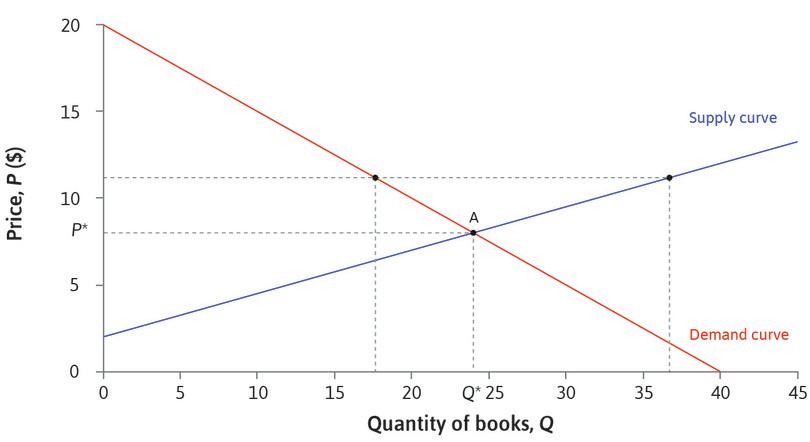

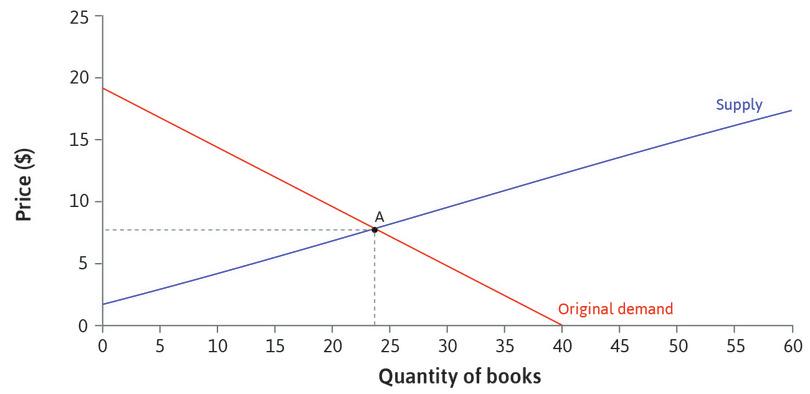

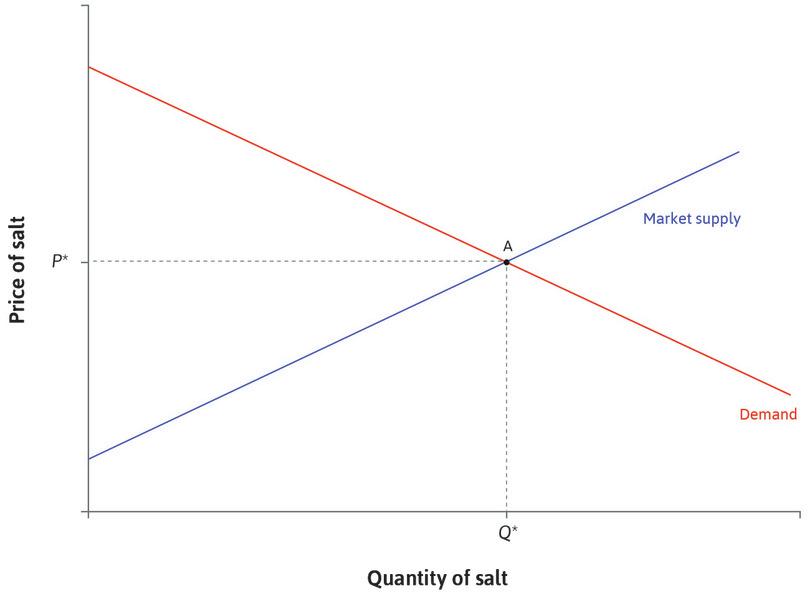

We can find the equilibrium price by drawing the supply and demand curves on one diagram, as in Figure 8.3. At a price P* = $8, the supply of books is equal to demand: 24 buyers are willing to pay $8, and 24 sellers are willing to sell. The equilibrium quantity is Q* = 24.

Equilibrium in the market for second-hand books.

Equilibrium in the market for second-hand books.

Figure 8.3 Equilibrium in the market for second-hand books.

Supply and demand

We find the equilibrium by drawing the supply and demand curves in the same diagram.

Figure 8.3a We find the equilibrium by drawing the supply and demand curves in the same diagram.

The market-clearing price

At a price P* = $8, the quantity supplied is equal to the quantity demanded: Q* = 24. The market is in equilibrium. We say that the market clears at a price of $8.

Figure 8.3b At a price P* = $8, the quantity supplied is equal to the quantity demanded: Q* = 24. The market is in equilibrium. We say that the market clears at a price of $8.

A price above the equilibrium price

At a price greater than $8 more students would wish to sell, but not all of them would find buyers. There would be excess supply, so these sellers would want to lower their price.

Figure 8.3c At a price greater than $8 more students would wish to sell, but not all of them would find buyers. There would be excess supply, so these sellers would want to lower their price.

A price below the equilibrium price

At a price less than $8, there would be more buyers than sellers—excess demand—so sellers could raise their prices. Only at $8 is there no tendency for change.

Figure 8.3d At a price less than $8, there would be more buyers than sellers—excess demand—so sellers could raise their prices. Only at $8 is there no tendency for change.

The market-clearing price is $8—that is, supply is equal to demand at this price, so all buyers who want to buy and all sellers who want to sell can do so. The market is in equilibrium. In everyday language, something is in equilibrium if the forces acting on it are in balance, so that it remains still. Remember Fisher’s hydraulic model of price determination from Unit 2: changes in the economy caused water to flow through the apparatus until it reached an equilibrium, with no further tendency for prices to change. We say that a market is in equilibrium if the actions of buyers and sellers have no tendency to change the price or the quantities bought and sold, unless there is a change in market conditions such as the numbers of potential buyers and sellers, and how much they value the good. At the equilibrium price for textbooks, all those who wish to buy or sell are able to do so, so there is no tendency for change.

Not all online markets for books are in competitive equilibrium. In one case when the conditions for equilibrium were not met, automatic price-setting algorithms raised the price of a book to $23 million! Michael Eisen, a biologist, noticed a classic but out-of-print text, The Making of a Fly, was listed for sale on Amazon by two reputable sellers, with prices starting at $1,730,045.91 (+$3.99 shipping). He watched over the next week as the prices rose rapidly, eventually peaking at $23,698,655.93, before dropping to $106.23. Eisen explains why in his blog.3

Price-taking

Will the market always be in equilibrium? As we have seen, Marshall argued that prices would not deviate far from the equilibrium level, because people would want to change their prices if there were excess supply or demand. In this unit, we study competitive market equilibria. In Unit 11 we will look at when and how prices change when the market is not in equilibrium.

- price-taker

- Characteristic of producers and consumers who cannot benefit by offering or asking any price other than the market price in the equilibrium of a competitive market. They have no power to influence the market price.

In the market equilibrium that we have described for the textbook, individual students have to accept the prevailing price in the market, determined by the supply and demand curves. No one would trade with a student asking a higher price or offering a lower one, because anyone could find an alternative seller or buyer with a better price. The participants in this market are price-takers, because there is sufficient competition from other buyers and sellers so the best they can do is to trade at the same price. Any buyer or seller is of course free to choose a different price, but they cannot benefit by doing so.

We have seen examples where market participants do not behave as price-takers: the producer of a differentiated product can set its own price because it has no close competitors. Notice, however, that although the sellers of differentiated products are price-setters, the buyers in Unit 7 were price-takers. Since there are so many consumers wanting to buy breakfast cereals, an individual consumer has no power to negotiate a more advantageous deal, but simply has to accept the price that all other consumers are paying.

In this unit, we study market equilibria where both buyers and sellers are price-takers. We expect to see price-taking on both sides of the market where there are many sellers selling the identical goods, and many buyers wishing to purchase them. Sellers are forced to be price-takers by the presence of other sellers, as well as buyers who always choose the seller with the lowest price. If a seller tried to set a higher price, buyers would simply go elsewhere.

- competitive equilibrium

- A market outcome in which all buyers and sellers are price-takers, and at the prevailing market price, the quantity supplied is equal to the quantity demanded.

Similarly buyers are price-takers when there are plenty of other buyers, and sellers willing to sell to whoever will pay the highest price. On both sides of the market, competition eliminates bargaining power. We will describe the equilibrium in such a market as a competitive equilibrium.

A competitive market equilibrium is a Nash equilibrium, because given what all other actors are doing (trading at the equilibrium price), no actor can do better than to continue what he or she is doing (also trading at the equilibrium price).

Exercise 8.2 Price-takers

Think about some of the goods you buy: perhaps different kinds of food, clothes, transport tickets, or electronic goods.

- Are there many sellers of these goods?

- Do you try to find the lowest price in each case?

- If not, why not?

- For which goods would price be your main criterion?

- Use your answers to help you decide whether the sellers of these goods are price-takers. Are there goods for which you, as a buyer, are not a price-taker?

Question 8.2 Choose the correct answer(s)

The diagram shows the demand and the supply curves for a textbook. The curves intersect at (Q, P) = (24, 8). Which of the following is correct?

- At $10 the price is above the equilibrium price of $8, and there is an excess supply of books.

- At $8, all buyers with a WTP at $8 or above can be matched with all sellers with a WTA of $8 or less. If one of these sellers raised their price to $9, the buyer could find another seller willing to accept less.

- At $8, the quantity demanded is equal to the quantity supplied—that is, the market clears.

- The maximum level of demand is 40, but 16 of these will be unfulfilled as their willingness-to-pay is below the market clearing price of $8.

8.3 Price-taking firms

In the second-hand textbook example, both buyers and sellers are individual consumers. Now we look at markets where the sellers are firms. We know from Unit 7 how firms choose their price and quantity when producing differentiated goods, and we saw that if other firms made similar products, their choice of price would be restricted (the demand curve for their own product would be almost flat) because raising the price would cause consumers to switch to other similar brands.

If there are many firms producing identical products, and consumers can easily switch from one firm to another, then firms will be price-takers in equilibrium. They will be unable to benefit from attempting to trade at a price different from the prevailing price.

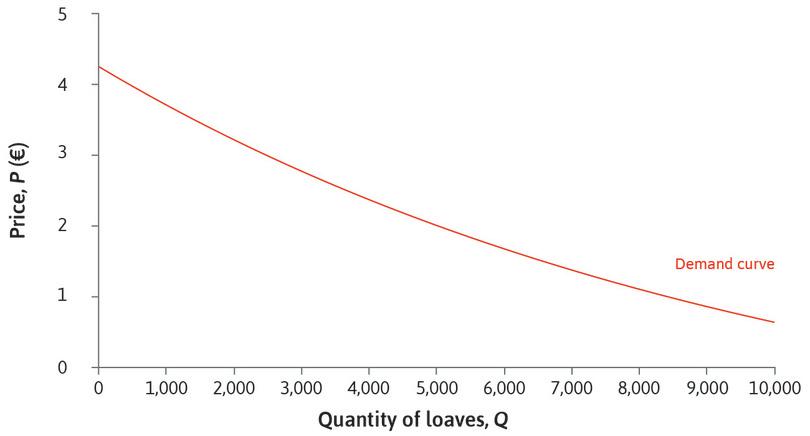

To see how price-taking firms behave, consider a city where many small bakeries produce bread and sell it direct to consumers. Figure 8.4 shows what the market demand curve (the total daily demand for bread of all consumers in the city) might look like. It is downward-sloping as usual because at higher prices, fewer consumers will be willing to buy.

The market demand curve for bread.

The market demand curve for bread.

Figure 8.4 The market demand curve for bread.

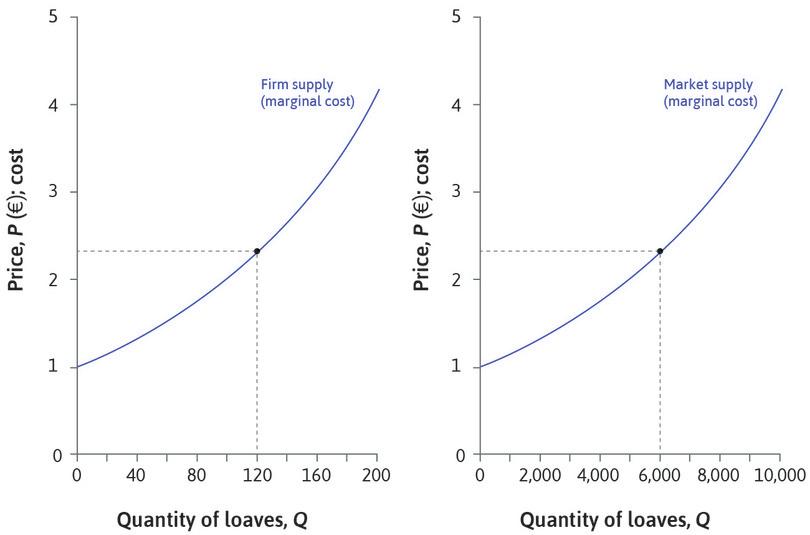

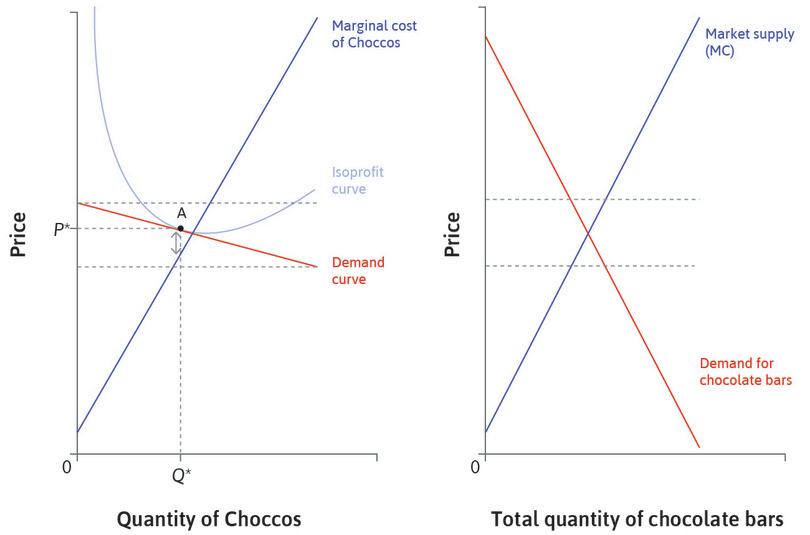

Suppose that you are the owner of one small bakery. You have to decide what price to charge and how many loaves to produce each morning. Suppose that neighbouring bakeries are selling loaves identical to yours at €2.35. This is the prevailing market price, and you will not be able to sell loaves at a higher price than other bakeries, because no one would buy—you are a price-taker.

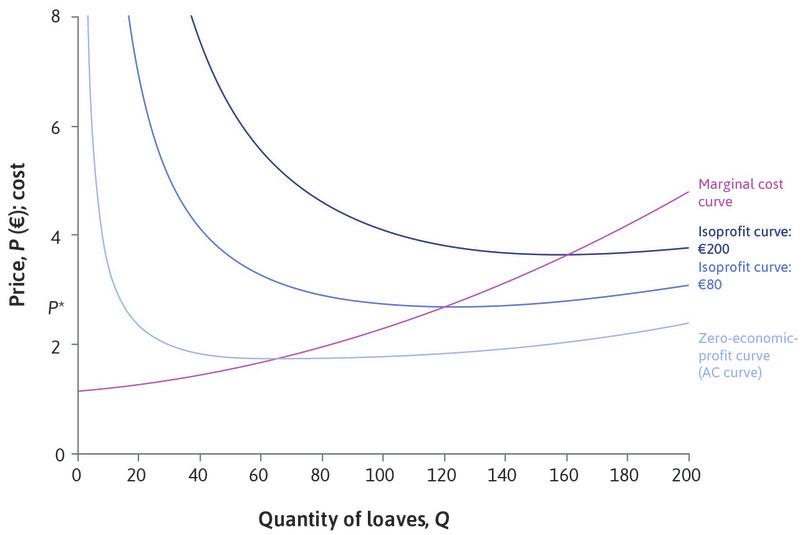

Your marginal costs increase with your output of bread. When the quantity is small, the marginal cost is low, close to €1: having installed mixers, ovens and other equipment, and employed a baker, the additional cost to produce a loaf of bread is relatively small, but the average cost of a loaf is high. As the number of loaves per day increases, the average cost falls, but marginal costs begin to rise gradually because you have to employ extra staff and use equipment more intensively. At higher quantities the marginal cost is above the average cost; then average costs rise again.

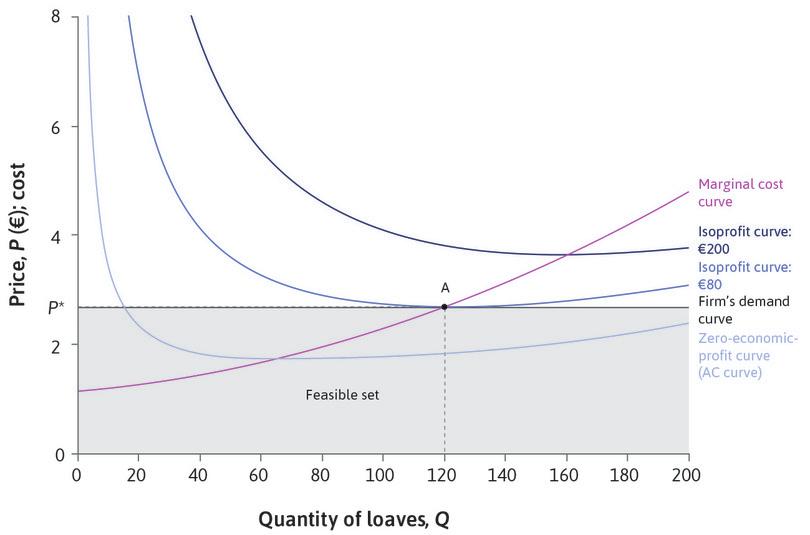

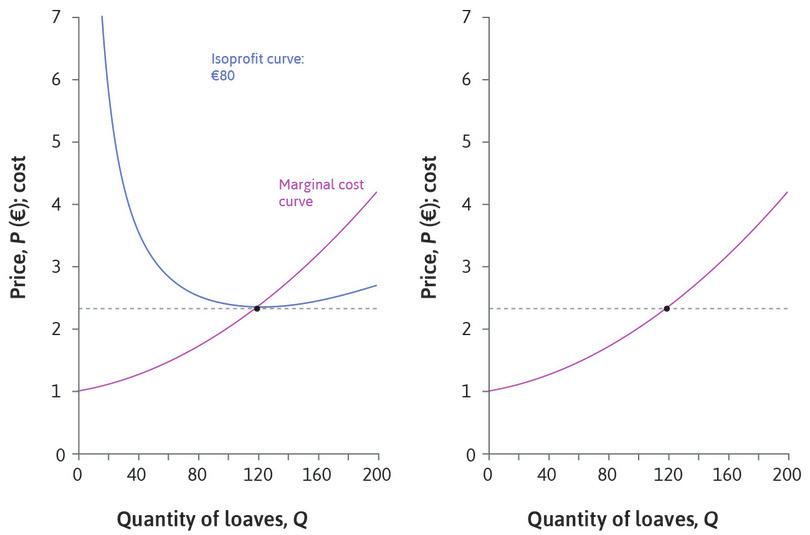

The marginal and average cost curves are drawn in Figure 8.5. As in Unit 7, costs include the opportunity cost of capital. If price were equal to average cost (P = AC), your economic profit would be zero. You, the owner, would obtain a normal return on your capital. So the average cost curve (the leftmost curve in Figure 8.5) is the zero-economic-profit curve. The isoprofit curves show price and quantity combinations at which you would receive higher levels of profit. As we explained in Unit 7, isoprofit curves slope downwards where price is above marginal cost, and upwards where price is below marginal cost, so the marginal cost curve passes through the lowest point on each isoprofit curve. If price is above marginal cost, total profits can remain unchanged only if a larger quantity is sold for a lower price. Similarly, if price is below marginal cost, total profits can remain unchanged only if a larger quantity is sold for a higher price.

Figure 8.5 demonstrates how to make your decision. Like the firms in Unit 7, you face a constrained optimization problem. You want to find the point of maximum profit in your feasible set.

The profit-maximizing price and quantity for a bakery.

The profit-maximizing price and quantity for a bakery.

Figure 8.5 The profit-maximizing price and quantity for a bakery.

Marginal cost and isoprofit curves

The bakery has an increasing MC curve. On the AC curve, profit is zero. When MC > AC, the AC curve slopes upward. The other isoprofit curves represent higher levels of profit, and MC passes through the lowest points of all the isoprofit curves.

Figure 8.5a The bakery has an increasing MC curve. On the AC curve, profit is zero. When MC > AC, the AC curve slopes upward. The other isoprofit curves represent higher levels of profit, and MC passes through the lowest points of all the isoprofit curves.

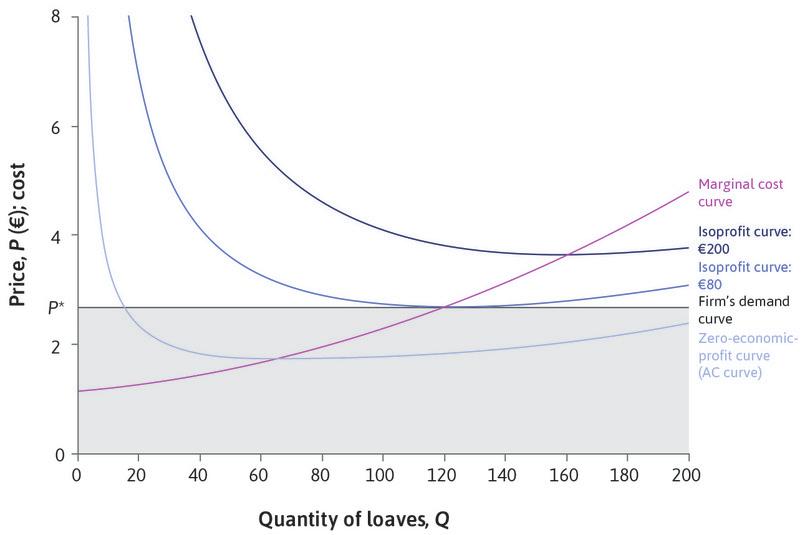

Price-taking

The bakery is a price-taker. The market price is P* = €2.35. If you choose a higher price, customers will go to other bakeries. Your feasible set of prices and quantities is the area below the horizontal line at P*.

Figure 8.5b The bakery is a price-taker. The market price is P* = €2.35. If you choose a higher price, customers will go to other bakeries. Your feasible set of prices and quantities is the area below the horizontal line at P*.

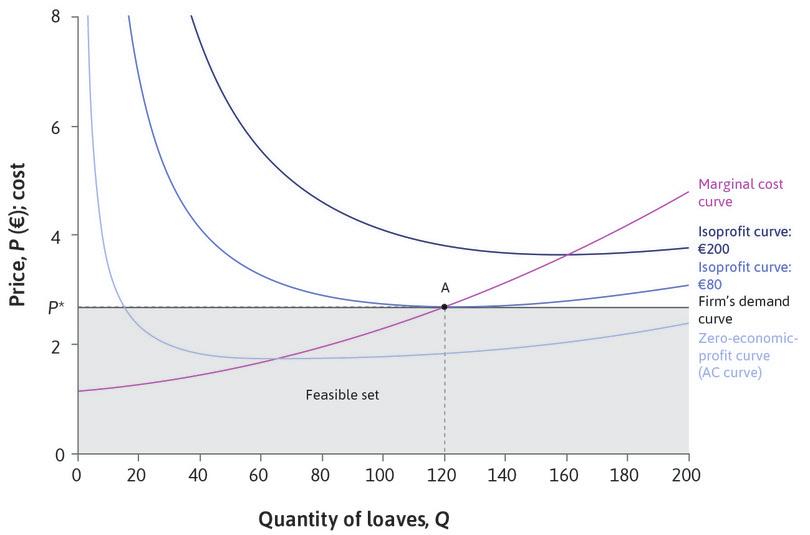

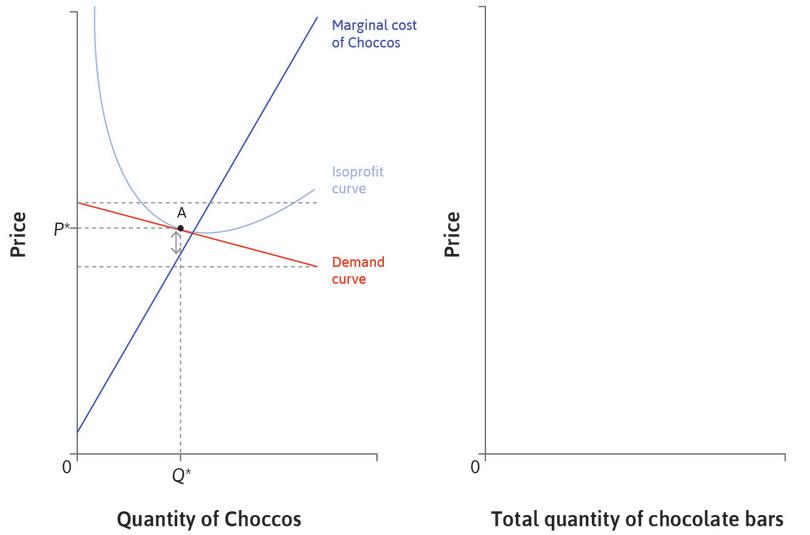

The profit-maximizing price

The point of highest profit in the feasible set is point A, where the €80 isoprofit curve is tangent to the feasible set. You should make 120 loaves per day, and sell them at the market price, €2.35 each. You will make €80 of profit per day in addition to normal profits.

Figure 8.5c The point of highest profit in the feasible set is point A, where the €80 isoprofit curve is tangent to the feasible set. You should make 120 loaves per day, and sell them at the market price, €2.35 each. You will make €80 of profit per day in addition to normal profits.

The profit-maximizing quantity

Your profit-maximizing quantity, Q* = 120, is found at the point where P* = MC: the marginal cost of the 120th loaf is equal to the market price.

Figure 8.5d Your profit-maximizing quantity, Q* = 120, is found at the point where P* = MC: the marginal cost of the 120th loaf is equal to the market price.

Because you are a price-taker, the feasible set is all points where price is less than or equal to €2.35, the market price. Your optimal choice is P* = €2.35 and Q* = 120, where the isoprofit curve is tangent to the feasible set. The problem looks similar to the one for Beautiful Cars in Unit 7, except that for a price-taker, the demand curve is completely flat. For your bakery, it is not the market demand curve in Figure 8.4 that affects your own demand, it is the price charged by your competitors. This is why the horizontal line at P* in Figure 8.5 is labelled as the firm’s demand curve. If you charge more than P*, your demand will be zero, but at P* or less you can sell as many loaves as you like.

Figure 8.5 illustrates a very important characteristic of price-taking firms. They choose to produce a quantity at which the marginal cost is equal to the market price (MC = P*). This is always true. For a price-taking firm, the demand curve for its own output is a horizontal line at the market price, so maximum profit is achieved at a point on the demand curve where the isoprofit curve is horizontal. And we know from Unit 7 that where isoprofit curves are horizontal, the price is equal to the marginal cost.

Another way to understand why a price-taking firm produces at the level of output where MC = P* is to think about what would happen to its profits if it deviated from this point. If the firm were to increase output to a level where MC > P*, the last unit would cost more than P* to make, so the firm would make a loss on this unit and could make higher profits by reducing output. If it were to produce where MC < P*, it could produce at least one more unit and sell it at a profit. Therefore it should raise output as far as the point where MC = P*. This is where profits are maximized.

Price-taking firm

A price-taking firm maximizes profit by choosing a quantity where the marginal cost is equal to the market price (MC = P*) and selling at the market price P*.

This is an important result that you should remember, but you need to be careful with it. When we make statements like ‘for a price-taking firm, price equals marginal cost’, we do not mean that the firm chooses a price equal to its marginal cost. Instead, we mean the opposite: the firm accepts the market price, and chooses its quantity so that the marginal cost is equal to that price.

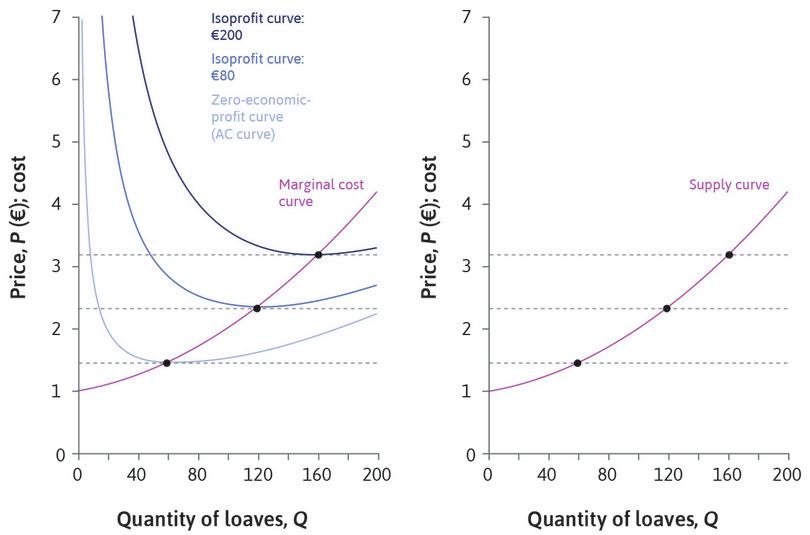

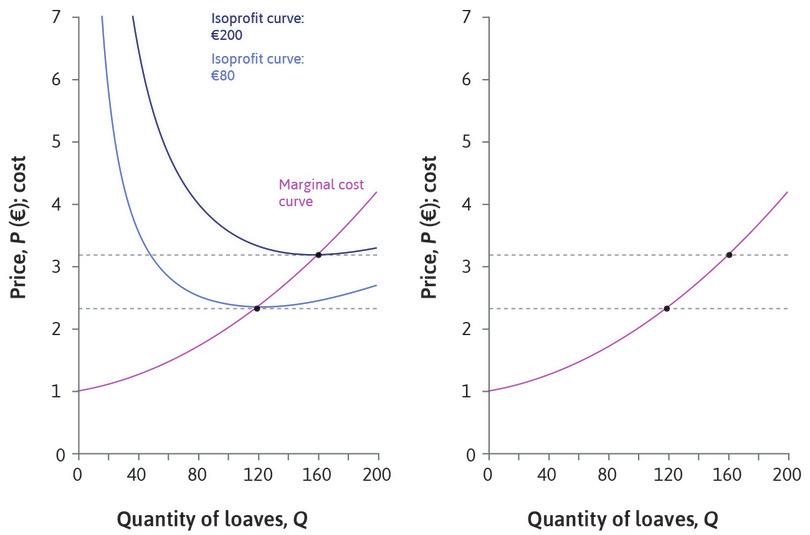

Put yourself in the position of the bakery owner again. What would you do if the market price changed? Figure 8.6 demonstrates that as prices change you would choose different points on the marginal cost curve.

The firm’s supply curve.

The firm’s supply curve.

Figure 8.6 The firm’s supply curve.

A change in price

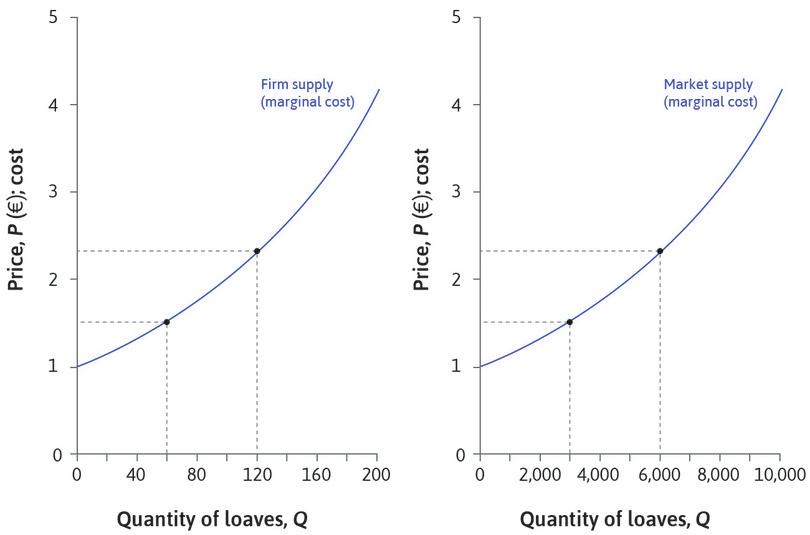

When the market price is €2.35, you supply 120 loaves. What would you do if the price changed?

Figure 8.6a When the market price is €2.35, you supply 120 loaves. What would you do if the price changed?

If the price rises

If P* were to rise to €3.20, you could reach a higher isoprofit curve. To maximize profit you should produce 163 loaves per day.

Figure 8.6b If P* were to rise to €3.20, you could reach a higher isoprofit curve. To maximize profit you should produce 163 loaves per day.

If the price falls

If the price falls to €1.52 you could reach only the lightest blue curve. Your best choice would be 66 loaves, and your economic profit would be zero.

Figure 8.6c If the price falls to €1.52 you could reach only the lightest blue curve. Your best choice would be 66 loaves, and your economic profit would be zero.

The marginal cost curve is the supply curve

In each case, you choose the point on your marginal cost curve where MC = market price. Your marginal cost curve is your supply curve.

Figure 8.6d In each case, you choose the point on your marginal cost curve where MC = market price. Your marginal cost curve is your supply curve.

For a price-taking firm, the marginal cost curve is the supply curve: for each price it shows the profit-maximizing quantity—that is, the quantity that the firm will choose to supply.

Notice, however, that if the price fell below €1.52 you would be making a loss. The supply curve shows how many loaves you should produce to maximize profit, but when the price is this low, the economic profit is nevertheless negative. On the supply curve, you would be minimizing your loss. If this happened, you would have to decide whether it was worth continuing to produce bread. Your decision depends on what you expect to happen in the future:

- If you expect market conditions to remain bad, it might be best to sell up and leave the market—you could obtain a better return on your capital elsewhere.

- If you expect the price to rise soon, you might be willing to incur some short-term losses, and it might be worth continuing to produce bread if the revenue helped you to cover the costs of maintaining your premises and retaining staff.

Question 8.3 Choose the correct answer(s)

Figure 8.5 shows a price-taking bakery’s marginal and average cost curves, and its isoprofit curves. The market price for bread is P*= €2.35. Which of the following statements is correct?

- The firm’s demand curve is horizontal. Its supply curve is upward sloping.

- At €2.35 the firm maximizes profit at point A, where it supplies 120 loaves.

- At each price, the firm will choose a point on the highest isoprofit curve attainable, which will be a point on the marginal cost curve.

- At each price, the firm maximizes profit by choosing the corresponding quantity on the marginal cost curve. So the marginal cost curve is its supply curve.

8.4 Market supply and equilibrium

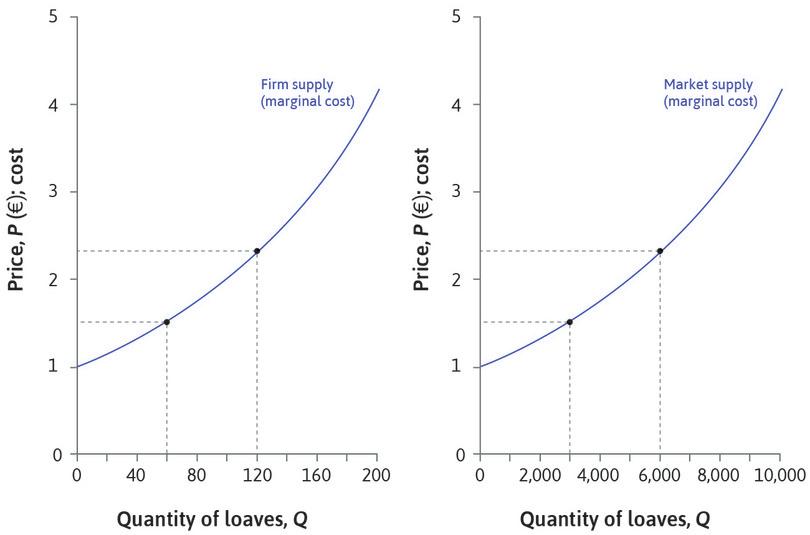

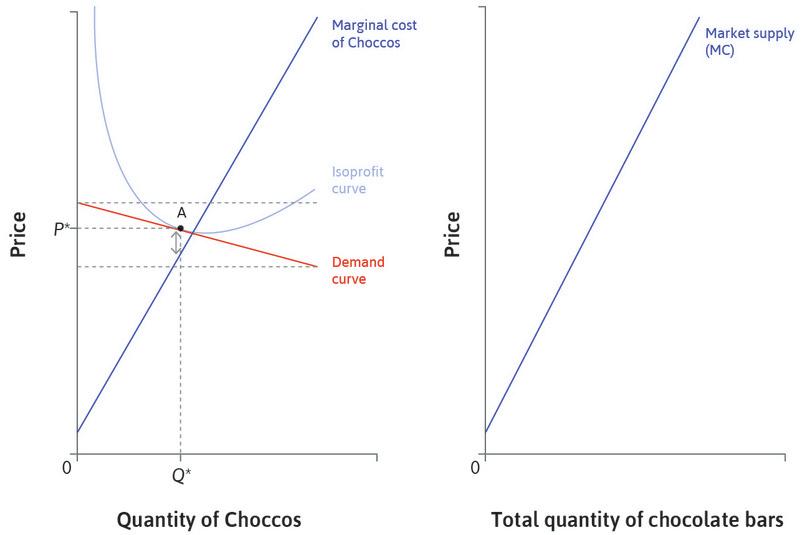

The market for bread in the city has many consumers and many bakeries. Let’s suppose there are 50 bakeries. Each one has a supply curve corresponding to its own marginal cost curve, so we know how much it will supply at any given market price. To find the market supply curve, we just add up the total amount that all the bakeries will supply at each price.

Figure 8.7 shows how this works if all the bakeries have the same cost functions. We work out how much one bakery would supply at a given price, then multiply by 50 to find total market supply at that price.

The firm and market supply curves.

The firm and market supply curves.

Figure 8.7 The firm and market supply curves.

The firm’s supply curve

There are 50 bakeries, all with the same cost functions. If the market price is €2.35, each bakery will produce 120 loaves.

Figure 8.7a There are 50 bakeries, all with the same cost functions. If the market price is €2.35, each bakery will produce 120 loaves.

The market supply curve

When P = €2.35, each bakery supplies 120 loaves, and the market supply is 50 × 120 = 6,000 loaves.

Figure 8.7b When P = €2.35, each bakery supplies 120 loaves, and the market supply is 50 × 120 = 6,000 loaves.

Firm and market supply curves look similar

At a price of €1.52 they each supply 66 loaves, and market supply is 3,300. The market supply curve looks like the firm’s supply curve, but the scale on the horizontal axis is different.

Figure 8.7c At a price of €1.52 they each supply 66 loaves, and market supply is 3,300. The market supply curve looks like the firm’s supply curve, but the scale on the horizontal axis is different.

What if different firms had different costs?

If the bakeries had different cost functions, then at a price of €2.35 some bakeries would produce more loaves than others, but we could still add them together to find market supply.

Figure 8.7d If the bakeries had different cost functions, then at a price of €2.35 some bakeries would produce more loaves than others, but we could still add them together to find market supply.

The market supply curve shows the total quantity that all the bakeries together would produce at any given price. It also represents the marginal cost of producing a loaf, just as the firm’s supply curve does. For example, if the market price is €2.75, total market supply is 7,000. For every bakery, the marginal cost—the cost of producing one more loaf—is €2.75. And that means that the cost of producing the 7,001st loaf in the market is €2.75, whichever firm produces it. So the market supply curve is the market’s marginal cost curve.

Leibniz: Market supply curve

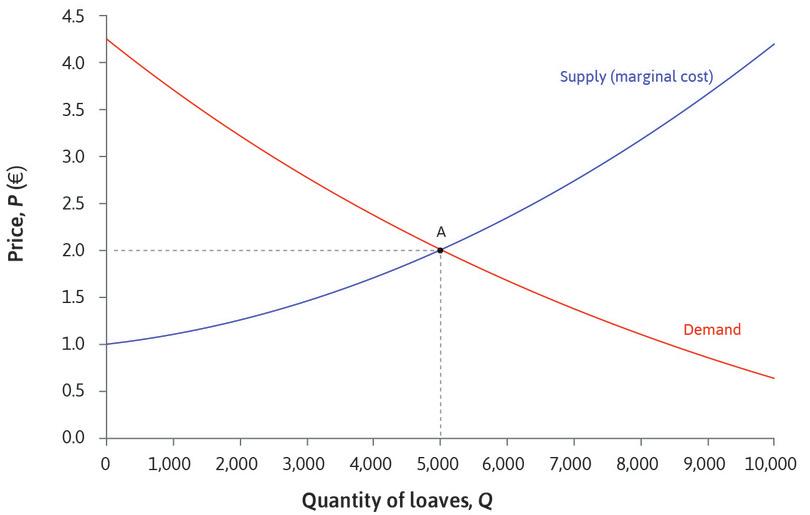

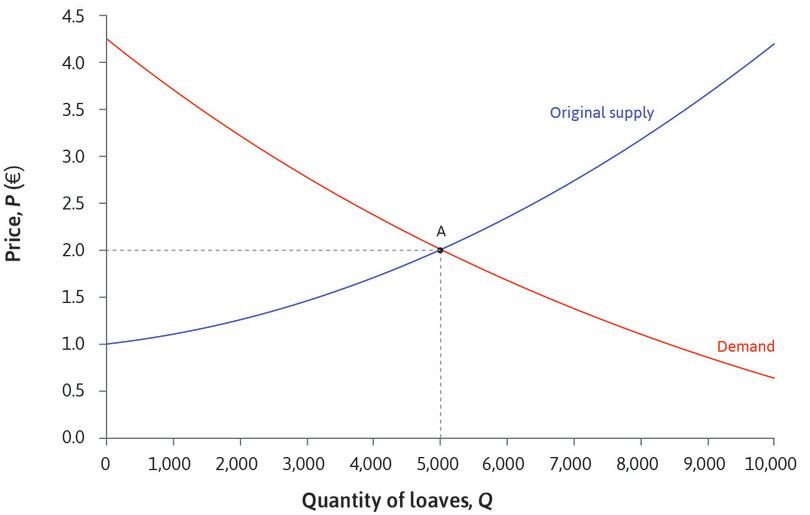

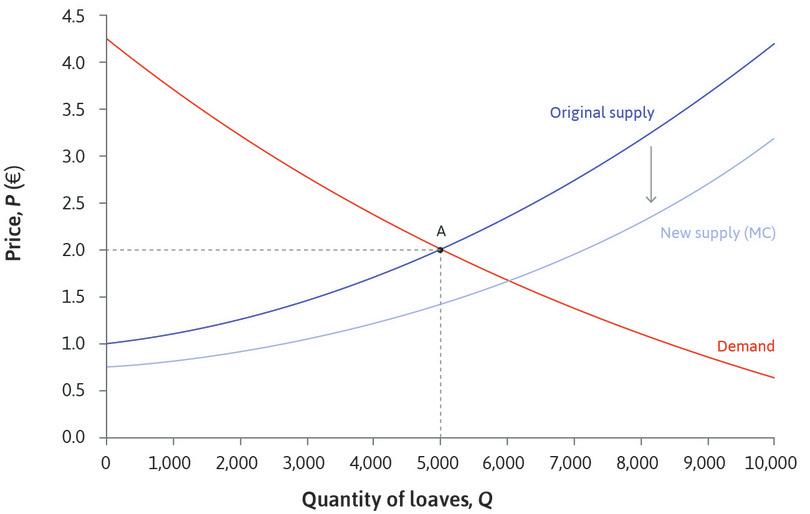

Now we know both the demand curve (Figure 8.4) and the supply curve (Figure 8.7) for the bread market as a whole. Figure 8.8 shows that the equilibrium price is exactly €2.00. At this price, the market clears: consumers demand 5,000 loaves per day, and firms supply 5,000 loaves per day.

Equilibrium in the market for bread.

Equilibrium in the market for bread.

Figure 8.8 Equilibrium in the market for bread.

Leibniz: Market equilibrium

In the market equilibrium, each bakery is producing on its marginal cost curve, at the point where its marginal cost is €2.00. If you look back to the isoprofit curves in Figure 8.6, you will see that the firm is above its average cost curve, the isoprofit curve where economic profits are zero. So the owners of the bakeries are receiving economic rents (profit in excess of normal profit). Whenever there are economic rents, there is an opportunity for someone to benefit by taking an action. In this case, we might expect the economic rents to attract other bakeries into the market. We will see presently how this would affect the market equilibrium.

Question 8.4 Choose the correct answer(s)

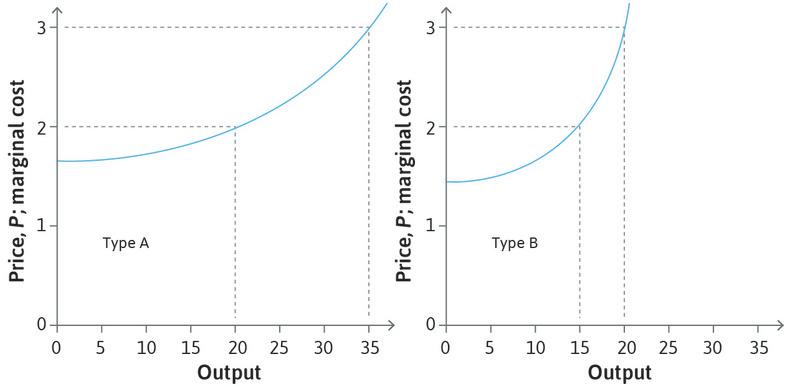

There are two different types of producers of a good in an industry where firms are price-takers. The marginal cost curves of the two types are given below:

Type A is more efficient than Type B: for example, as shown, at the output of 20 units, the Type A firms have a marginal cost of $2, as opposed to a marginal cost of $3 for the Type B firms. There are 10 Type A firms and 8 Type B firms in the market. Which of the following statements is correct?

- At $2, type A firms supply 20 units and type B firms supply 15 units. So the market supply is (10 × 20) + (8 × 15) = 320.

- At $3, type A firms supply 35 units and type B firms supply 20 units. So the market supply is (10 × 35) + (8 × 20) = 510.

- Both types will be producing at the marginal cost of $2. Therefore the market marginal cost is $2, irrespective of which firm produces the extra unit.

- The market’s marginal cost curve is its supply curve. We can calculate supply at each price as in (a) and (b).

8.5 Competitive equilibrium: Gains from trade, allocation, and distribution

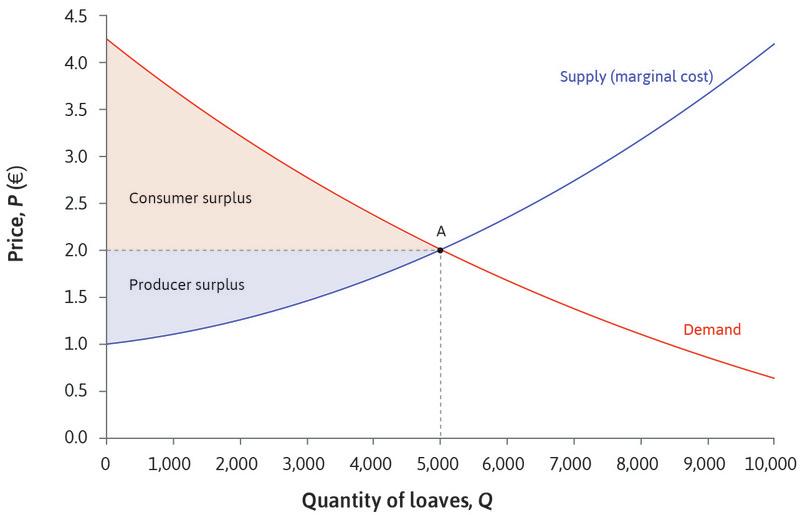

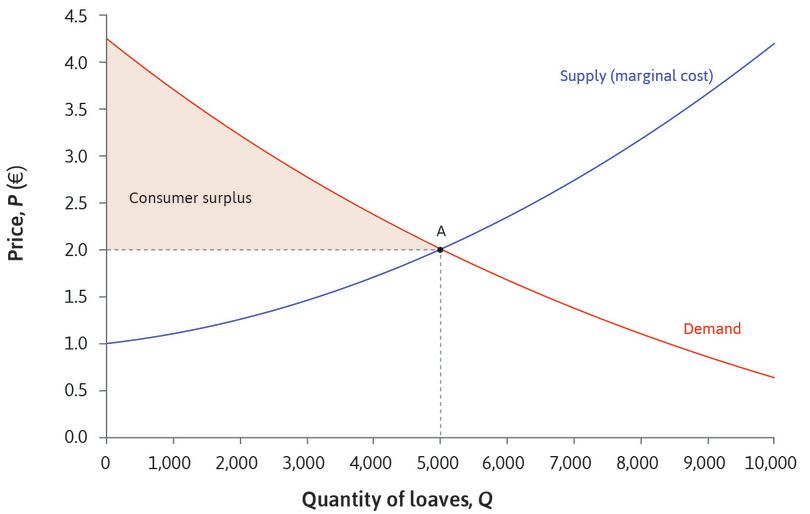

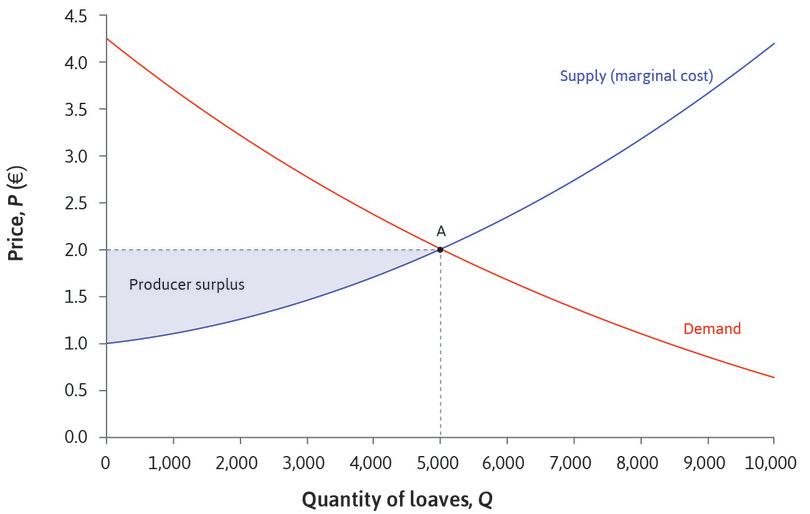

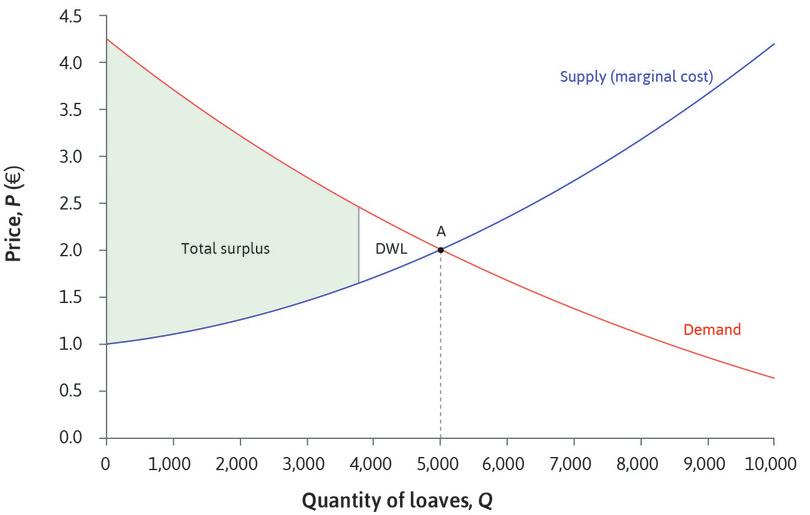

Buyers and sellers of bread voluntarily engage in trade because both benefit. Their mutual benefits from the equilibrium allocation can be measured by the consumer and producer surpluses introduced in Unit 7. Any buyer whose willingness to pay for a good is higher than the market price receives a surplus: the difference between the WTP and the price paid. Similarly, if the marginal cost of producing a good is below the market price, the producer receives a surplus. Figure 8.9a shows how to calculate the total surplus (the gains from trade) at the competitive equilibrium in the market for bread, in the same way as we did for the markets in Unit 7.

Equilibrium in the bread market: Gains from trade.

Equilibrium in the bread market: Gains from trade.

Figure 8.9a Equilibrium in the bread market: Gains from trade.

The consumer surplus

At the equilibrium price of €2 in the bread market, a consumer who is willing to pay €3.50 obtains a surplus of €1.50.

Figure 8.9a-a At the equilibrium price of €2 in the bread market, a consumer who is willing to pay €3.50 obtains a surplus of €1.50.

Total consumer surplus

The shaded area above €2 shows total consumer surplus—the sum of all the buyers’ gains from trade.

Figure 8.9a-b The shaded area above €2 shows total consumer surplus—the sum of all the buyers’ gains from trade.

The producer surplus

Remember from Unit 7 that the producer’s surplus on a unit of output is the difference between the price at which it is sold, and the marginal cost of producing it. The marginal cost of the 2,000th loaf is €1.25; since it is sold for €2, the producer obtains a surplus of €0.75.

Figure 8.9a-c Remember from Unit 7 that the producer’s surplus on a unit of output is the difference between the price at which it is sold, and the marginal cost of producing it. The marginal cost of the 2,000th loaf is €1.25; since it is sold for €2, the producer obtains a surplus of €0.75.

Total producer surplus

The shaded area below €2 is the sum of the bakeries’ surpluses on every loaf that they produce. The whole shaded area shows the sum of all gains from trade in this market, known as the total surplus.

Figure 8.9a-d The shaded area below €2 is the sum of the bakeries’ surpluses on every loaf that they produce. The whole shaded area shows the sum of all gains from trade in this market, known as the total surplus.

When the market for bread is in equilibrium with the quantity of loaves supplied equal to the quantity demanded, the total surplus is the area below the demand curve and above the supply curve.

Notice how the equilibrium allocation in this market differs from the allocation of a differentiated product, Beautiful Cars, in Unit 7. The equilibrium quantity of bread is at the point where the market supply curve, which is also the marginal cost curve, crosses the demand curve, and the total surplus is the whole of the area between the two curves. Figure 7.13 showed that in the market for Beautiful Cars, the manufacturer chooses to produce a quantity below the point where the marginal cost curve meets the demand curve, and the total surplus is lower than it would be at that point.

- deadweight loss

- A loss of total surplus relative to a Pareto-efficient allocation.

The competitive equilibrium allocation of bread has the property that the total surplus is maximized. Figure 8.9b shows that the surplus would be smaller if fewer than 5,000 loaves were produced. There would be consumers without bread who would be willing to pay more than the cost of producing another loaf, so there would be unexploited gains from trade. The total gains from trade in the market would be lower. We say there would be a deadweight loss equal to the triangle-shaped area. Producers would be missing out on potential profits, and some consumers would be unable to obtain the bread they were willing to pay for.

Leibniz: Gains from trade

Deadweight loss.

Deadweight loss.

Figure 8.9b Deadweight loss.

And if more than 5,000 loaves were produced, the surplus on the extra loaves would be negative: they would cost more to make than consumers were willing to pay. (Is the exchange of gifts at Christmas a similar case of deadweight loss?)

Joel Waldfogel, an economist, gave his chosen discipline a bad name by suggesting that gift-giving at Christmas may result in a deadweight loss.4 If you receive a gift that is worth less to you than it cost the giver, you could argue that the surplus from the transaction is negative. Do you agree?5

At the equilibrium, all the potential gains from trade are exploited. This property—that the combined consumer and producer surplus is maximized at the point where supply equals demand—holds in general: if both buyers and sellers are price-takers, the equilibrium allocation maximizes the sum of the gains achieved by trading in the market, relative to the original allocation. We demonstrate this result in our Einstein at the end of this section.

Pareto efficiency

- Pareto efficient

- An allocation with the property that there is no alternative technically feasible allocation in which at least one person would be better off, and nobody worse off.

At the competitive equilibrium allocation in the bread market, it is not possible to make any of the consumers or firms better off (that is, to increase the surplus of any individual) without making at least one of them worse off. Provided that what happens in this market does not affect anyone other than the participating buyers and sellers, we can say that the equilibrium allocation is Pareto efficient.

Pareto efficiency follows from three assumptions we have made about the bread market.

Price-taking

The participants are price-takers. They have no market power. When a particular buyer trades with a particular seller, each of them knows that the other can find an alternative trading partner willing to trade at the market price. Sellers can’t raise the price because of competition from other sellers, and competition from other buyers prevents buyers from lowering it. Hence the suppliers will choose their output so that the marginal cost (the cost of the last unit produced) is equal to the market price.

In contrast, the producer of a differentiated good has bargaining power because it faces less competition: no one else produces an identical good. The firm uses its power to keep the price high, raising its own share of the surplus but lowering total surplus. The price is above marginal cost, so the allocation is Pareto inefficient.

A complete contract

The exchange of a loaf of bread for money is governed by a complete contract between buyer and seller. If you find there is no loaf of bread in the bag marked ‘bread’ when you get home, you can get your money back. Compare this with the incomplete employment contract in Unit 6, in which the firm can buy the worker’s time, but cannot be sure how much effort the worker will put in. We will see in Unit 9 that this leads to a Pareto-inefficient allocation in the labour market.

No effects on others

We have implicitly assumed that what happens in this market affects no one except the buyers and sellers. To assess Pareto efficiency, we need to consider everyone affected by the allocation. If, for example, the early morning activities of bakeries disrupt the sleep of local residents, then there are additional costs of bread production and we ought to take the costs to the bakeries’ neighbours into account too. Then, we may conclude that the equilibrium allocation is not Pareto efficient after all. We will investigate this type of problem in Unit 12.

Fairness

Remember from Unit 5 that there are two criteria for assessing an allocation: efficiency and fairness. Even if we think that the market allocation is Pareto efficient, we should not conclude that it is necessarily a desirable one. What can we say about fairness in the case of the bread market? We could examine the distribution of the gains from trade between producers and consumers: Figure 8.9a showed that both consumers and firms obtain a surplus, and in this example consumer surplus is slightly higher than producer surplus. You can see that this happens because the demand curve is relatively steep compared with the supply curve. Recall also from Unit 7 that a steep demand curve corresponds to a low elasticity of demand. Similarly, the slope of the supply curve corresponds to the elasticity of supply: in Figure 8.9a, demand is less elastic than supply.

In general, the distribution of the total surplus between consumers and producers depends on the relative elasticities of demand and supply.

We might also want to take into account the market participants’ standard of living. For example, if a poor student buys a book from a rich student, we might think that an outcome in which the buyer paid less than the market price (closer to the seller’s reservation price) would be better, because it would be fairer. Or, if the consumers in the bread market were exceptionally poor, we might decide that it would be better to pass a law setting a maximum bread price lower than €2.00 to achieve a fairer (although Pareto-inefficient) outcome.6 In Unit 11, we will look at the effect of regulating markets in this way.

The Pareto efficiency of a competitive equilibrium allocation is often interpreted as a powerful argument in favour of markets as a means of allocating resources. But we need to be careful not to exaggerate the value of this result:

- The allocation may not be Pareto efficient: We might not have taken everything into account.

- There are other important considerations: Fairness, for example.

- Price-takers are hard to find in real life: It is not as easy as you might think to find behaviour consistent with our simple model of the bread market (as we will see in Section 8.9).

- willingness to pay (WTP)

- An indicator of how much a person values a good, measured by the maximum amount he or she would pay to acquire a unit of the good. See also: willingness to accept.

- willingness to accept (WTA)

- The reservation price of a potential seller, who will be willing to sell a unit only for a price at least this high. See also: willingness to pay.

Exercise 8.3 Maximizing the surplus

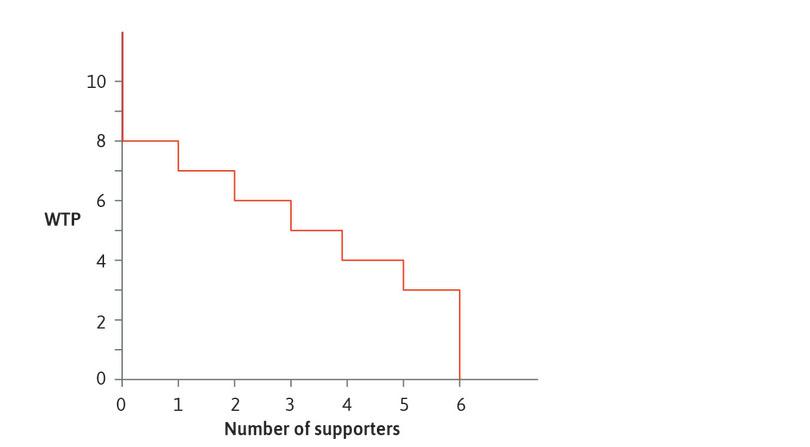

Consider a market for the tickets to a football match. Six supporters of the Blue team would like to buy tickets; their valuations of a ticket (their WTP) are 8, 7, 6, 5, 4, and 3. The diagram below shows the demand ‘curve’. Six supporters of the Red team already have tickets, for which their reservation prices (WTA) are 2, 3, 4, 5, 6, and 7.

![]()

- Draw the supply and demand ‘curves’ on a single diagram (Hint: the supply curve is also a step function, like the demand curve).

- Show that four trades take place in equilibrium.

- What is the equilibrium price?

- Calculate the consumer (buyer) surplus by adding up the surpluses of the four buyers who trade.

- Similarly calculate the producer (or seller) surplus.

- Hence, find the total surplus in equilibrium.

- Suppose that the market operates through bargaining between individual buyers and sellers. Find a way of matching the buyers and sellers so that more than four trades occur. (Hint: suppose the highest WTP buyer buys from the highest WTA seller.)

- In this case, work out the surplus from each trade.

- How does the total surplus in this case compare with the equilibrium surplus?

- Starting from the allocation of tickets you obtained through bargaining, in which at least five tickets are owned by Blue supporters, is there a way through further trade to make one of the supporters better off without making anyone worse off?

Exercise 8.4 Surplus and deadweight loss

- Sketch a diagram to illustrate the competitive market for bread, showing the equilibrium where 5,000 loaves are sold at a price of €2.00.

- Suppose that the bakeries get together to form a cartel. They agree to raise the price to €2.70, and jointly cut production to supply the number of loaves that consumers demand at that price. Shade the areas on your diagram to show the consumer surplus, producer surplus, and deadweight loss caused by the cartel.

- For what kinds of goods would you expect the supply curve to be highly elastic?

- Draw diagrams to illustrate how the share of the gains from trade obtained by producers depends on the elasticity of the supply curve.

Question 8.5 Choose the correct answer(s)

In Figure 8.9a, the market equilibrium output and price of the bread market is shown to be at (Q*, P*) = (5,000, €2). Suppose that the mayor decrees that bakeries must sell as much bread as consumers want, at a price of €1.50. Which of the following statements are correct?

- Producer surplus is lower, because the price is below marginal cost.

- Consumer surplus is higher, because the price of the first 5,000 loaves is lower, and for the additional loaves it is below the consumers’ WTP.

- The consumers benefit from the lower price, but producers lose because the price is below marginal cost.

- There is a deadweight loss, equal to the area of the triangle between the supply and demand curves to the right of equilibrium.

Question 8.6 Choose the correct answer(s)

Which of the following statements about a competitive equilibrium allocation are correct?

- The allocation maximizes the total surplus, but the does not mean it is best for everyone in the market—for example, we may think it is unfair.

- This must be true, since the allocation maximizes the total surplus.

- The equilibrium allocation may not be Pareto efficient if it affects someone other than the buyers or sellers.

- This is a general property of competitive equilibrium.

Einstein Total surplus and WTP

However the market works, and whatever prices are paid, we can calculate the consumer surplus by adding together the differences between WTP and price paid for all the people who buy, and the producer surplus by adding together the difference between price received and marginal cost of every unit of output:

Then when we calculate the total surplus, the prices paid and received cancel out:

When buyers and sellers are price-takers, and the price equalizes supply and demand, the total surplus is as high as possible, because the consumers with the highest WTPs buy the product and the units of output with the lowest marginal costs are sold. Every trade involves a buyer with a higher WTP than the seller’s reservation value, so the surplus would go down if we omitted any of them. And if we tried to include any more units of output in this calculation, the surplus would also go down because the WTPs would be lower than the MCs.

8.6 Changes in supply and demand

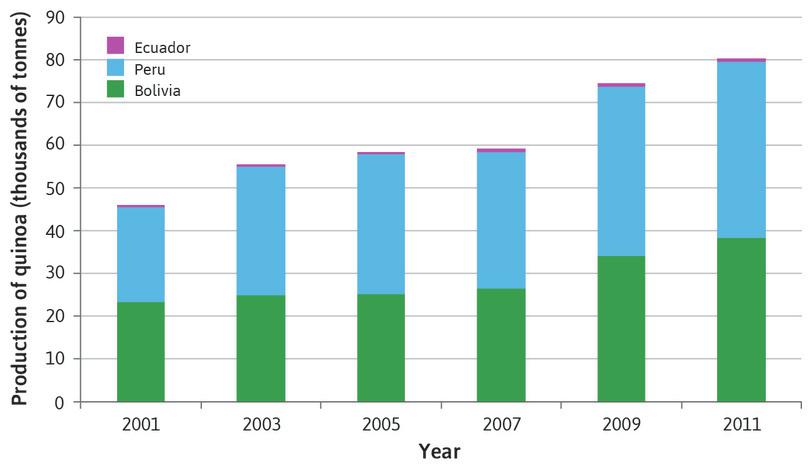

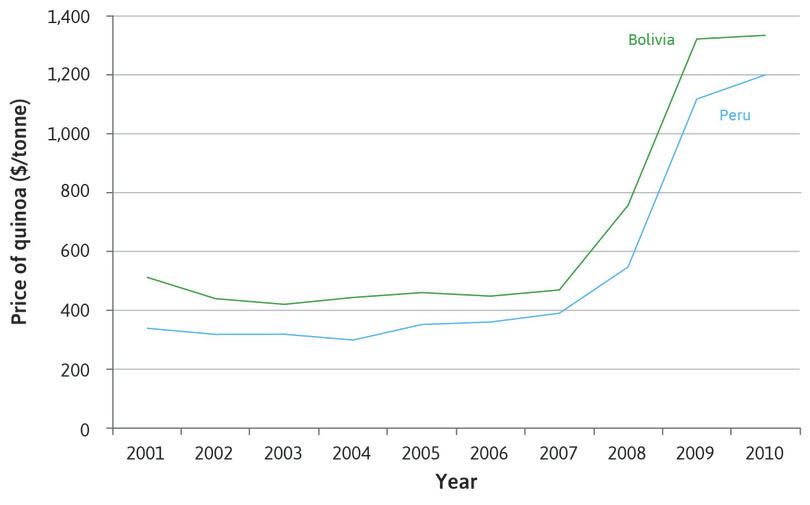

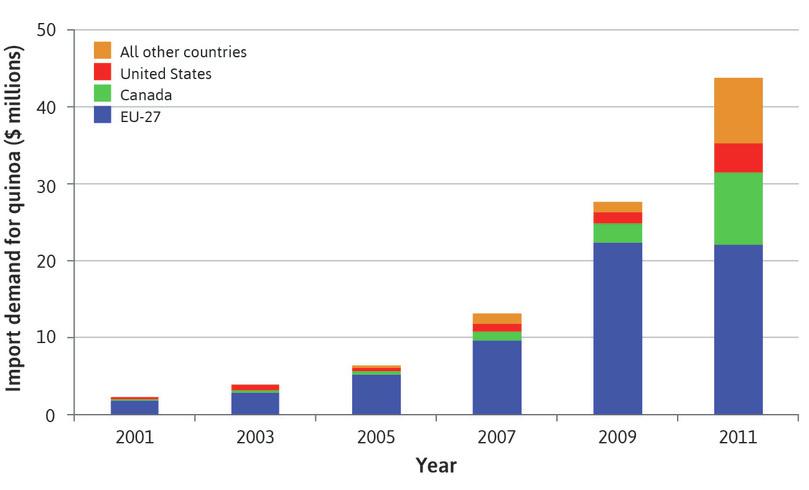

Quinoa is a cereal crop grown on the Altiplano, a high barren plateau in the Andes of South America. It is a traditional staple food in Peru and Bolivia. In recent years, as its nutritional properties have become known, there has been a huge increase in demand from richer, health-conscious consumers in Europe and North America. Figures 8.10a–c show how the market changed. You can see in Figures 8.10a and 8.10b that between 2001 and 2011, the price of quinoa trebled and production almost doubled. Figure 8.10c indicates the strength of the increase in demand: spending on imports of quinoa rose from just $2.4 million to $43.7 million in 10 years.

The production of quinoa.

The production of quinoa.

Figure 8.10a The production of quinoa.

Jose Daniel Reyes and Julia Oliver. ‘Quinoa: The Little Cereal That Could’. The Trade Post. 22 November 2013. Underlying data from Food and Agriculture Organization of the United Nations. FAOSTAT Database.

For the producer countries these changes are a mixed blessing. While their staple food has become expensive for poor consumers, farmers—who are amongst the poorest—are benefiting from the boom in export sales. Other countries are now investigating whether quinoa can be grown in different climates, and France and the US have become substantial producers.

How can we explain the rapid increase in the price of quinoa? In this section, we look at the effects of changes in demand and supply in our simple examples of books and bread. At the end of this section you can apply the analysis to the real-world case of quinoa.

An increase in demand

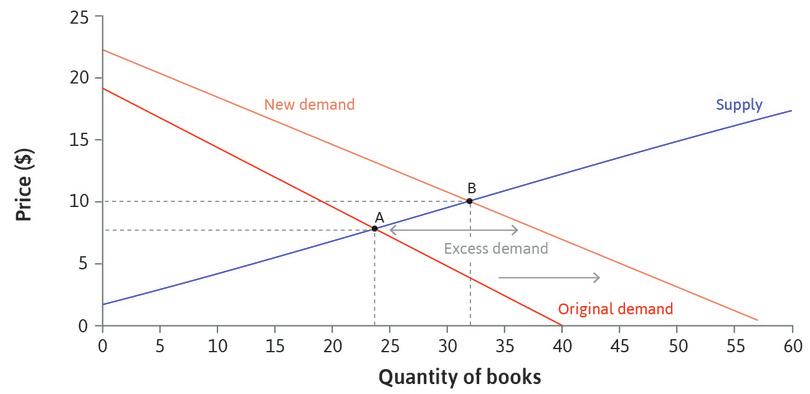

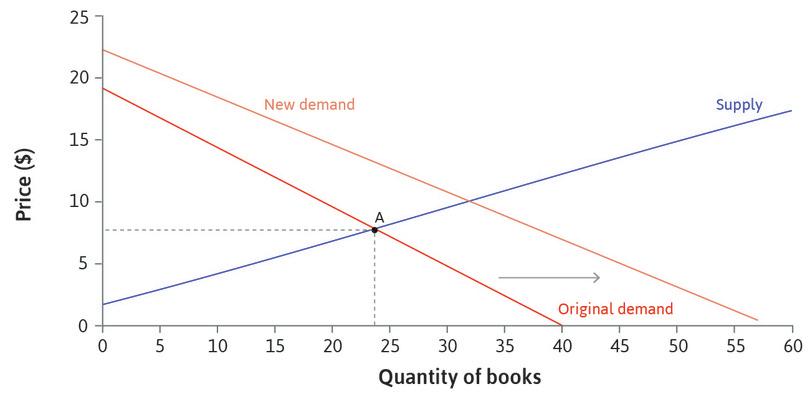

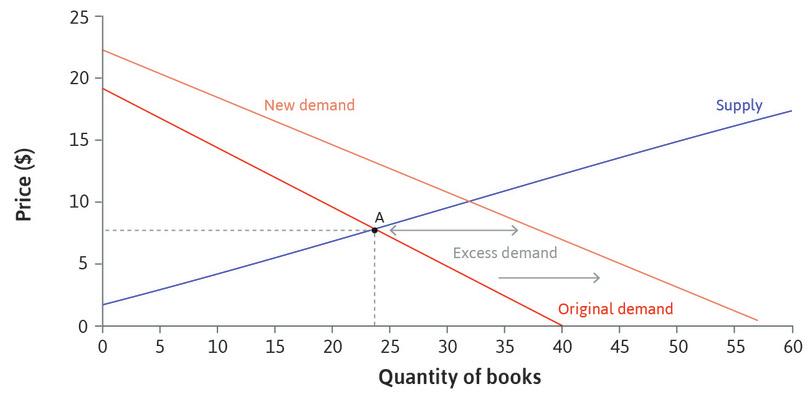

In the market for second-hand textbooks, demand comes from new students enrolling on the course, and supply comes from students who took the course in the previous year. In Figure 8.11 we have plotted supply and demand for textbooks when the number of students enrolling remains stable at 40 per year. The equilibrium price is $8 and 24 books are sold, as shown by point A. Suppose that in one year the course became more popular. Figure 8.11 shows what would happen.

An increase in the demand for books.

Figure 8.11 An increase in the demand for books.

The initial equilibrium point

At the original levels of demand and supply, the equilibrium is at point A. The price is $8, and 24 books are sold.

Figure 8.11a At the original levels of demand and supply, the equilibrium is at point A. The price is $8, and 24 books are sold.

An increase in demand

If there were more students enrolling in one year, there would be more students wanting to buy the book at each possible price. The demand curve shifts to the right.

Figure 8.11b If there were more students enrolling in one year, there would be more students wanting to buy the book at each possible price. The demand curve shifts to the right.

Excess demand when the price is $8

If the price remained at $8, there would be excess demand for books, that is, more buyers than sellers.

Figure 8.11c If the price remained at $8, there would be excess demand for books, that is, more buyers than sellers.

A new equilibrium point

There is a new equilibrium at point B with a price of $10, at which 32 books are sold. The increase in demand has led to a rise in the equilibrium quantity and price.

Figure 8.11d There is a new equilibrium at point B with a price of $10, at which 32 books are sold. The increase in demand has led to a rise in the equilibrium quantity and price.

The increase in demand leads to a new equilibrium, in which 32 books are sold for $10 each. At the original price, there would be excess demand and sellers would want to raise their prices. At the new equilibrium, both price and quantity are higher. Some students who would not have sold their books at $8 will now sell at a higher price. Notice, however, that although demand has increased, not all the students who would have bought at $8 will purchase the book at the new equilibrium: those with WTP between $8 and $10 no longer want to buy.

When we say ‘increase in demand’, it’s important to be careful about exactly what we mean:

- Demand is higher at each possible price, so the demand curve has shifted.

- In response to this shift there is a change in the price.

- This leads to an increase in the quantity supplied.

- This change is a movement along the supply curve.

- But the supply curve itself has not shifted (the number of sellers and their reserve prices have not changed), so we do not call this ‘an increase in supply’.

After an increase in demand, the equilibrium quantity rises, but so does the price. You can see in Figure 8.11 that the steeper (more inelastic) the supply curve, the higher the price will rise and the lower the quantity will increase. If the supply curve is quite flat (elastic), then the price rise will be smaller and the quantity sold will be more responsive to the demand shock.

An increase in supply due to improved productivity

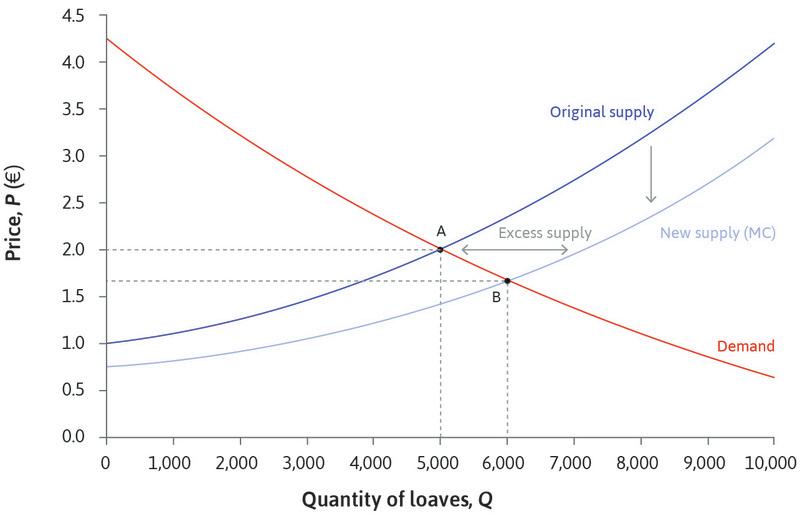

In contrast, as an example of an increase in supply, think again about the market for bread in one city. Remember that the supply curve represents the marginal cost of producing bread. Suppose that bakeries discover a new technique that allows each worker to make bread more quickly. This will lead to a fall in the marginal cost of a loaf at each level of output. In other words, the marginal cost curve of each bakery shifts down.

Figure 8.12 shows the original supply and demand curves for the bakeries. When the MC curve of each bakery shifts down, so does the market supply curve for bread. Look at Figure 8.12 to see what happens next.

An increase in the supply of bread: A fall in MC.

An increase in the supply of bread: A fall in MC.

Figure 8.12 An increase in the supply of bread: A fall in MC.

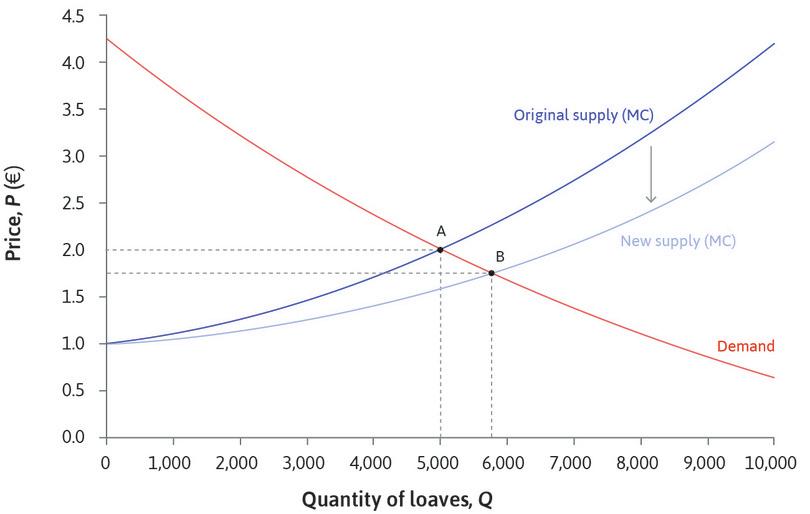

The initial equilibrium point

The city’s bakeries start out at point A, producing 5,000 loaves and selling them for €2 each.

Figure 8.12a The city’s bakeries start out at point A, producing 5,000 loaves and selling them for €2 each.

A fall in marginal costs

The market supply curve then shifts because of the fall in the bakeries’ marginal costs. The supply curve shifts down, because at each level of output, the marginal cost and therefore the price at which they are willing to supply bread is lower.

Figure 8.12b The market supply curve then shifts because of the fall in the bakeries’ marginal costs. The supply curve shifts down, because at each level of output, the marginal cost and therefore the price at which they are willing to supply bread is lower.

An increase in supply

The supply curve has shifted down. But another way to think of this change in supply is to say that the supply curve has shifted to the right. Since costs have fallen, the amount that bakeries will supply at each price is greater—an increase in supply.

Figure 8.12c The supply curve has shifted down. But another way to think of this change in supply is to say that the supply curve has shifted to the right. Since costs have fallen, the amount that bakeries will supply at each price is greater—an increase in supply.

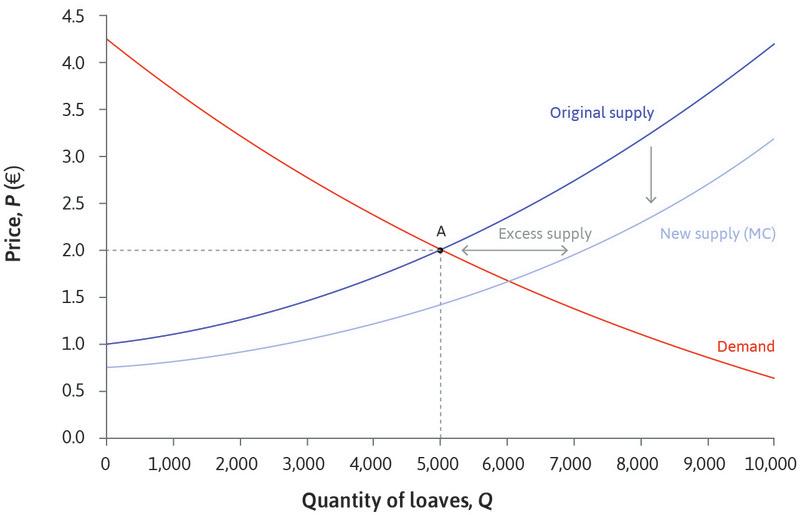

Excess supply when the price is €2

The effect of the fall in marginal cost is an increase in market supply. At the original price, there is more bread than buyers want (excess supply). The bakeries would want to lower their prices.

Figure 8.12d The effect of the fall in marginal cost is an increase in market supply. At the original price, there is more bread than buyers want (excess supply). The bakeries would want to lower their prices.

The new equilibrium point

The new market equilibrium is at point B, where more bread is sold and the price is lower. The demand curve has not shifted, but the fall in price has led to an increase in the quantity of bread demanded, along the demand curve.

Figure 8.12e The new market equilibrium is at point B, where more bread is sold and the price is lower. The demand curve has not shifted, but the fall in price has led to an increase in the quantity of bread demanded, along the demand curve.

The improvement in the technology of breadmaking leads to:

- an increase in supply

- a fall in the price of bread

- a rise in the quantity sold

Leibniz: Shifts in demand and supply

As in the example of an increase in demand, an adjustment of prices is needed to bring the market into equilibrium. Such shifts in supply and demand are often referred to as shocks in economic analysis. We start by specifying an economic model and find the equilibrium. Then we look at how the equilibrium changes when something changes—the model receives a shock. The shock is called exogenous because our model doesn’t explain why it happened: the model shows the consequences, not the causes.

- shock

- An exogenous change in some of the fundamental data used in a model.

- exogenous

- Coming from outside the model rather than being produced by the workings of the model itself. See also: endogenous.

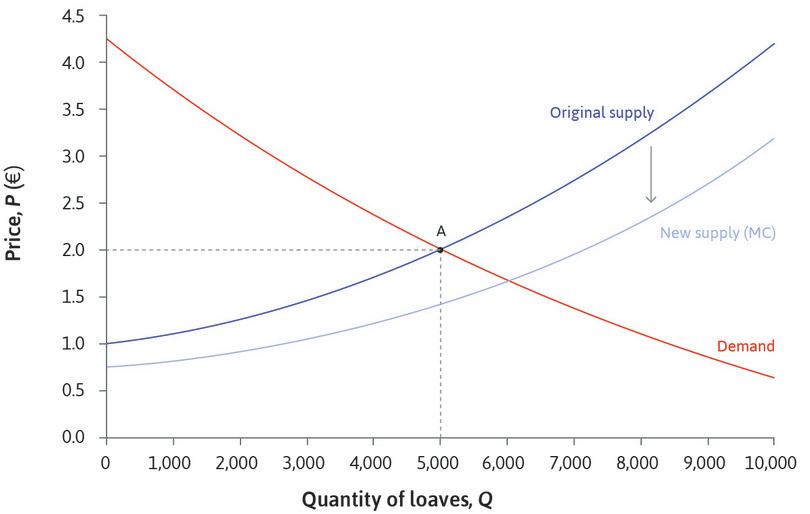

An increase in supply: More bakeries enter the market

Another reason for a change in market supply is the entry of more firms or the exit of existing firms. We analysed the equilibrium of the bread market in the case when there were 50 bakeries in the city. Remember from Section 8.4 that at the equilibrium price of €2, each bakery is on an isoprofit curve above the average cost curve. If economic profits are greater than zero, firms are receiving an economic rent, so other firms might want to invest in the baking business.

- costs of entry

- Startup costs that would be incurred when a seller enters a market or an industry. These would usually include the cost of acquiring and equipping new premises, research and development, the necessary patents, and the cost of finding and hiring staff.

Since there is an opportunity for making greater than normal profit by selling bread in the city, new bakeries may decide to enter the market. There will be some costs of entry, for example, acquiring and equipping the premises, but provided these are not too high (or if premises and equipment can be easily sold if the venture doesn’t work out) it will be worthwhile to do so.

Remember that we find the market supply curve by adding up the amounts of bread supplied by each firm, at each price. When more bakeries have entered, more bread will be supplied at each price level. Although the reason for the supply increase is different from the previous one, the effect on the market equilibrium is the same: a fall in price and a rise in bread sales. Figure 8.13 shows the effects on equilibrium. The bakeries once again start off at point A, selling 5,000 loaves of bread for €2. The entry of new firms shifts the supply curve outwards. There is more bread for sale at each price, so at the original price there would be excess supply. The new equilibrium is at point B with a lower price and higher bread sales.

An increase in the supply of bread: More firms enter.

An increase in the supply of bread: More firms enter.

Figure 8.13 An increase in the supply of bread: More firms enter.

The entry of new firms is unlikely to be welcomed by the existing bakeries. Their costs have not changed, but the market price has fallen to €1.75, so they must be making less profit than before. As we will see in Unit 11, the entry of new firms may eventually drive economic profits to zero, eliminating rents altogether.

Exercise 8.5 The market for quinoa

Consider again the market for quinoa. The changes shown in Figures 8.10a–c can be analysed as shifts in demand and supply.

- Suppose there was an unexpected increase in demand for quinoa in the early 2000s (a shift in the demand curve). What would you expect to happen to the price and quantity initially?

- Assuming that demand continued to rise over the next few years, how do you think farmers responded?

- Why did the price stay constant until 2007?

- How could you account for the rapid price rise in 2008 and 2009?

- Would you expect the price to fall eventually to its original level?

Exercise 8.6 Prices, shocks, and revolutions

Historians usually attribute the wave of revolutions in Europe in 1848 to long-term socioeconomic factors and a surge of radical ideas. But a poor wheat harvest in 1845 lead to food shortages and sharp price rises, which may have contributed to these sudden changes.7

The table shows the average and peak prices of wheat from 1838 to 1845, relative to silver. There are three groups of countries: those where violent revolutions took place, those where constitutional change took place without widespread violence, and those where no revolution occurred.

- Explain, using supply and demand curves, how a poor wheat harvest could lead to price rises and food shortages.

- Find a way to present the data to show that the size of the price shock, rather than the price level, is associated with the likelihood of revolution.

- Do you think this is a plausible explanation for the revolutions that occurred?

- A journalist suggests that similar factors played a part in the Arab Spring in 2010. Read the post. What do you think of this hypothesis?

Avg. price 1838–45 Max. price 1845–48 Violent revolution 1848 Austria 52.9 104.0 Baden 77.0 136.6 Bavaria 70.0 127.3 Bohemia 61.5 101.2 France 93.8 149.2 Hamburg 67.1 108.7 Hessedarmstadt 76.7 119.7 Hungary 39.0 92.3 Lombardy 88.3 119.9 Mecklenburgschwerin 72.9 110.9 Papal states 74.0 105.1 Prussia 71.2 110.7 Saxony 73.3 125.2 Switzerland 87.9 146.7 Württemberg 75.9 128.7 Immediate constitutional change 1848 Belguim 93.8 140.1 Bremen 76.1 109.5 Brunswick 62.3 100.3 Denmark 66.3 81.5 Netherlands 82.6 136.0 Oldenburg 52.1 79.3 No revolution 1848 England 115.3 134.7 Finland 73.6 73.7 Norway 89.3 119.7 Russia 50.7 44.1 Spain 105.3 141.3 Sweden 75.8 81.4 Berger, Helge, and Mark Spoerer. 2001. ‘Economic Crises and the European Revolutions of 1848.’ The Journal of Economic History 61 (2): pp. 293–326.

Question 8.7 Choose the correct answer(s)

Figure 8.8 shows the equilibrium of the bread market to be 5,000 loaves per day at price €2. A year later, we find that the market equilibrium price has fallen to €1.50. What can we conclude?

- This is not the only possible cause of a fall in price.

- This is not the only possible cause of a fall in price.

- A downward shift in either curve would cause the price to fall. If we knew whether output had increased or decreased, we could determine which curve had shifted.

- At the market equilibrium price, there is no excess demand or supply.

Question 8.8 Choose the correct answer(s)

Which of the following statements are correct?

- If mortgage borrowing becomes cheaper, more people will want to buy houses at each house price.

- A launch of a substitute would decrease demand, shifting the demand curve down.

- The quantity of oil demanded would increase by moving along the demand curve; the curve itself would not move.

- The marginal cost of producing plastics would fall, so the supply curve would shift down.

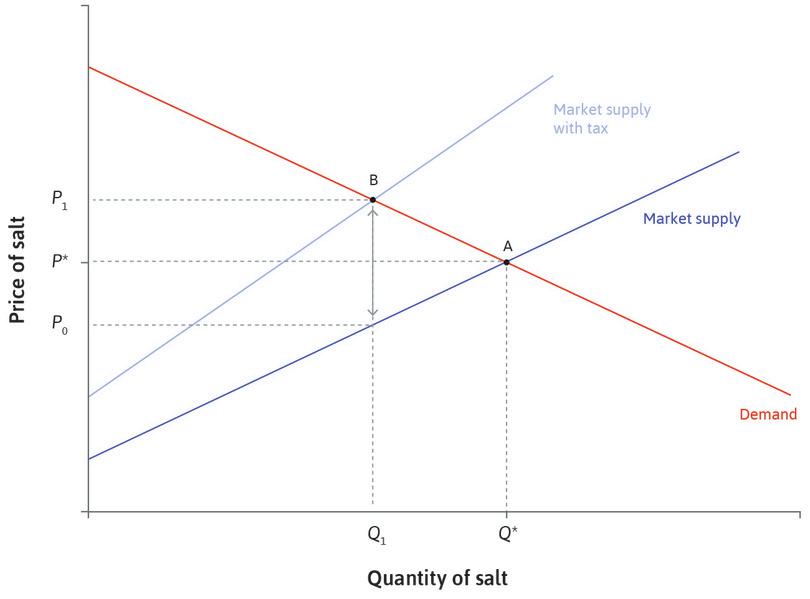

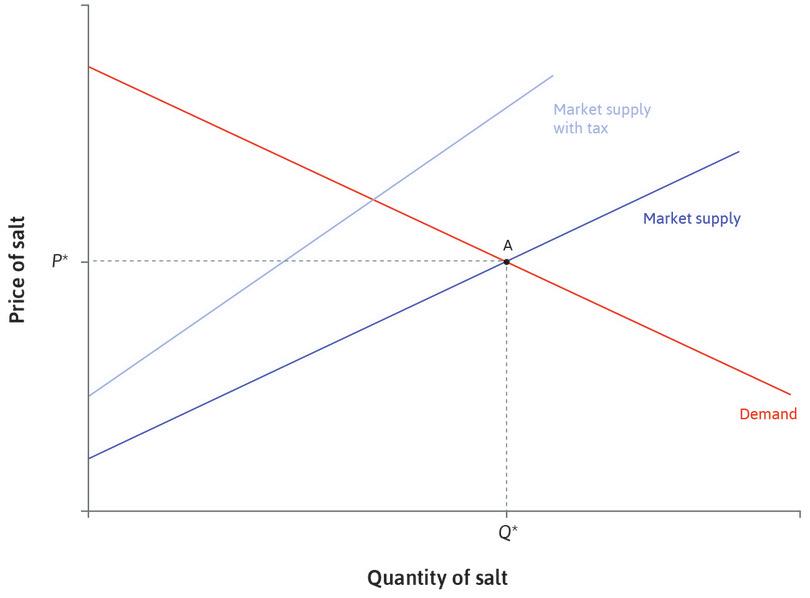

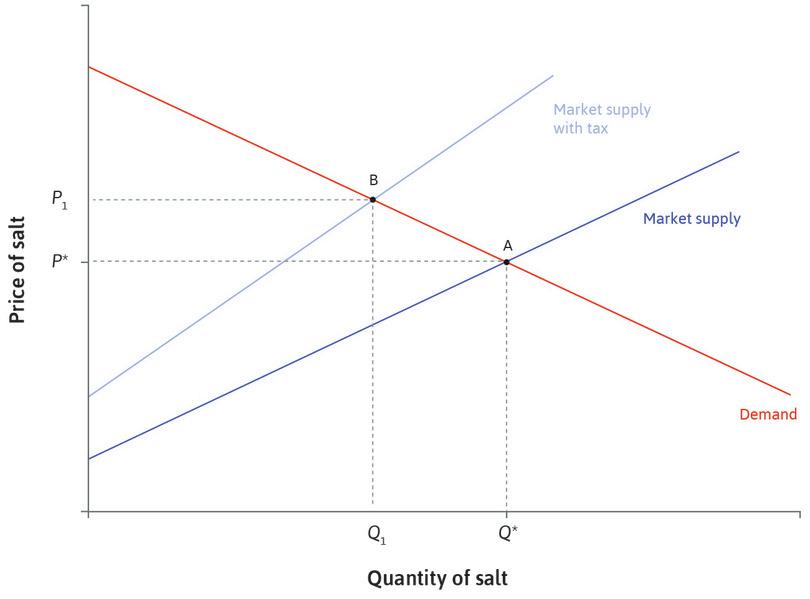

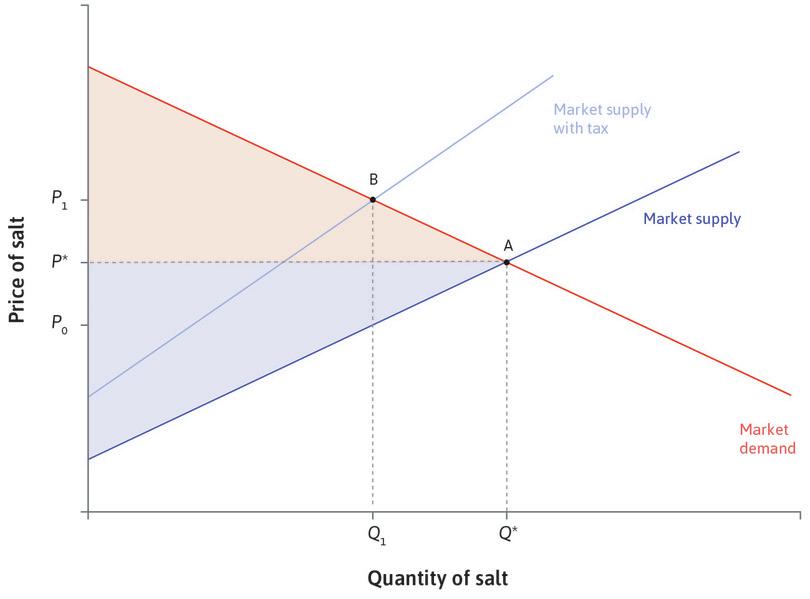

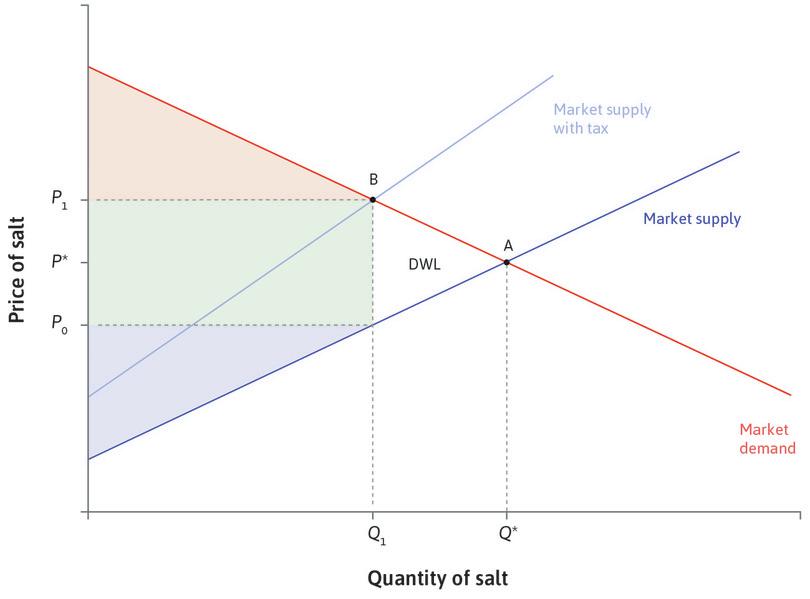

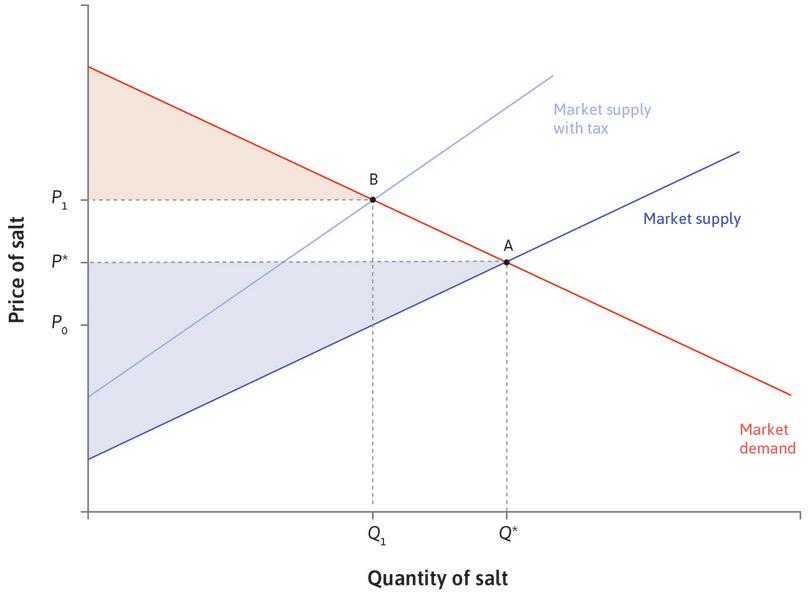

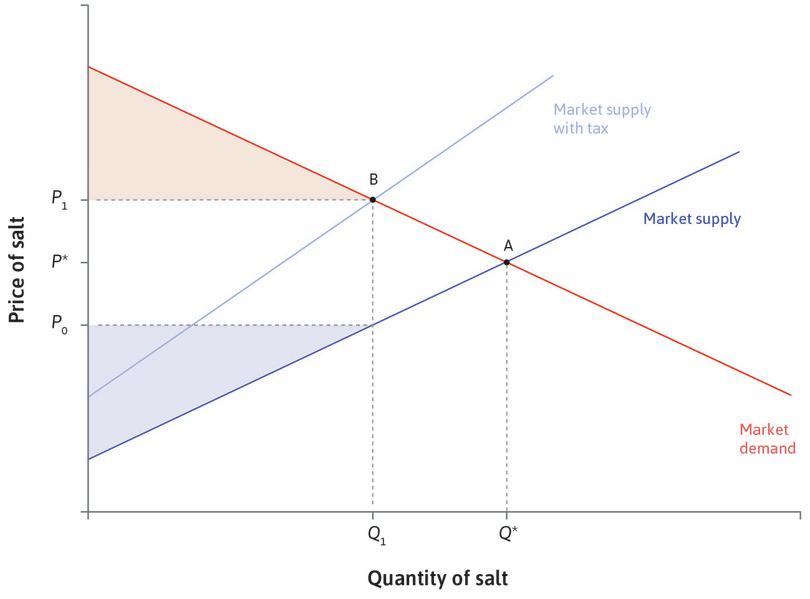

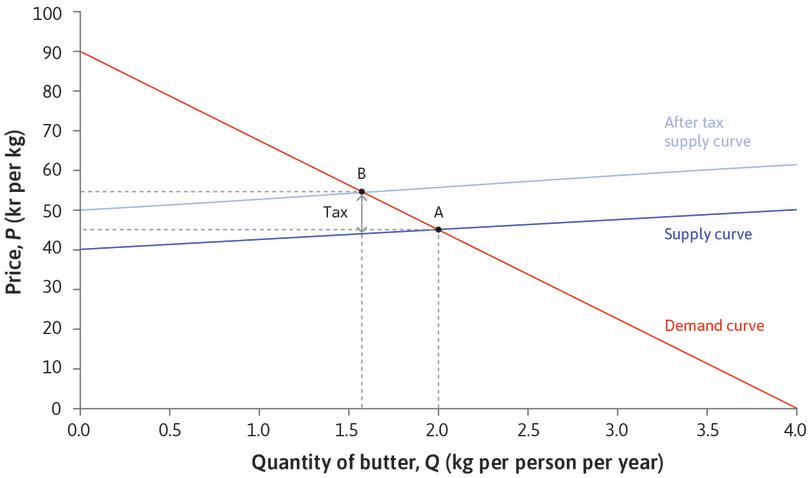

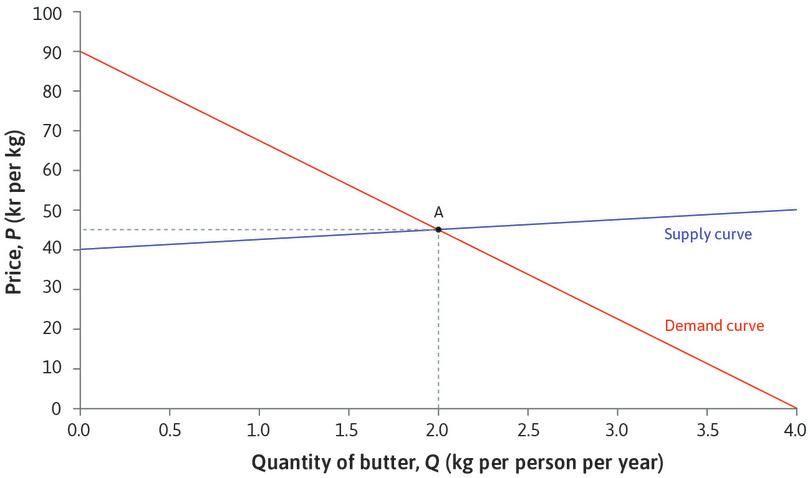

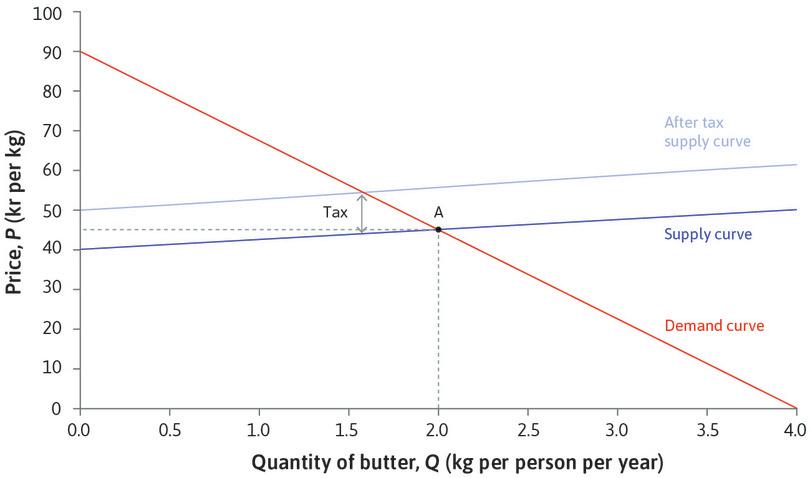

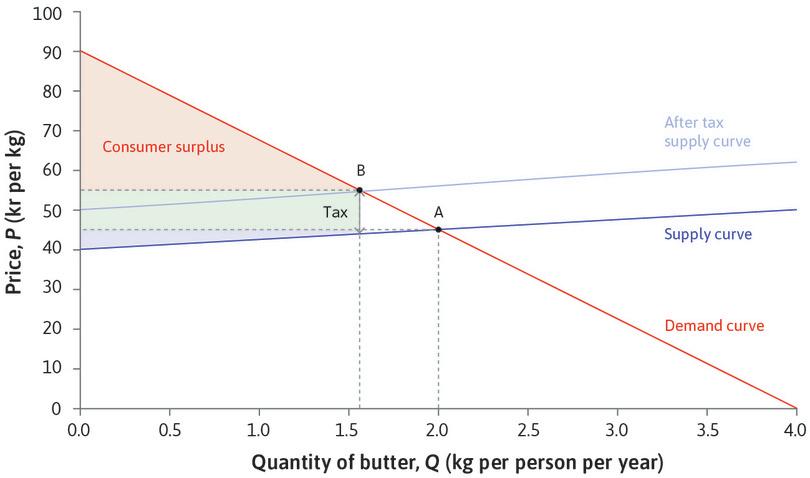

8.7 The effects of taxes

Governments can use taxation to raise revenue (to finance government spending, or redistribute resources) or to affect the allocation of goods and services in other ways, perhaps because the government considers a particular good to be harmful. The supply and demand model is a useful tool for analysing the effects of taxation.

Using taxes to raise revenue