Unit 15 Inflation, unemployment, and monetary policy

Themes and capstone units

How the rate of unemployment and the level of output in the economy affect inflation, the challenges this poses to policymakers, and how this knowledge can support effective policies to stabilize employment and incomes

- When unemployment is low, inflation tends to rise. When unemployment is high, inflation falls.

- Policymakers and voters prefer low unemployment and low inflation (but not a falling price level).

- They typically cannot have both and face a trade-off instead.

- There is an inflation-stabilizing rate of unemployment, and a wage-price inflation spiral develops if unemployment is kept lower than this.

- Monetary policy affects aggregate demand and inflation through a variety of channels.

- Adverse shocks, such as an oil price increase, can lead to higher unemployment and higher inflation.

- Many governments have given responsibility for monetary policy—often described as inflation targeting—to central banks.

Before his successful 1992 US presidential campaign, Bill Clinton’s electoral strategists had decided that two of their campaign issues should be health policy and ‘change’. But it was the third focus of his campaign—the recession of 1991—that resonated with the public. The reason was the phrase the campaign workers used: ‘The economy, stupid!’

The 1991 recession meant that many Americans lost their jobs, and the Clinton campaign slogan brought this issue to the attention of the voters. When the ballots were counted in November 1992, Clinton received almost 6 million more votes than George H. W. Bush, the incumbent president.

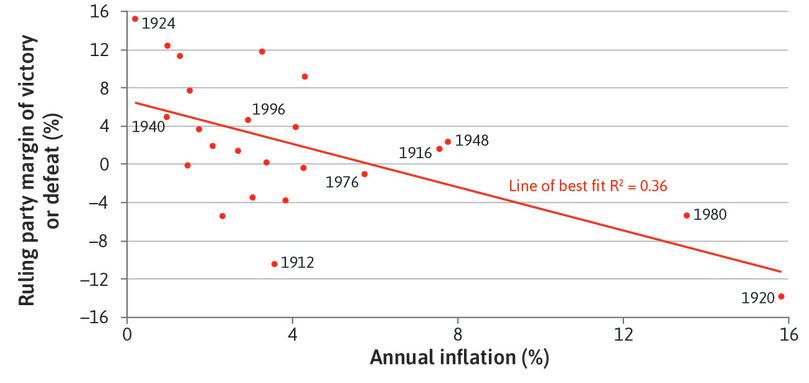

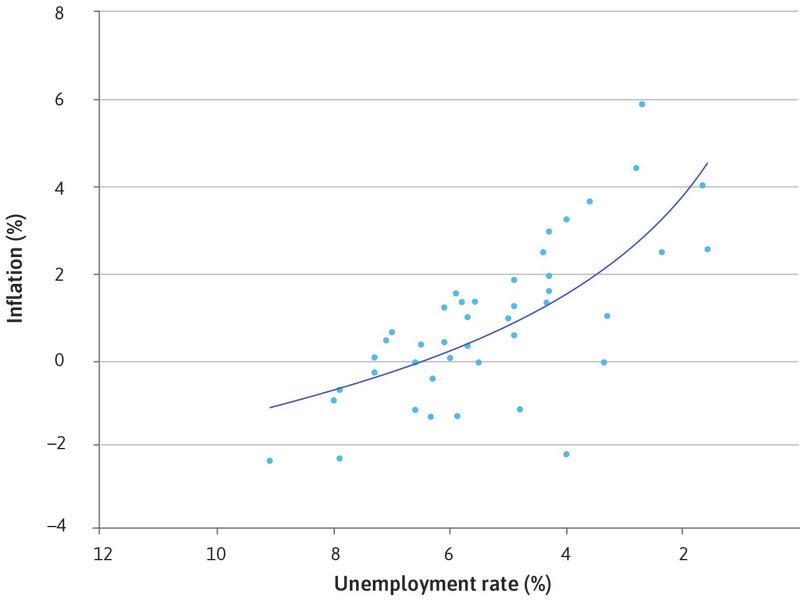

In a democracy, election outcomes are always affected by the state of the economy, and how the public judges the economic competence of the government and the opposition. Two important measures of this economic performance are unemployment and inflation. In Unit 13 we saw that unemployment undermines our wellbeing, but inflation worries us too. Figure 15.1 shows that in US presidential elections, the margin of victory of the ruling party is higher when inflation is lower.

Inflation and presidential election victory in the US (1912–2012).

Figure 15.1 Inflation and presidential election victory in the US (1912–2012).

Inflation before 1950: Michael Bordo, Barry Eichengreen, Daniela Klingebiel, and Maria Soledad Martinez-Peria. 2001. ‘Is the Crisis Problem Growing More Severe?’. Economic Policy 16 (32) (April): pp. 52–82; CPI after 1950: Federal Reserve Bank of St. Louis. 2015. FRED; Electoral results: US National Archives. 2012. ‘1789–2012 Presidential Elections’. US Electoral College.

So if you are a politician worrying about your citizens’ concerns as well as your own career, you should minimize both unemployment and inflation. Is this possible?

We get an insight by looking at how a German minister of finance, trained as an economist, handled his dual role as a politician (at an election rally in the evening) and as an economist (in his office the next day).

Helmut Schmidt was called the ‘super minister’ in the West German government of Chancellor Willy Brandt because he was both minister of economics and minister of finance.

At an election rally in 1972, he claimed that: ‘Five per cent inflation is easier to bear than five per cent unemployment.’ He promised that his party would prioritize lower unemployment whilst keeping inflation low and stable.

Helmut Schmidt (1918–2015) was West German Chancellor from 1974 until 1982. In 1972, inflation in West Germany was 5.5% (up from 5.2% the previous year) and unemployment was 0.7% (up from 0.5% the previous year). By 1975, inflation was 5.9% and unemployment was 3.1%.

The following day Professor Otto Schlecht, head of the economics policy department at the Federal Ministry of Economics, said to Schmidt: ‘Herr Minister, what you said yesterday, which is in the newspapers this morning, is false.’

Schmidt replied: ‘I agree that what I said was technically wrong. But you cannot advise me about what I decide is politically expedient to say to an election rally in front of 10,000 Ruhr miners in the Westfalenhalle in Dortmund.’

Helmut Schmidt’s commitment at the rally and his explanation afterward, show two things about the relationship between economics and politics. The first is that politicians are elected to office, and so respond to the views of voters. The second is that politicians as policymakers face constraints on their choice of policies. They can’t just promise the economic outcomes that voters care about—in Schmidt’s case: low unemployment, and low and stable inflation. The economist in Schmidt was well aware of the constraints but, at the rally, he was speaking as a politician.

- opportunity cost

- When taking an action implies forgoing the next best alternative action, this is the net benefit of the foregone alternative.

While the policymaker wants to deliver both low unemployment and low inflation, the economy operates in such a way that when unemployment goes down, inflation tends to go up. And when inflation falls, unemployment tends to go up. This is a problem we have seen before: policymakers must deliver what is feasible, and this involves trading one objective off against the other. Another way to say this: more inflation is the opportunity cost of lower unemployment, and more unemployment is the opportunity cost of less inflation. Moreover, the economy is subject to shocks that can make both inflation and unemployment worse, limiting the set of feasible outcomes. And experience from the late 1960s showed that inflation would carry on rising if unemployment were too low. This was the setting for Helmut Schmidt’s reflections on his election promise.

- inflation targeting

- Monetary policy regime where the central bank changes interest rates to influence aggregate demand in order to keep the economy close to an inflation target, which is normally specified by the government.

Following the experience of rising inflation across the world, during the late 1980s there was a rethinking of how macroeconomic policy should be designed. In the 1990s, the policy known as inflation targeting by central banks was widely adopted. Many governments delegated the management of fluctuations in the economy to the central bank, with fiscal policy playing a lesser role, and recognized that policies to improve the supply side of their economies—such as increasing competition and better functioning labour markets—were necessary if they wanted to achieve a lower rate of unemployment compatible with low and stable inflation.

As we saw in Unit 11, prices are messages. They send signals about scarce resources. We looked at how shifts in demand or supply for a good resulted in a change in its price relative to other goods and services, and how this signalled a change in the relative scarcity of the good or service. In this unit, we look not at relative prices but at inflation or deflation: a rise or fall in prices in general. We begin by asking how inflation got a bad name.

15.1 What’s wrong with inflation?

Before we turn to the question, we need to clarify a few terms.

- inflation

- An increase in the general price level in the economy. Usually measured over a year. See also: deflation, disinflation.

- deflation

- A decrease in the general price level. See also: inflation.

- disinflation

- A decrease in the rate of inflation. See also: inflation, deflation.

What is the difference between inflation, deflation, and disinflation?

A car analogy is a useful way to think about these differences. We can compare what happens to the price level in the economy with a car’s initial location and the distance covered when it travels at different speeds:

- Zero inflation: A constant price level from year to year means that inflation is zero. This is like a stationary car: the car’s location is constant and the distance travelled per hour is zero.

- Inflation: Now, consider a rate of inflation, such as 2% per year. This means that the price level goes up by 2% each year. This is the case of a car travelling at a constant speed: a car travelling at 20 km per hour means that the distance from the initial location increases by 20 km each hour. After two hours, the car is 40 km away from its initial location; after another hour, it is 60 km away, and so on.

- Deflation: Deflation is when the price level falls. This is equivalent to the car travelling backward at 20 km per hour. After an hour, the car is 20 km behind its initial location, and so on.

- Rising inflation: If the rate of inflation is increasing, the price level is increasing at an increasing rate. Suppose now that the rate of inflation increases from 2% to 4% to 6% in successive years, so the economy experiences rising inflation. This is the case of a car accelerating: the distance travelled from the starting point is increasing at an increasing rate, for example from 20 km per hour in the first hour to 40 km per hour in the second hour, and so on. After two hours, the car is 60 km away from its initial location.

- Falling inflation: This is called disinflation and is equivalent to a car reducing its speed, for example from 60 km per hour to 40 km per hour to 20 km per hour. Once the speed reaches zero, the car’s location does not change. The equivalent in the economy is that when inflation falls to zero, the price level does not change.

Describing a change in price level

- Inflation: The price level is rising

- Deflation: The price level is falling

- Disinflation: The inflation rate is falling

We have seen why voters dislike unemployment. But why do voters dislike inflation? For some people in the economy, such as some pensioners, incomes are fixed in nominal terms, meaning that they receive a fixed number of yuan or dollars or euros. If prices rise during the year, these households can buy fewer goods and services at the end of the year than they could at the beginning. They are worse off and will tend to vote against a party they believe will permit higher inflation.

Whether one loses or benefits from inflation also depends on which side of the credit market one is on. Julia the borrower and Marco the lender (in Unit 10) have a conflict about the interest rate at which Julia borrows. They also have differing interests about inflation, because if prices rise before Julia repays her loan, Marco will find that he can buy less with the repayment than would have been the case if there were zero inflation.

- nominal interest rate

- The interest rate uncorrected for inflation. It is the interest rate quoted by high-street banks. See also: real interest rate, interest rate.

- real interest rate

- The interest rate corrected for inflation (that is, the nominal interest rate minus the rate of inflation). It represents how many goods in the future one gets for the goods not consumed now. See also: nominal interest rate, interest rate.

More generally, using the same logic as we used when discussing the government’s debt in the previous unit, inflation means that:

- Borrowers with nominal debt will benefit: Those with mortgages on fixed nominal interest rate loans, for example, will benefit from inflation, because the debt stays the same in nominal terms, and so becomes smaller in real terms.

- Lenders with nominal assets will lose: Banks or others who have loaned money at fixed nominal interest rates will lose, because when the sum is repaid it will be worth less in terms of the goods or services it can buy. Very high inflation will wipe out the value of nominal assets, which happened in Zimbabwe in 2008–2009.1

- Fisher equation

- The relation that gives the real interest rate as the difference between the nominal interest rate and expected inflation: real interest rate = nominal interest rate – expected inflation.

To take account of inflation when analysing borrowing and lending, we use what is termed the real interest rate, which is defined as follows and is also known as the Fisher equation:

The real interest rate measures the buying power of the repayment of a loan at the prices that exist when the loan is repaid. To see what this means, let’s suppose Julia were to borrow $50 from Marco with a repayment of $55 next year. The nominal interest rate is 10%. But if next year’s prices were 6% higher than this year’s (6% inflation rate), then what Marco could buy with the repayment is not 10% more than he could have bought with the sum he loaned to Julia, but instead only 4%. The real interest rate is 4%.

In addition to redistributing income from creditors (those with assets) and those on nominally fixed incomes (like pensioners) to debtors, in some cases inflation can also make the economy work less well. While there is no evidence that moderate inflation is bad for the economy, when inflation is high it is often also volatile and therefore hard to predict. Large price changes create uncertainty, and make it more difficult for individuals and firms to make decisions based on prices.

- relative price

- The price of one good or service compared to another (usually expressed as a ratio).

- menu costs

- The resources used in setting and changing prices.

In an environment of high and volatile inflation, it is hard to separate the signal about the scarcity of resources (sent by relative prices) from the noise of erratically rising prices. Firms might find it harder to know which sector to invest in, or which crop would be better to plant (quinoa or barley, for example); individuals would find it harder to decide whether quinoa has become more expensive relative to other sources of protein. Moreover, in an inflationary environment, firms have to update their prices more frequently than they would prefer. This requires time and resources, referred to as menu costs.

Would households and firms be better off with falling prices? No. A sustained fall in the price level is undesirable for many of the same reasons that inflation is undesirable, and could have even more dramatic economic consequences. When prices are falling, households will postpone consumption (particularly of expensive items such as fridges, televisions, and cars) because they expect goods will be cheaper in the future. Similarly, deflation increases the debt burden of borrowers, for the same reason that inflation reduces it.

As we have seen in Unit 14, a rise in the debt burden depresses consumption because some affected households save to restore their target wealth and others find themselves credit-constrained. The fall in consumption will induce a drop in aggregate demand and economic activity. Weaker aggregate spending will tend to depress prices further and can trigger a vicious circle of falling prices and economic stagnation.

This happened in Japan. The Japanese economy was one of the great success stories of the period after the Second World War. The upward slope of its hockey stick was remarkably steep, as you saw in Unit 1. Living standards, as measured by GDP per capita, went from less than one-fifth of the level in the US in 1950 to more than 70% by 1980. But in the past 25 years, Japan has faced low growth and rising unemployment. For the first time for an advanced economy in the postwar period, there has been persistent deflation: deflation was observed in 12 years out of 21 between 1995 and 2015.

Many economists think that a little bit of inflation is a good thing, as long as it remains stable. In the next unit we will see one reason why this is the case. The process of innovation and change that characterizes a dynamic economy means that, in any given year, workers in some firms and sectors will be more in demand than in others. With rising prices, a fall in real income among the losers may be masked by the fact that nominal incomes are rising, or at least not falling. For example, many people will not even notice a slight fall in their real wage due to modest inflation, but nobody would fail to notice a reduction in his or her nominal wage. With some low inflation, the adjustment of workers and resources between different firms and industries in response to changes in relative wages can take place without losers experiencing falling nominal wages. Inflation greases the wheels of the labour market.

Another important reason to prefer a bit of inflation to none is that it gives monetary policy more room to manoeuvre. As we will see later, positive inflation allows the real interest rate to go lower in order to offset a major recession than if inflation is zero.

Question 15.1 Choose the correct answer(s)

The following table shows the annual inflation rate (the GDP deflator) of Japan, the UK, China, and South Sudan in the period 1996–2015 (Source: World Bank).

| 1996–2000 | 2001–2005 | 2006–2010 | 2011–2015 | |

|---|---|---|---|---|

| Japan | −1.9% | −0.9% | -0.5% | 1.6% |

| UK | 2.1% | 1.7% | 1.8% | 1.8% |

| China | 8.1% | 2.4% | 2.1% | 0.8% |

| South Sudan | 54.1% | 6.5% | 0.6% | −18.7% |

Based on this information, which of the following statements is correct?

- Japan experienced a falling price level—deflation—between 1996 and 2010. Disinflation describes a falling inflation rate but the inflation rate became less negative over time.

- In the UK the inflation rate remained stable. This means that the price level increased at a stable rate, not that the price level remained stable.

- China has been experiencing disinflationary pressure (falling inflation) and not deflationary pressure (which is a falling price level).

- The price level is lower in 2015 than in 2011 because inflation was negative, but it was not negative enough to outweigh the high inflation rate over 1996–2000.

Question 15.2 Choose the correct answer(s)

The following table shows the nominal interest rate and the annual inflation rate (the GDP deflator) of Japan in the period 1996–2015 (Source: World Bank).

| 1996–2000 | 2001–2005 | 2006–2010 | 2011–2015 | |

|---|---|---|---|---|

| Interest rate | 1.5% | 1.4% | 1.3% | 1.2% |

| Inflation rate | –1.9% | –0.9% | –0.5% | 1.6% |

Based on this information, which of the following statements are correct?

- Using the Fisher equation, the real interest rate in 1996–2000 was 1.5 – (–1.9) = 3.4%.

- The real interest rates for the four periods are: 3.4%, 2.3%, 1.8%, and –0.4% respectively. Therefore the real interest rate has been falling consistently over the period.

- It was positive in the first three periods and turned negative in 2011–2015.

- The decline in the real interest rate each year is larger than the decline in the nominal interest rate because the inflation rate was also rising.

15.2 Inflation results from conflicting and inconsistent claims on output

Inflation arises from conflicts among economic actors, when they are powerful enough that their claims on goods and services are inconsistent.

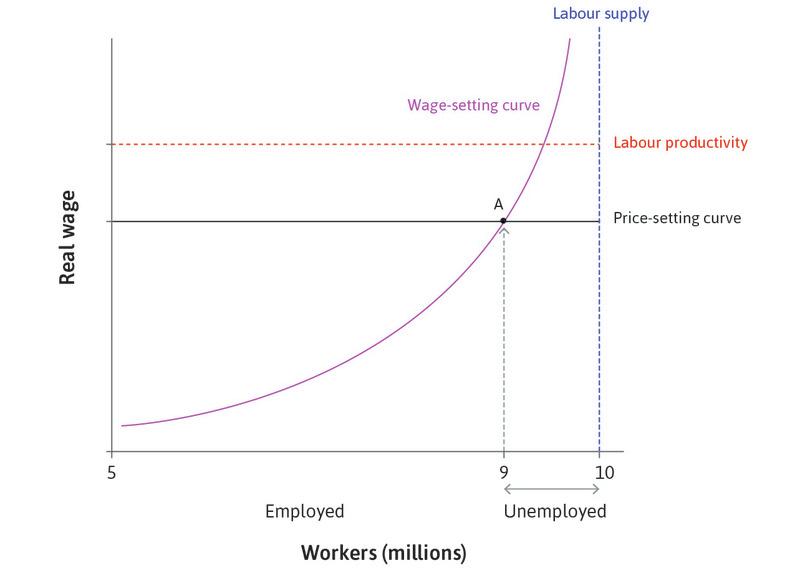

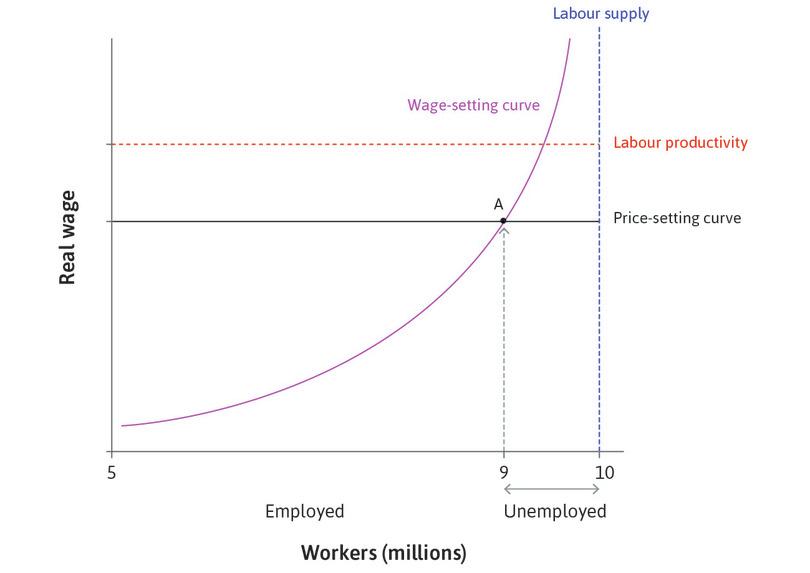

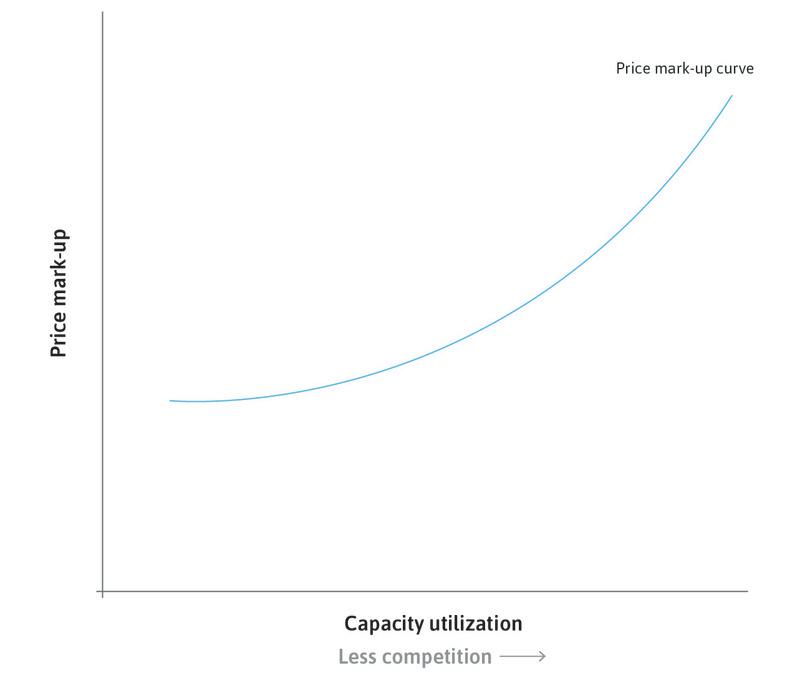

To see how this works, think of an economy composed of many firms (each of which is owned by a single individual) and their employees, who are also the consumers of the various goods produced by the firms. To keep track of what is happening in the firms, we assume that prices are set by the marketing department and wages by the human resources (HR) department.

Initially the marketing department in each firm is setting prices based on the markup that maximizes its profits, given the degree of competition in the markets in which it sells (as we saw in Units 7 and 9). And the HR department is also setting the real wage for its workers (which is the nominal wage in the firm, divided by the price level in the economy) as the lowest wage consistent with workers actually working, given the level of unemployment in the economy (as we saw in Units 6 and 9).

If, once all firms have set their wages and prices, the wage rate and the price level are consistent with the firms maximizing their profits, then there will be no reason for either prices or wages to be changed. At this unemployment rate, the price level is constant (inflation is zero). This is the level of unemployment where the wage-setting and price-setting curves intersect, that is, the labour market Nash equilibrium that we saw in Unit 9.

- protectionist policy

- Measures taken by a government to limit trade; in particular, to reduce the amount of imports in the economy. These are designed to protect local industries from external competition. They can take different forms, such as taxes on imported goods or import quotas.

Suppose now that the government adopts protectionist policies, which make it difficult for foreign firms to enter its markets. Then the markets facing the firm become less competitive, so that the firm can charge a higher markup on its costs. If this is the case across the economy, the resulting increase in the price level will lower the real wage of the workers. But while the owner of an individual firm is happy with the higher price that the marketing department can now charge, the workers are unhappy with the fall in the real wage. The result is that workers now lack the motivation to work. So the HR department of the firm will raise its nominal wage, and all other firms will do the same. Both prices and wages have risen and the economy experiences inflation.

Will it end there? No. The nominal wage increase has raised the cost of production to firms and they will use this as the basis of their markup pricing, leading to a further increase in prices and a fall in the real wage, which the HR department will correct by again raising the nominal wage. The process of rising wages and prices will continue as long as:

- firms are powerful enough to charge the higher markup

- workers at the given unemployment rate have enough bargaining power to require the initial real wage in order to motivate them to work

In the example given, inflation rose while unemployment did not change, following a change in the competitive conditions facing firms that allowed them to raise their markup, increasing the owners’ profits. But there are other ways that the process could have begun from the same starting point. Suppose the degree of competition in product markets remains the same, but the level of employment rises. At the new lower level of unemployment the firms would want to pay workers a higher real wage to keep them working. This induces the marketing departments of firms to raise their prices, so as to maintain the markup that competitive conditions allowed. And the inflationary process would begin.

To summarize, inflation may result from:

- An increase in the bargaining power of firms over their consumers: This is caused by a reduction in competition, which allows firms to charge a higher markup. It is a downward shift of the price-setting curve.

- An increase in the bargaining power of workers over firms: This allows them to get a higher wage in return for working hard.

There are two ways that the increase in the bargaining power of workers could take place:

- A shift upward of the wage-setting curve: The wage they would receive is higher at every level of employment.

- An increase in the level of employment, moving along the wage-setting curve: In this case, the wage-setting curve is unchanged.

We studied reasons for the shift in the wage-setting curve, such as improved generosity of unemployment benefits or stronger trade unions, in Unit 9. The movement along the wage-setting curve, rather than a shift in the curve, is what we will analyse next.

- wage inflation

- An increase in the nominal wage. Usually measured over a year. See also: nominal wage.

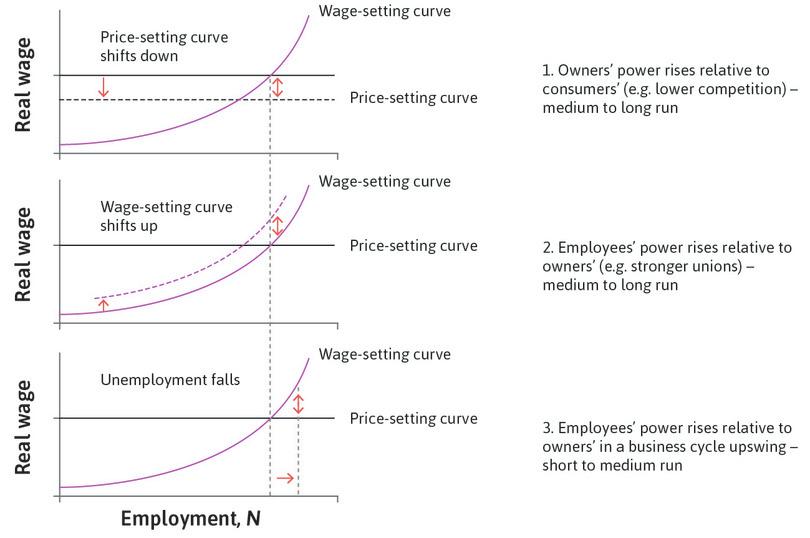

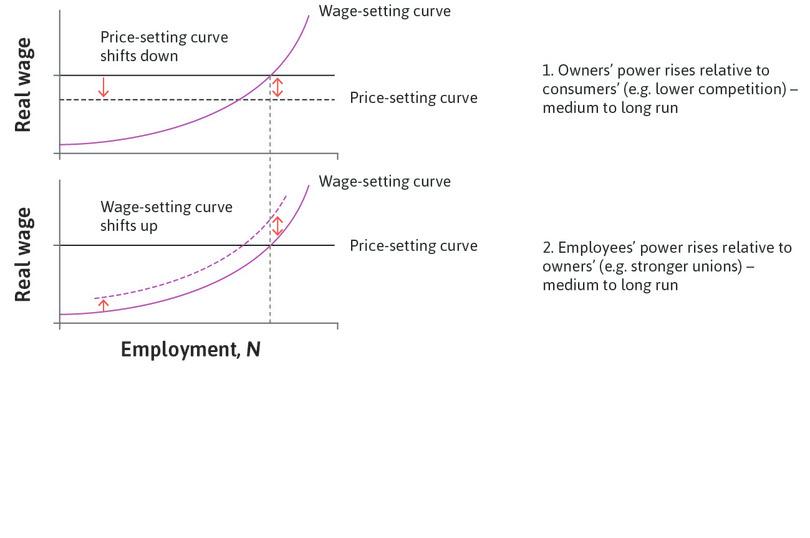

Figure 15.2 summarizes three causes of inflation. In Section 15.3, we explain how the changes in bargaining power illustrated in Figure 15.2 translate into inflation. The third cause—higher employment may result in inflation—came to light when William (Bill) Phillips, the economist, published a scatter plot of annual wage inflation and unemployment in the British economy. This is shown in Figure 15.3.

Three causes of inflation: changes in bargaining power.

Figure 15.2 Three causes of inflation: changes in bargaining power.

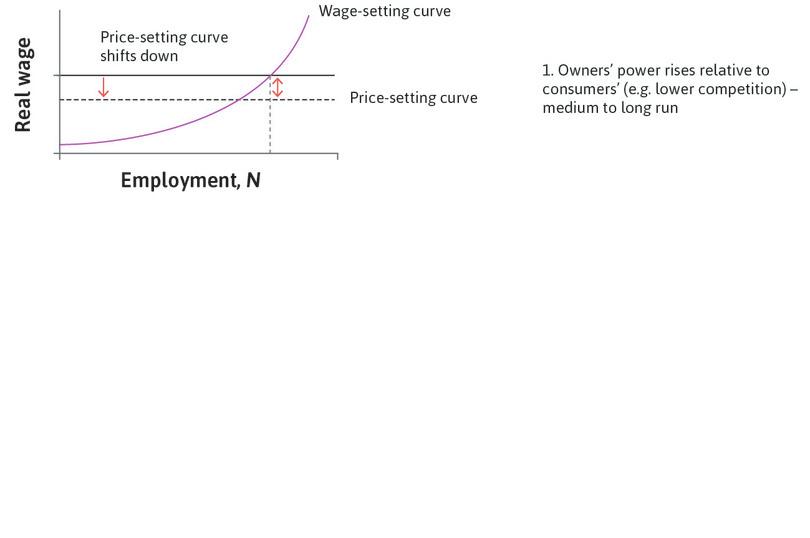

Owners’ power rises relative to consumers’

For example, due to lower competition (medium- to long-run effect).

Figure 15.2a For example, due to lower competition (medium- to long-run effect).

Employees’ power rises relative to owners’

For example, due to stronger unions (medium- to long-run effect).

Figure 15.2b For example, due to stronger unions (medium- to long-run effect).

Employees’ power rises relative to owners’

For example, due to a business cycle upswing (short- to medium-run effect).

Figure 15.2c For example, due to a business cycle upswing (short- to medium-run effect).

Phillips’s original curve: Wage inflation and unemployment (1861–1913).

Figure 15.3 Phillips’s original curve: Wage inflation and unemployment (1861–1913).

Ryland Thomas and Nicholas Dimsdale. (2017). ‘A Millennium of UK Data’. Bank of England OBRA dataset.

Great economists Bill Phillips

A. W. (‘Bill’) Phillips (1914–1975) was an unusually colourful character for a world-renowned economist. Raised in New Zealand, Phillips spent time as a crocodile hunter, a movie director, and a prisoner of war in Indonesia during the Second World War, before finally becoming a professor at the London School of Economics.

Phillips had engineering know-how, and while studying sociology in London in 1949, he built a hydraulic machine to model the British economy. The Monetary National Income Analogue Computer (MONIAC) used transparent pipes and coloured water to bring economists’ equations to life. It was like the hydraulic economy model produced by Irving Fisher half a century earlier (mentioned in Unit 2), but much more elaborate. MONIAC had tanks for each of the components of domestic GDP, such as investment, consumption, and government expenditures. Imports and exports were shown by water being added or drained from the model. The machine could be used to model the effect on the economy of shocks to different variables, such as tax rates and government spending, which would set in motion flows between the tanks. Working versions of the machine can still be found in the London Science Museum and universities around the world.2

- Phillips curve

- An inverse relationship between the rate of inflation and the rate of unemployment.

In a 1958 paper, Phillips made another major contribution to the study of economics. By drawing a scatterplot of the data for the rates of unemployment and inflation in the British economy between 1861 and 1913, he found that low rates of unemployment were associated with high rates of inflation, and high unemployment with low inflation. The relationship has since been referred to as the Phillips curve.

Question 15.3 Choose the correct answer(s)

The following diagram depicts the model of the labour market:

The labour market

Suppose now that the government adopts policies that make it difficult for foreign firms to enter its markets. Assume that the level of employment and the labour supply remain constant. Which of the following statements regarding mechanisms by which inflation is created are correct?

- A higher markup implies a downward shift in the price-setting curve.

- Wages rise because the economy is below the wage-setting curve at the unchanged unemployment rate. The wage-setting curve does not shift.

- This process is described in the text.

- This process is described in the text.

Question 15.4 Choose the correct answer(s)

The following diagram depicts the model of the labour market:

Suppose there is an increase in workers’ bargaining power that causes inflation. Which of the following statements are correct?

- The wage-setting curve rises if workers’ bargaining power increases.

- An increase in the unemployment level along a given wage-setting curve results in a fall in the real wage required to motivate to work, to below the price-setting curve. This represents a decline in workers’ bargaining power and will lead to deflation, not inflation.

- The increase in workers’ bargaining power can be due to an upward shift of the wage-setting curve or a decline in unemployment along the wage-setting curve. Once this has occurred, there is no further shift in the curves. Inflation is due to the fact that the economy is no longer at the intersection of the two curves.

- Inflation occurs due to the fact that the economy is no longer at the intersection of the two curves, and does not involve further moves in the curves.

15.3 Inflation, the business cycle, and the Phillips curve

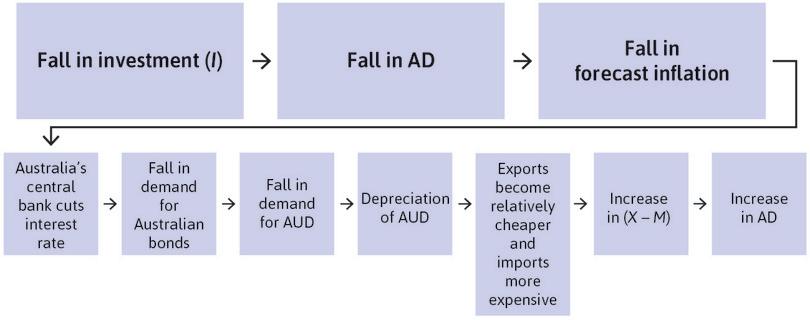

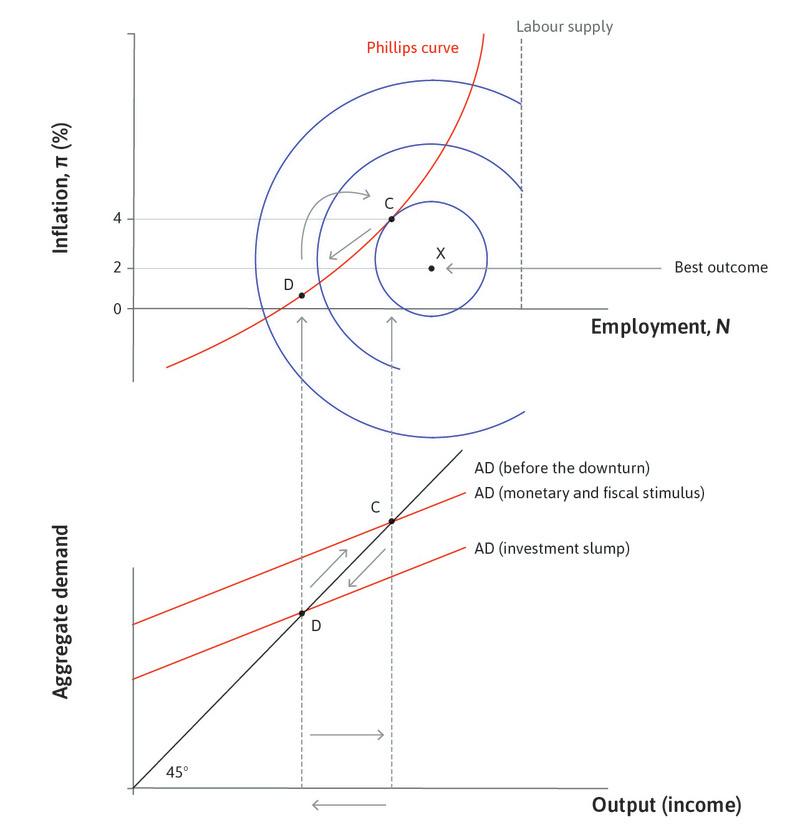

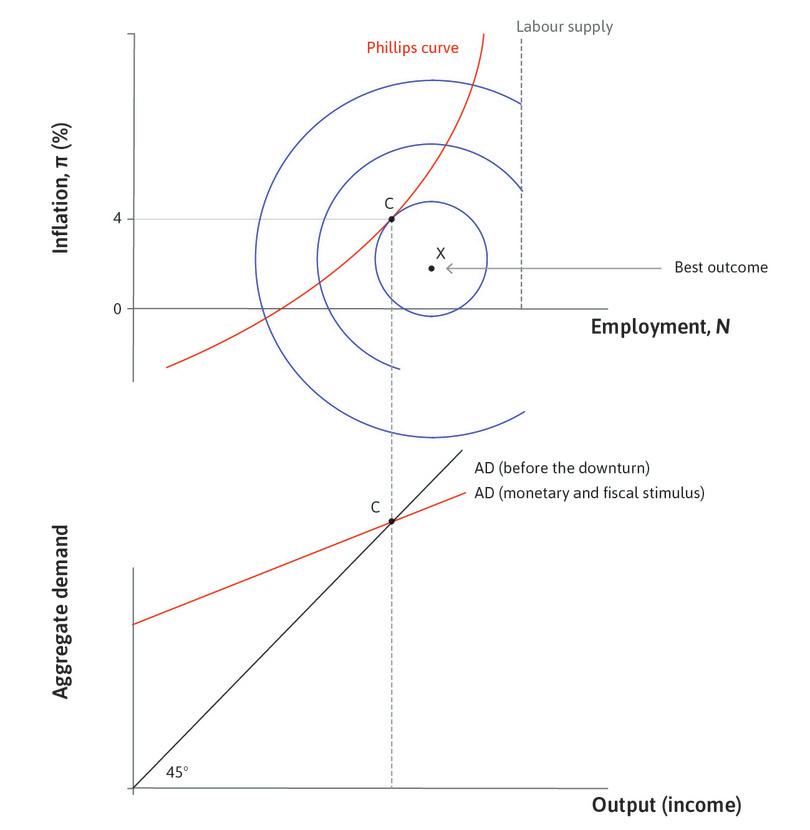

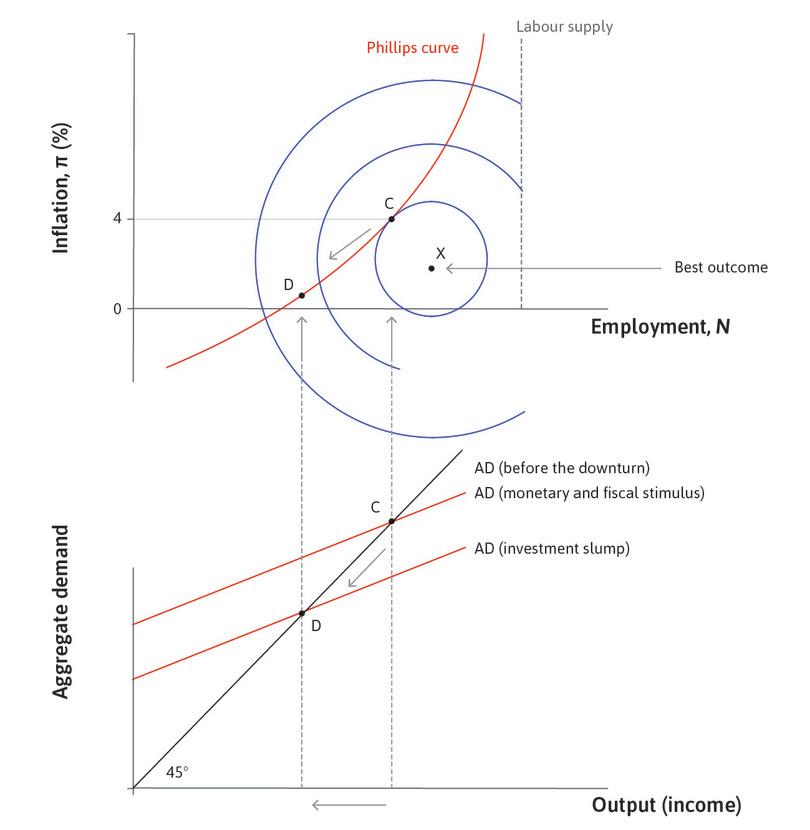

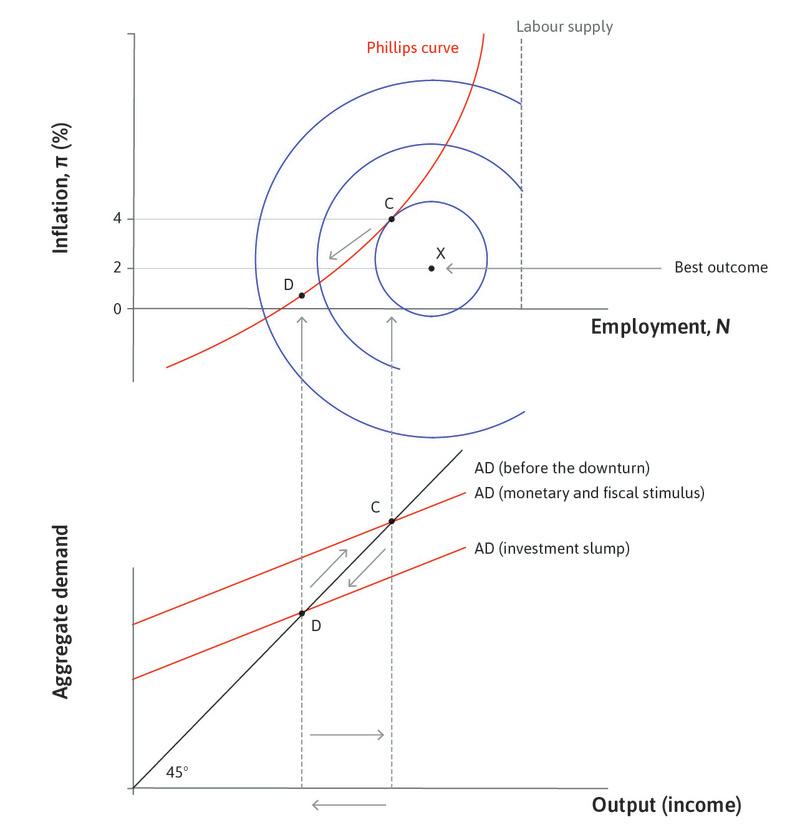

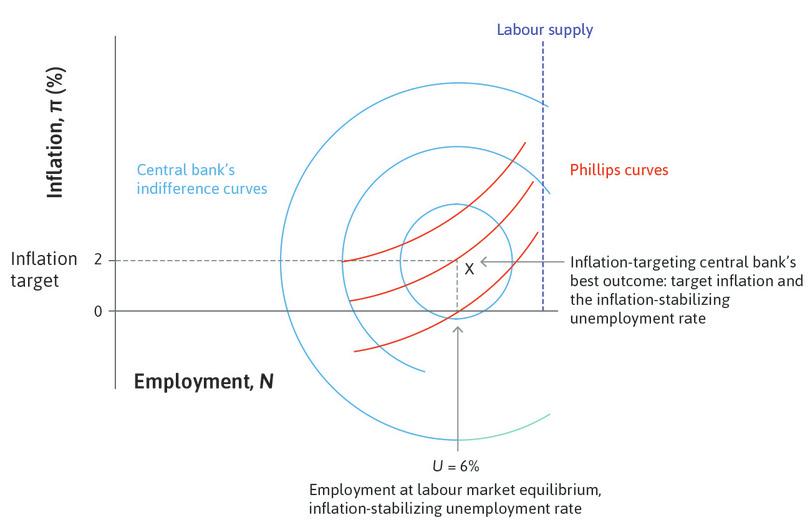

When central banks report their interest rate decision to the public, they normally justify a rise in the interest rate by saying that forecast inflation is up. They are raising the interest rate to dampen aggregate demand, raise cyclical unemployment, and as a result, bring inflation back toward target.

Conversely, if they are announcing a lower interest rate, they explain that this is because there is a danger of inflation falling too low (possibly into deflation). Just as a reduction in aggregate demand and employment will bring inflation down, a rise in aggregate demand and employment will increase inflation.

To model inflation, we assume that the HR departments of firms set nominal wages (for example, in dollars, pounds, or euros) once a year, and that the marketing departments set prices immediately after wages. The real wage that employees care about is their nominal wage relative to the economy-wide level of prices, and is defined as:

- real wage

- The nominal wage, adjusted to take account of changes in prices between different time periods. It measures the amount of goods and services the worker can buy. See also: nominal wage.

It is the real wage on the vertical axis in the labour market diagram in Question 15.4.

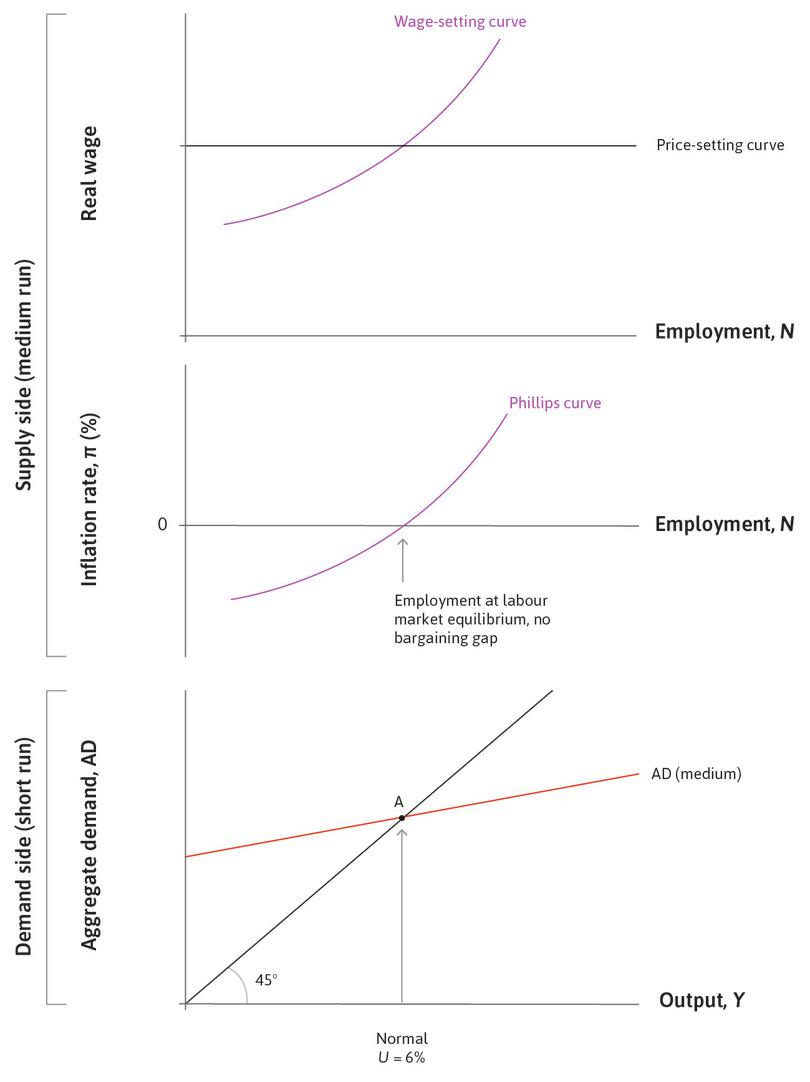

To see how inflation comes about in a business cycle upswing, we begin with the economy at the labour market equilibrium and with constant prices, and consider a rise in aggregate demand, which reduces unemployment below the equilibrium.

- When unemployment is low, the HR department needs to set higher wages: The cost of job loss is low and workers expect higher real wages if they are to work effectively.

- Higher wages mean higher costs for firms: The marketing department will raise prices to cover the higher costs. As long as competitive conditions have not changed, the firm’s markup will be unchanged.

- The price level will have gone up: Once all firms in the economy have set higher prices, the economy has experienced wage and price inflation. And real wages have not increased: the percentage increase in W equals the percentage increase in P, so W/P is unchanged.

- wage-price spiral

- This occurs if an initial increase in wages in the economy is followed by an increase in the price level, which is followed by an increase in wages and so on. It can also begin with an initial increase in the price level.

What happens next? We assume that aggregate demand remains high enough to keep unemployment below the labour market equilibrium. At the next annual round of wage-setting, the HR department is in the same position as the previous year: with continuing low unemployment, workers are disappointed with their real wage. It must raise nominal wages. When costs go up, the marketing department raises prices once more. This is called the wage-price spiral. It explains why, at low unemployment, the price level rises, not just in the year that unemployment fell, but year after year.

If there is a recession instead of a boom, the wage-price spiral operates in reverse, and the price level falls year after year.

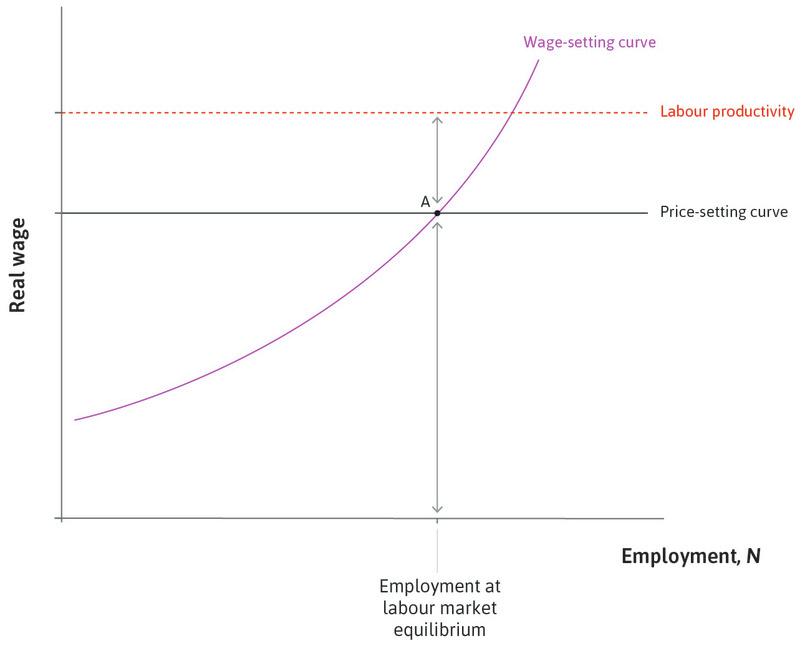

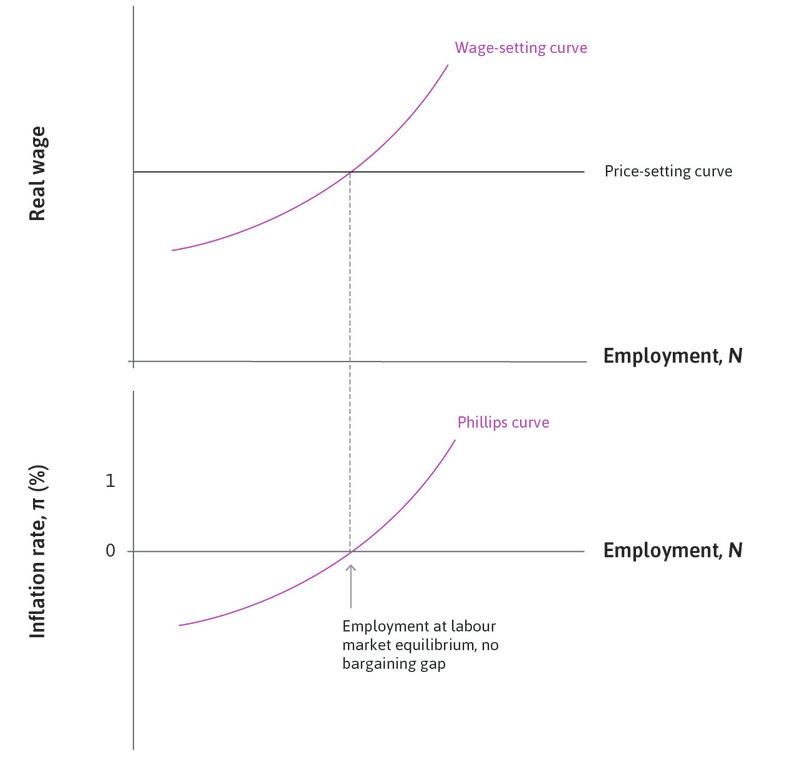

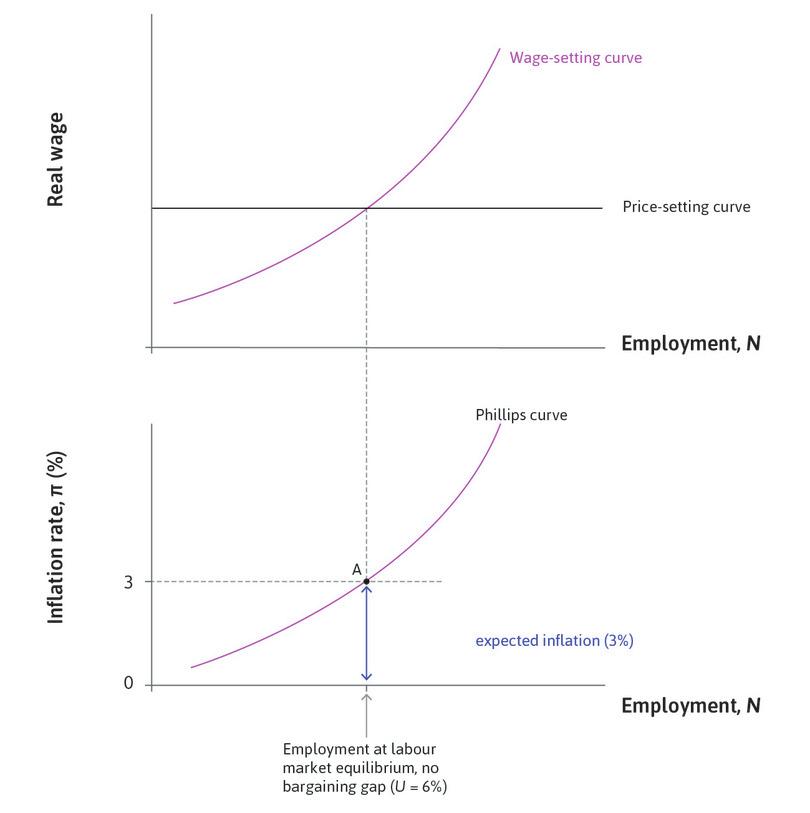

We now ask why prices would have been constant year after year before the boom in aggregate demand reduced unemployment. We will see that when the labour market is in equilibrium (the normal phase of the business cycle), there is no pressure for wages and prices to change. From Unit 9 we know that labour market equilibrium is where the wage-setting curve and the price-setting curve intersect. But why is this unemployment rate so special for the rate of inflation?

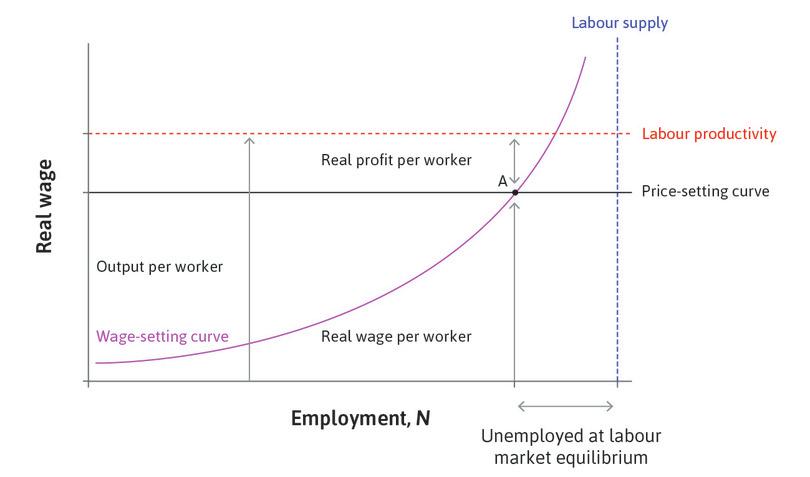

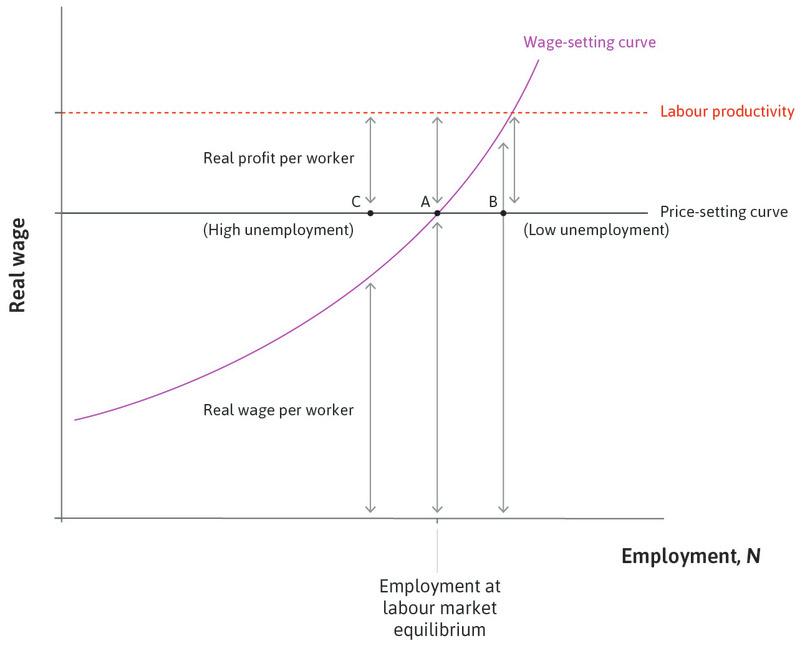

In Figure 15.4a, it is only at point (A), where the real wage on the wage-setting curve coincides with the real wage on the price-setting curve, that the labour market is at a Nash equilibrium. As we saw in Unit 9, at this point both workers and firms are doing the best that they can, given the actions of the other. At A, the claims of owners for profits and of workers for wages add up exactly to the size of the pie (the sum of the double-headed arrows showing the profits per worker and real wages is equal to output per worker, which is shown by the red dashed line). This means that the HR department will have no reason to raise wages, and with no increase in costs, the marketing department will keep prices unchanged. The real wage will remain constant and no one will be disappointed.

Inflation and conflict over the pie: Stable price level at labour market equilibrium.

Figure 15.4a Inflation and conflict over the pie: Stable price level at labour market equilibrium.

In an economy at the unemployment rate at labour market equilibrium (point A), wages and prices will be stable and inflation will be zero.

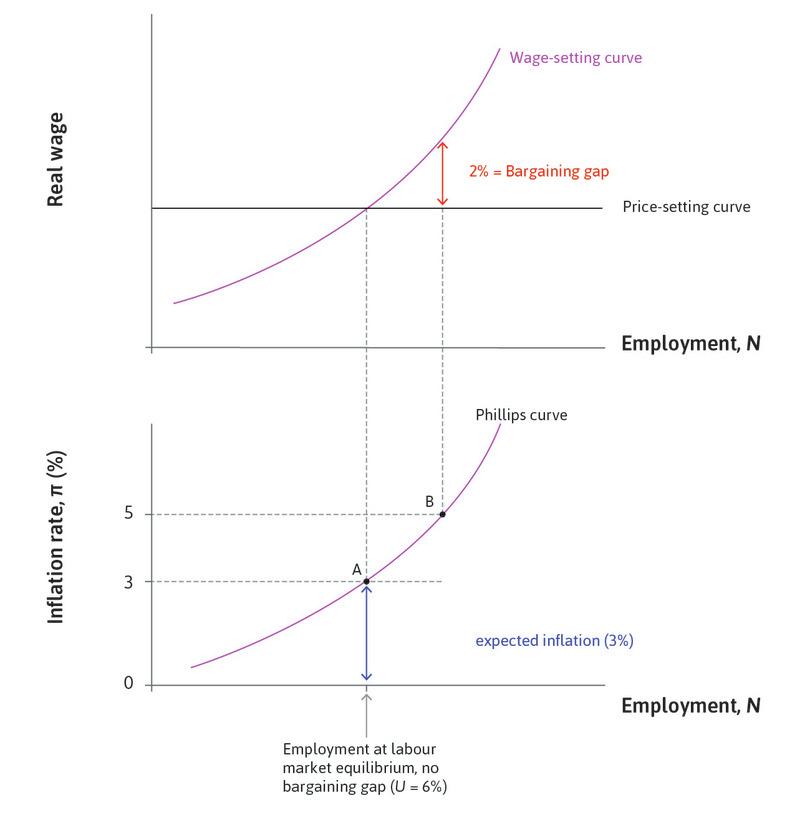

We now use the labour market diagram to show what happens in a boom, when unemployment is lower than at A. Figure 15.4b shows how workers’ claims to real wages and firms’ claims to real profits sum to more than total productivity when unemployment is below equilibrium, and sum to less than total productivity when unemployment is above equilibrium. When unemployment is below equilibrium this leads to upwards pressure on wages and prices, or a rising wage-price spiral. When unemployment is above equilibrium it leads to downwards pressure on wages and prices, or a declining wage-price spiral.

If we sketch the relationship between inflation and unemployment from the three phases of the business cycle, we get something similar to the one Phillips discovered in the data: when unemployment is lower, inflation is higher and vice versa.

Inflation and conflict over the pie at low and high unemployment.

Figure 15.4b Inflation and conflict over the pie at low and high unemployment.

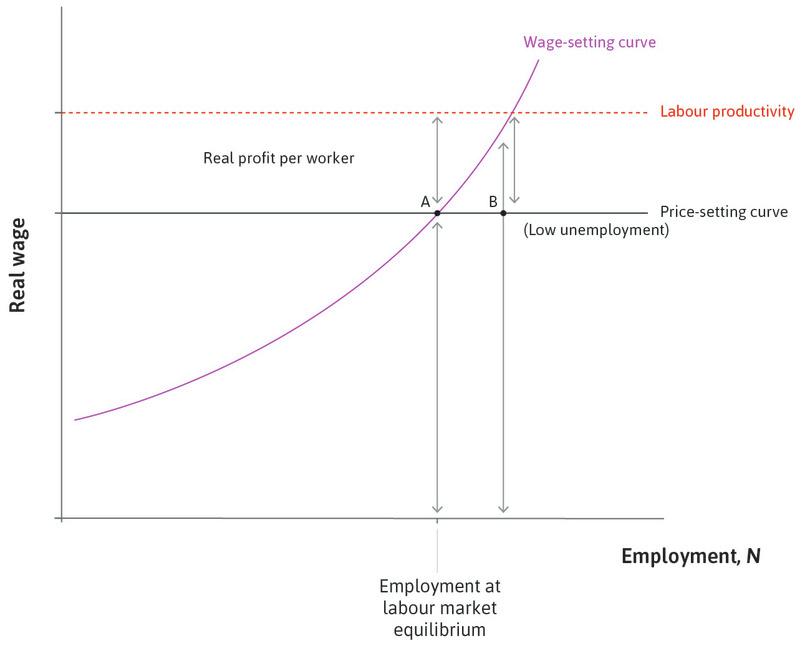

Labour market equilibrium at A

At A, the economy is at labour market equilibrium. The real wage on the wage-setting curve is equal to that on the price-setting curve, so firms’ claims to real profit per worker plus the workers’ claims to real wages sum to labour productivity.

Figure 15.4ba At A, the economy is at labour market equilibrium. The real wage on the wage-setting curve is equal to that on the price-setting curve, so firms’ claims to real profit per worker plus the workers’ claims to real wages sum to labour productivity.

Low unemployment at B

At low unemployment, the real wage required so that workers will work hard increases so the claims of workers for wages and owners for profits are inconsistent: they sum to more than labour productivity.

Figure 15.4bb At low unemployment, the real wage required so that workers will work hard increases so the claims of workers for wages and owners for profits are inconsistent: they sum to more than labour productivity.

High unemployment at C

At high unemployment, workers are in a weaker bargaining position. The claims of workers and owners sum to less than labour productivity.

Figure 15.4bc At high unemployment, workers are in a weaker bargaining position. The claims of workers and owners sum to less than labour productivity.

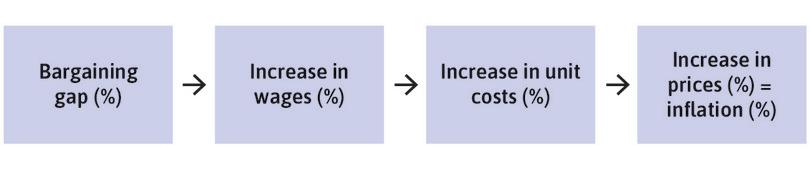

- bargaining gap

- The difference between the real wage that firms wish to offer in order to provide workers with incentives to work, and the real wage that allows firms the markup that maximizes profits given the degree of competition.

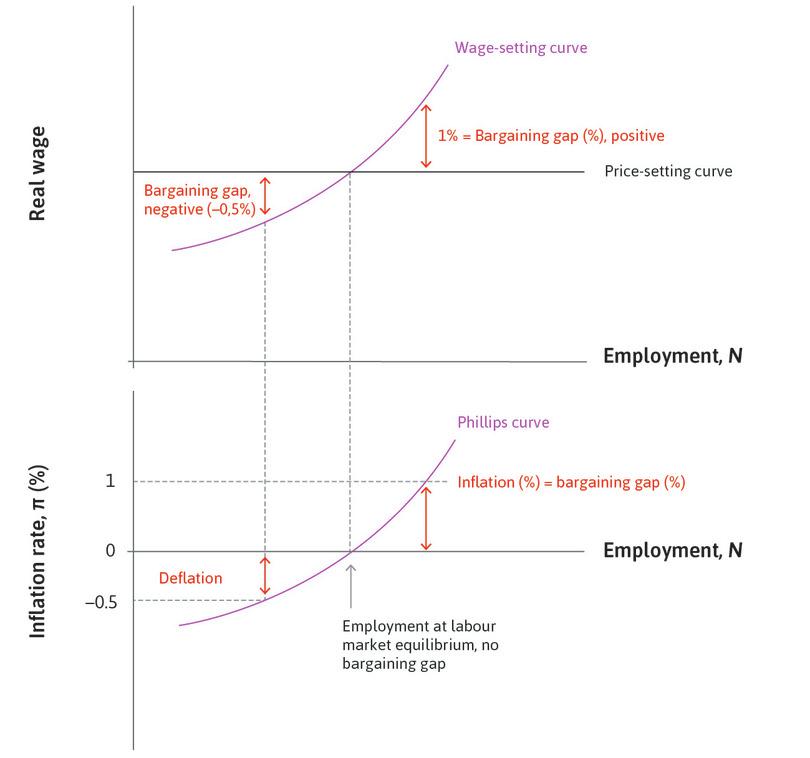

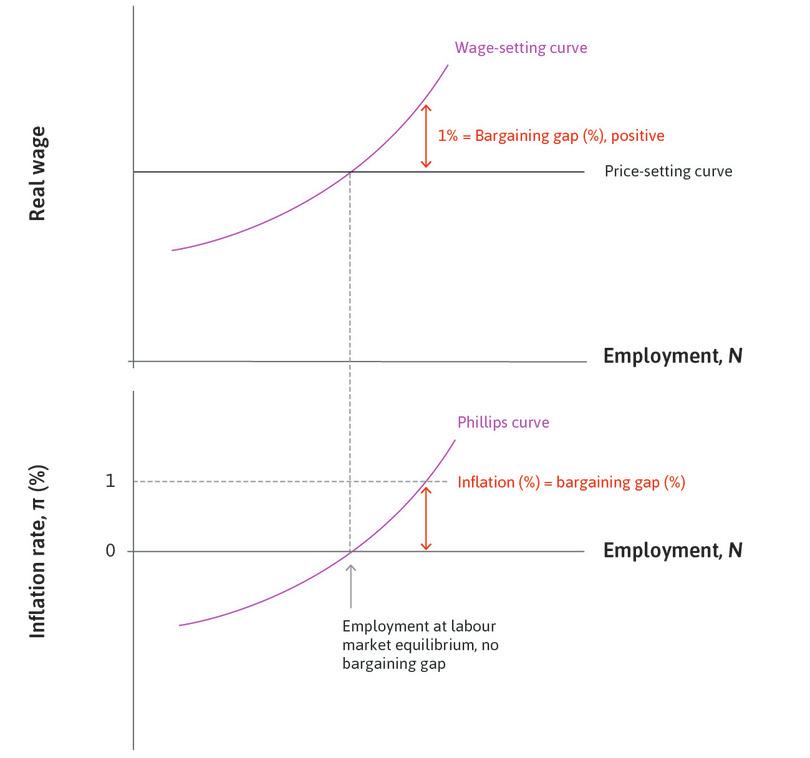

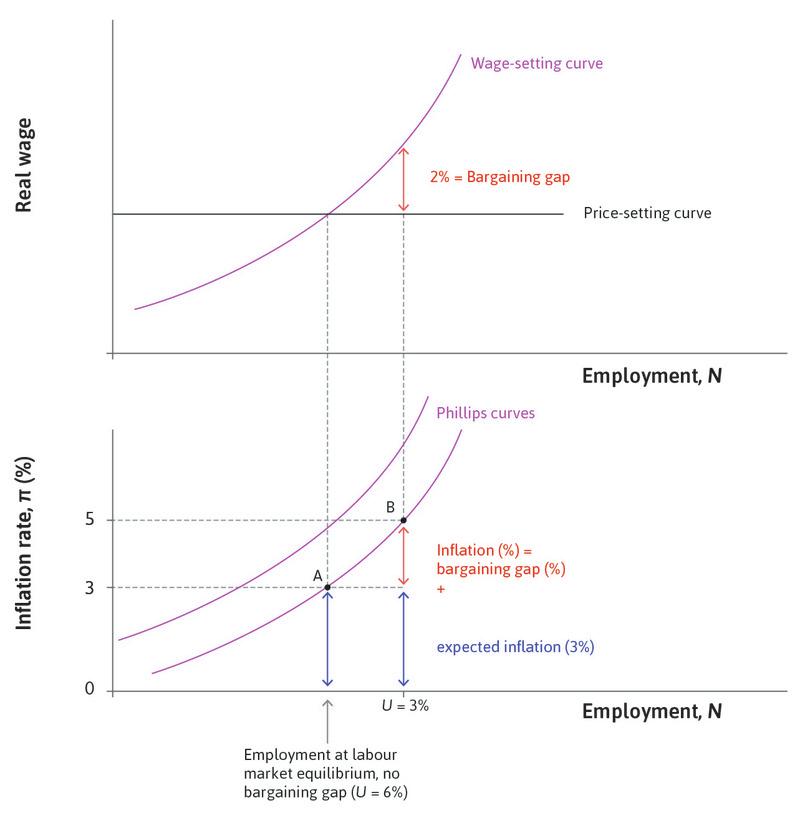

The big message from the model of inflation and conflict over the pie is that if employment is above or below the labour market equilibrium then the price level is either rising or falling. When the real wage given by the wage-setting curve and that given by the price-setting curve are not equal, we say there is a bargaining gap equal to the vertical distance between the two curves.

- If unemployment is lower than at the equilibrium: There is a positive bargaining gap and there is inflation.

- If unemployment is higher than at the equilibrium: There is a negative bargaining gap and there is deflation.

- If there is labour market equilibrium: The bargaining gap is zero and the price level is constant.

For example, if the wage on the price-setting curve is 100 and on the wage-setting curve it is 101, the bargaining gap is 1%.

The bargaining gap and the Phillips curve

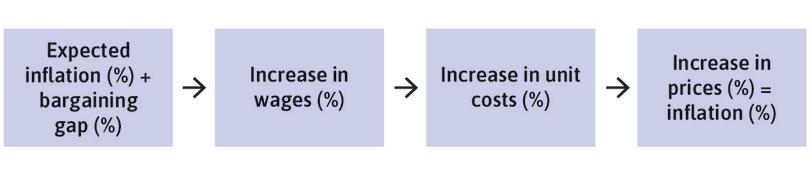

We can summarize the causal chain from the bargaining gap to inflation like this:

Remember, the triple bar indicates that inflation is defined as the percentage increase in prices. So, to work out the inflation rate, we use the following:

Bargaining gap

The difference between the real wage that firms wish to offer in order to provide workers with incentives to work (the wage-setting curve), and the real wage that allows firms the markup on costs required to motivate them to continue in business (the price-setting curve).

- When the bargaining gap is positive, the real wage on the wage-setting curve is above the price-setting curve, and the claims of employers and owners to output per worker are inconsistent.

- The percentage bargaining gap is equal to the wage on the wage-setting curve, minus the wage on the price-setting curve, divided by the wage on the price-setting curve.

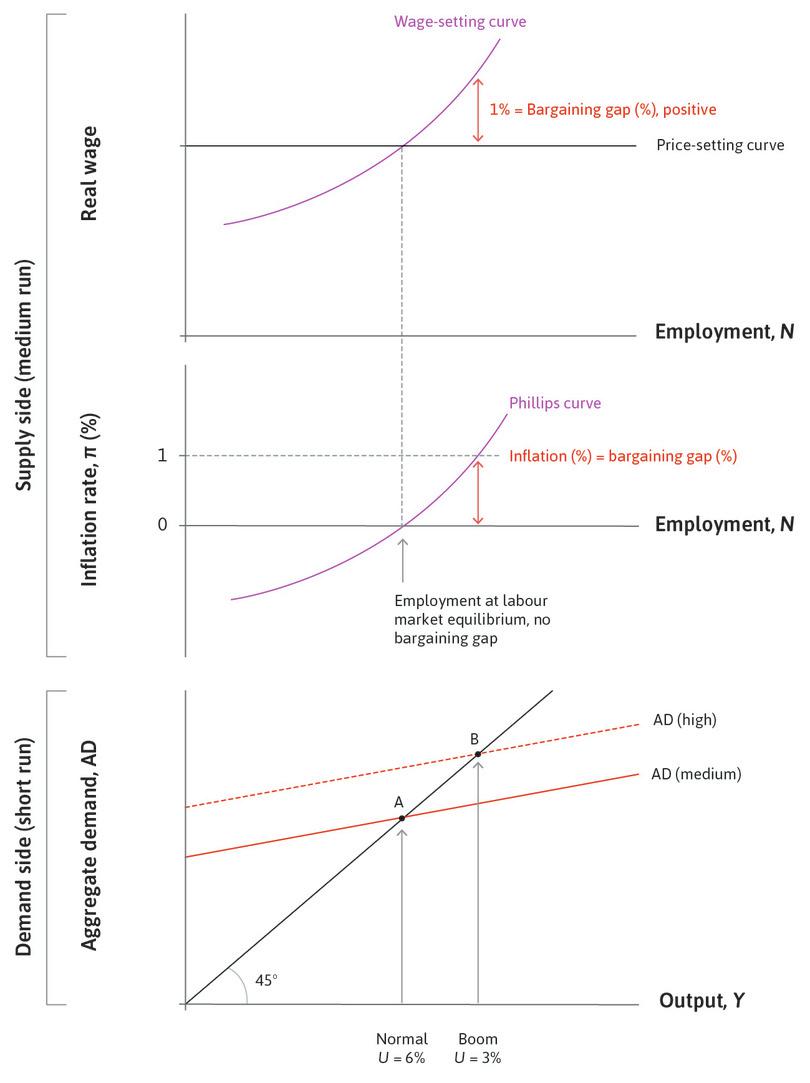

In Figure 15.4c, we draw a new diagram beneath the wage-setting curve and price-setting curve. This is the Phillips curve diagram, with inflation on the vertical axis and employment on the horizontal axis. If we begin with employment at the labour market equilibrium, and inflation of zero, we note that the economy can remain here: there is no pressure for the price level to rise or fall. This gives a point on the Phillips curve. Now consider a higher level of employment due to stronger aggregate demand. A positive bargaining gap opens up and wages and prices will rise. Firms increase wages in response to the fall in unemployment. The price level rises as firms put up their prices in response to the rise in their labour costs. If the bargaining gap is 1%, prices and wages will rise by 1%. This gives a second point on the Phillips curve.

Bargaining gaps, inflation, and the Phillips curve.

Figure 15.4c Bargaining gaps, inflation, and the Phillips curve.

Labour market equilibrium

The bargaining gap is zero and inflation is zero.

Figure 15.4ca The bargaining gap is zero and inflation is zero.

Low unemployment

The bargaining gap is positive and inflation is positive.

Figure 15.4cb The bargaining gap is positive and inflation is positive.

High unemployment

The bargaining gap is negative and inflation is negative.

Figure 15.4cc The bargaining gap is negative and inflation is negative.

As long as employment remains above the labour market equilibrium, employees will be disappointed at the end of the year. Their real wage will not have risen by 1% as they had anticipated, so they will bargain for another 1% rise. The result: wages and prices will rise by 1% the following year as well: firms will put up wages by 1% to take the real wage up to the wage-setting curve, and they will put up prices by 1% in response to that cost increase. We will observe lower unemployment and higher inflation as in Phillips’ original empirical scatter plot.

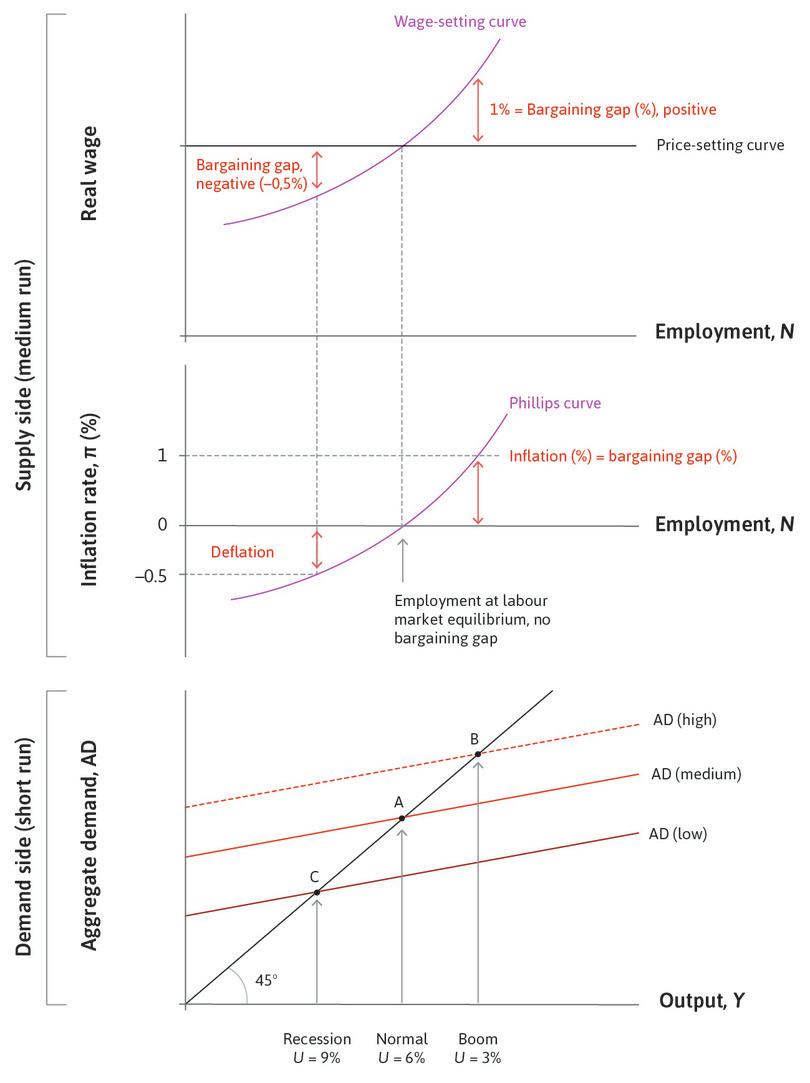

To complete the picture, we include the multiplier model beneath the labour market and Phillips diagrams to bring the short- and medium-run models together. This highlights that:

- At a higher level of aggregate demand (a boom) inflation is positive: Unemployment is lower, which means there is a positive bargaining gap, so wages and prices are rising continuously.

- At a lower level of aggregate demand (a recession), there is deflation: Unemployment is higher, which means there is a negative bargaining gap.

The short- and medium-run models: Aggregate demand, employment, and inflation.

Figure 15.4d The short- and medium-run models: Aggregate demand, employment, and inflation.

Labour market equilibrium

When the level of aggregate demand produces employment at labour market equilibrium (a normal level of activity), the price level is stable (inflation is zero).

Figure 15.4da When the level of aggregate demand produces employment at labour market equilibrium (a normal level of activity), the price level is stable (inflation is zero).

A boom

At a higher level of aggregate demand (a boom), there is a positive bargaining gap and inflation is positive.

Figure 15.4db At a higher level of aggregate demand (a boom), there is a positive bargaining gap and inflation is positive.

A recession

At a lower level of aggregate demand (a recession), there is a negative bargaining gap and deflation.

Figure 15.4dc At a lower level of aggregate demand (a recession), there is a negative bargaining gap and deflation.

Exercise 15.1 The bargaining gap in a recession

Suppose the economy is initially at labour market equilibrium with stable prices (inflation is zero). At the beginning of year 1, investment declines and the economy moves into recession with high unemployment.

- Explain why a negative bargaining gap arises.

- Assume the negative bargaining gap is 1%. Draw a diagram with years on the horizontal axis and the price level on the vertical axis. Starting from a price index of 100, sketch the path of the price level for the 5 years that follow, assuming the bargaining gap remains at –1%.

- Who are the winners and losers in this economy?

Exercise 15.2 Positive and negative shocks

Draw a labour market diagram where the economy is at labour market equilibrium with stable prices. Now consider:

- A positive shock to aggregate demand that reduces the unemployment rate by 2 percentage points.

- A negative shock that increases it by 2 percentage points.

- What happens to the bargaining gap in each case?

- What would you expect to happen to the price level in each case? Explain your answers.

Question 15.5 Choose the correct answer(s)

See Figure 15.4d for diagrams of the labour market model, the Phillips curve, and the multiplier model of aggregate demand. The unemployment rates and the bargaining gaps at different states of the economy are shown.

Based on this information, which of the following statements is correct?

- There is always a positive rate of unemployment in the labour market model (see Unit 9). If U is below 3%, then there would be an even larger positive bargaining gap than with U = 3 and even higher inflation. Inflation is zero in the diagram only when the unemployment rate is 6%.

- At point B unemployment is below the labour market equilibrium, creating a positive bargaining gap.

- The bargaining gap created as a result of the recession is –0.5%, which is negative.

- The Phillips curve shows a positive correlation between employment and the inflation rate, which means a negative correlation between the unemployment rate and the inflation rate.

15.4 Inflation and unemployment: Constraints and preferences

Phillips’ original curve, and the model in Figure 15.4d, suggest that there is a lasting trade-off between inflation and unemployment. For example, with the Phillips curve in the figure, if the government is happy to have inflation of 1% each year, then it can support a boom level of aggregate demand with an unemployment rate of 3% year after year.

- feasible set

- All of the combinations of the things under consideration that a decision-maker could choose given the economic, physical or other constraints that he faces. See also: feasible frontier.

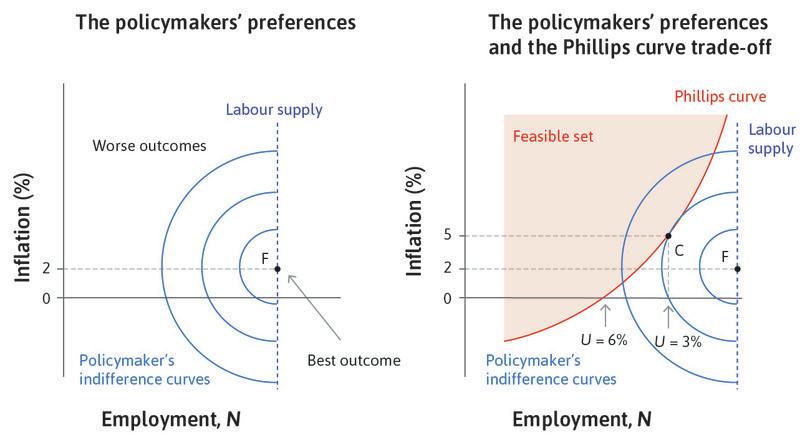

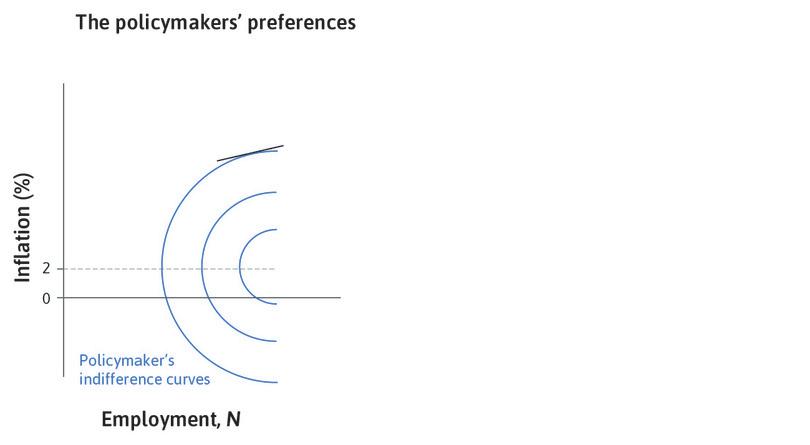

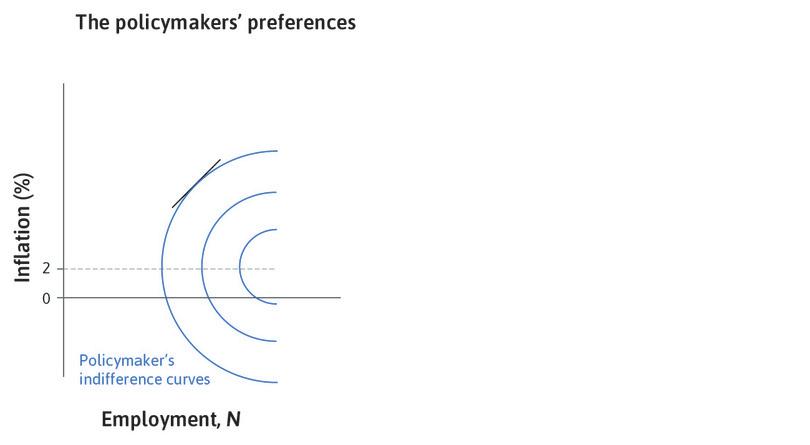

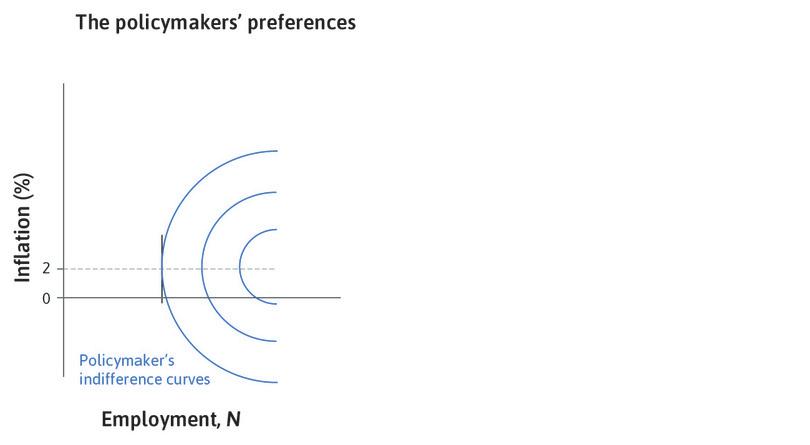

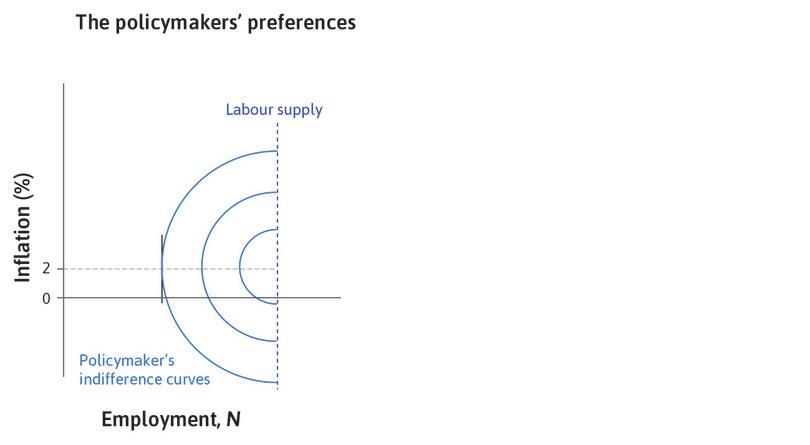

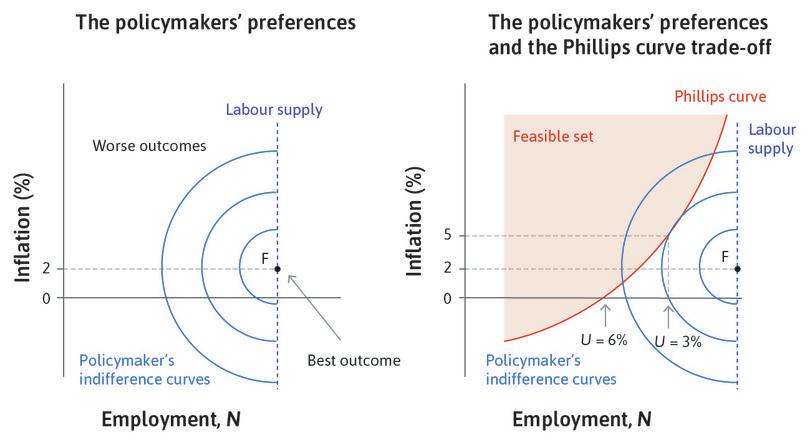

If it prefers stable prices (zero inflation), then it needs to keep aggregate demand at the normal level, with unemployment of 6%. This suggests that the Phillips curve is a feasible set from which the policymaker can select the desired combination of unemployment and inflation. The policymaker prefers low inflation and high employment, and those preferences can be represented in the usual way in the form of indifference curves.

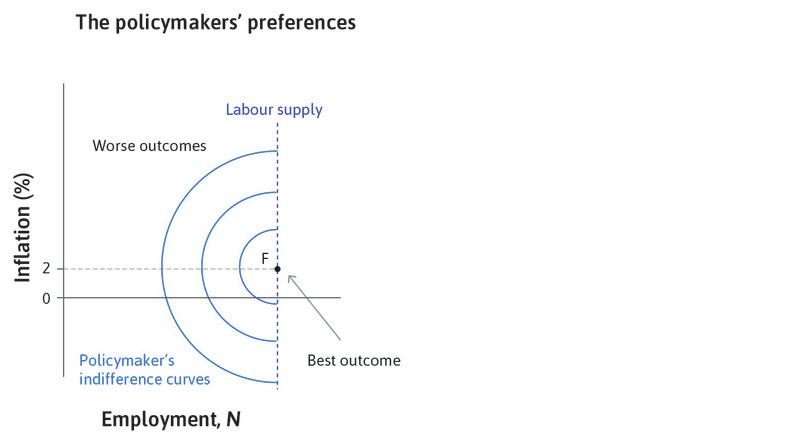

Work through the steps of the analysis in Figure 15.5 to see how the policymaker’s preferences are described by indifference curves.

Note first some important features of the diagram. Typically when drawing indifference curves, a choice further from the origin is preferred since more of what is on each axis is preferred. In this case, the policymaker’s best outcome is shown by point F, with inflation at the target and full employment. As we saw at the end of Section 15.1, the policymaker is likely to prefer low (stable) inflation to zero. This means the indifference curves become vertical at, say, 2% inflation. Above target inflation, the indifference curves are positively sloped, as getting employment closer to full employment is worth accepting higher (above target) inflation. Below the target, the indifference curves are negatively sloped, as getting employment closer to full employment is worth accepting lower (below target) inflation.

We assume that there are diminishing marginal returns to the two targets of high employment and low inflation. This implies that when the outcome is further from the inflation target but closer to full employment, the indifference curve is flatter because the policymaker places more value on getting closer to the inflation target. Conversely, when the outcome is further from full employment but closer to the inflation target, the indifference curve is steeper because the policymaker places more value on getting closer to full employment.

The Phillips curve and the policymaker’s preferences.

Figure 15.5 The Phillips curve and the policymaker’s preferences.

The policymaker’s preferences

The figure shows the policymaker’s indifference curves.

Figure 15.5a The figure shows the policymaker’s indifference curves.

High employment and inflation

When employment and inflation are very high, the indifference curve is flat.

Figure 15.5b When employment and inflation are very high, the indifference curve is flat.

Lower employment and inflation

When inflation and employment are lower, the indifference curve is steeper.

Figure 15.5c When inflation and employment are lower, the indifference curve is steeper.

Inflation at 2%

The indifference curve is vertical when inflation is at 2%.

Figure 15.5d The indifference curve is vertical when inflation is at 2%.

Full employment

The indifference curve is horizontal when employment = labour supply.

Figure 15.5e The indifference curve is horizontal when employment = labour supply.

The policymaker’s preferred outcome

F marks the policymaker’s preferred combination of inflation and unemployment.

Figure 15.5f F marks the policymaker’s preferred combination of inflation and unemployment.

The feasible set

The policymaker chooses from the feasible set on the Phillips curve.

Figure 15.5g The policymaker chooses from the feasible set on the Phillips curve.

The preferred feasible outcome

This is on the Phillips curve at point C.

Figure 15.5h This is on the Phillips curve at point C.

In the right-hand panel of the figure, the indifference curves and the Phillips curve are shown. The policymaker sees the Phillips curve as the feasible set and will try to use monetary or fiscal policy to choose the level of aggregate demand so that employment is at C. This is the indifference curve closest to the best outcome of F, which is consistent with the Phillips curve trade-off.

In this example, the policymaker prefers a combination of unemployment of 3% and inflation of 5% to another feasible combination of unemployment of 6% and a stable price level (zero inflation).

Exercise 15.3 The Phillips curve and the policymaker’s preferences

The following questions refer to Figure 15.5.

- What would the policymaker’s indifference curves look like if the policymaker cared only about low unemployment?

- Which point on the Phillips curve would that policymaker choose?

- What would the policymaker’s indifference curves look like if the policymaker cared only about low inflation?

- Which point on the Phillips curve would this policymaker choose?

- What would the indifference curves look like if, to be re-elected, the policymaker needed the support of pensioners more than that of working-age people?

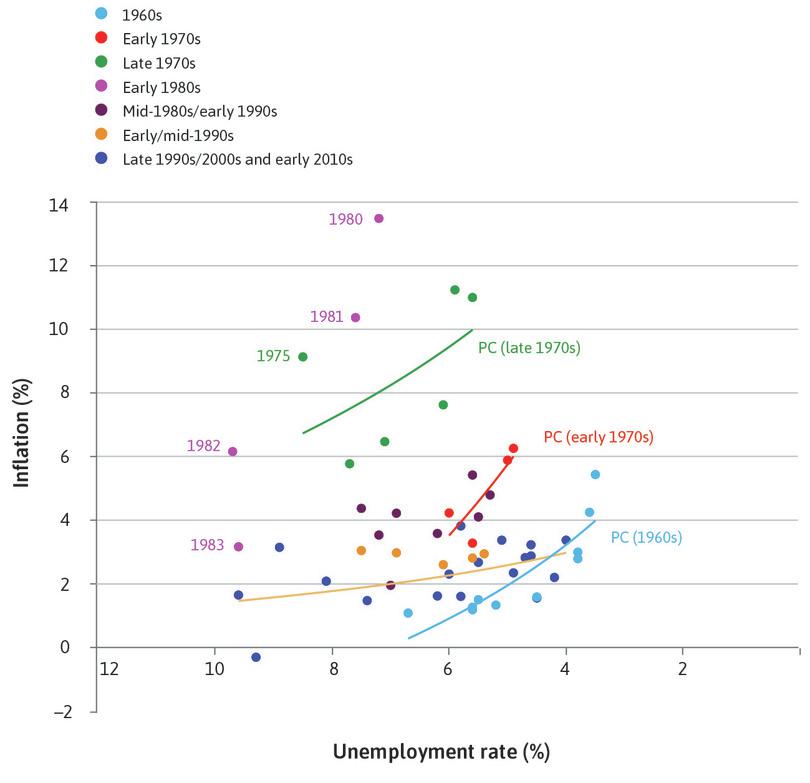

15.5 What happened to the Phillips curve?

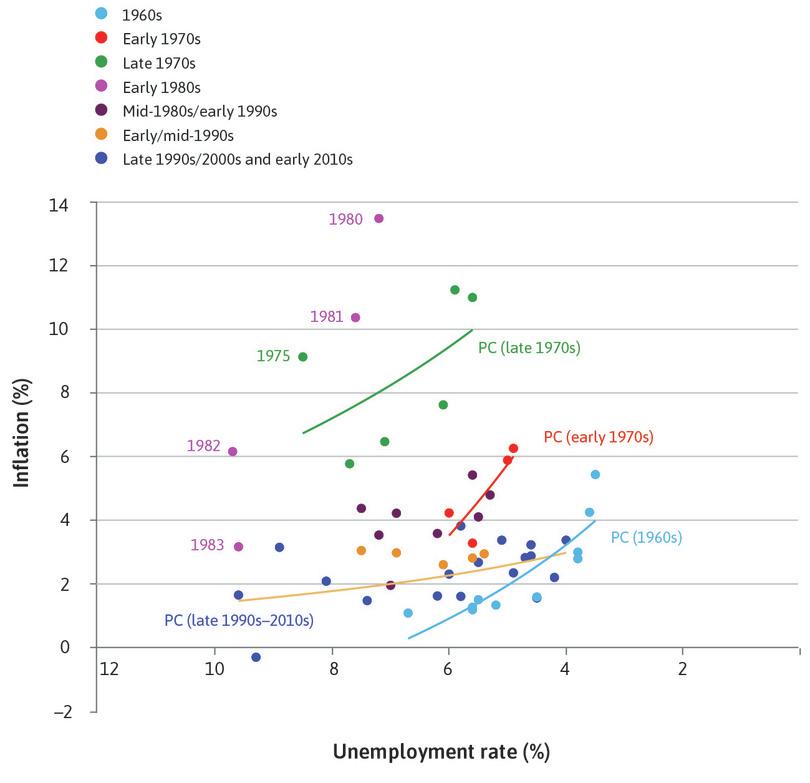

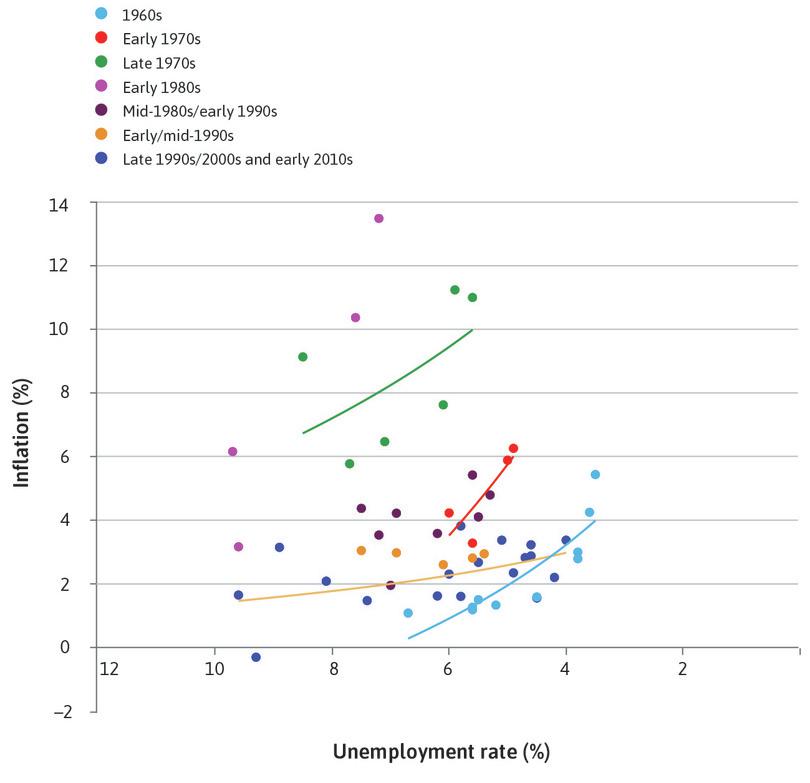

The model in Figure 15.5 suggests that a policymaker who is able to adjust the level of aggregate demand can pick any combination of inflation and unemployment along the Phillips curve. But the data in Figure 15.6 suggests that the trade-off between inflation and unemployment is not a stable one. There is a mass of data points and no discernible, positively sloped Phillips curve.

Figure 15.6 shows the inflation and unemployment combinations for the US for each year between 1960 and 2014. Note that on the horizontal axis, the scale for the unemployment rate declines as we move to the right in the figure. A Phillips curve sketched through the observations in the 1960s gives a reasonably good picture of the inflation-unemployment trade-off in that decade. But that curve clearly does not fit in other periods. The figure shows how the Phillips curve changed over time.

Phillips curves in the US (1960–2014).

Figure 15.6 Phillips curves in the US (1960–2014).

Federal Reserve Bank of St. Louis. 2015. FRED.

Where is the Phillips curve?

The figure shows the inflation and unemployment combinations for the US for each year between 1960 and 2014.

Figure 15.6a The figure shows the inflation and unemployment combinations for the US for each year between 1960 and 2014.

Federal Reserve Bank of St. Louis. 2015. FRED.

A shifting curve

We can use the figure to show how the Phillips curve shifted over time.

Figure 15.6b We can use the figure to show how the Phillips curve shifted over time.

Federal Reserve Bank of St. Louis. 2015. FRED.

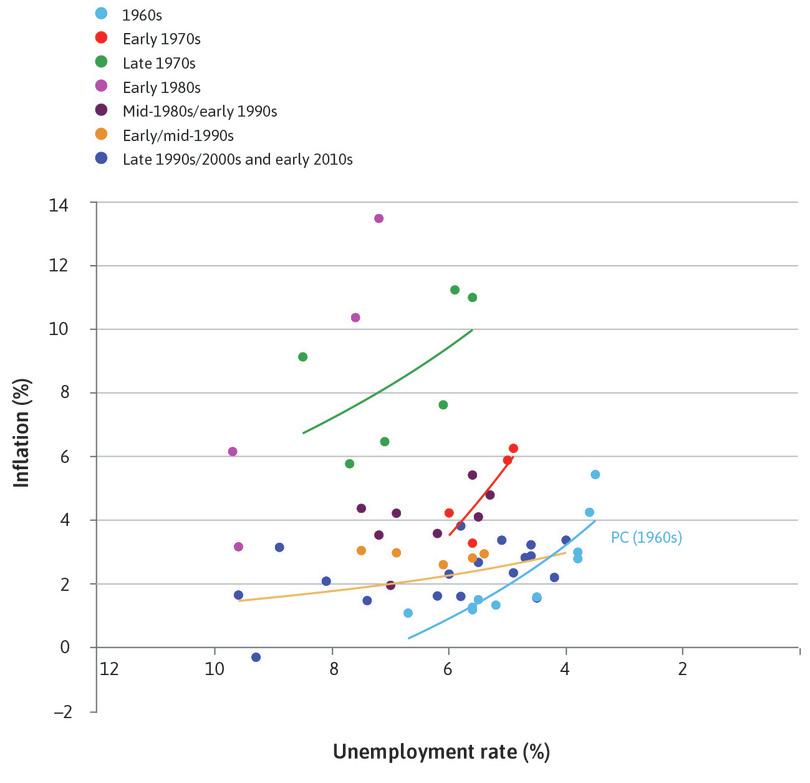

The 1960s

The Phillips curve (PC) for the 1960s shows the economy was in a good state. The US could achieve combinations of relatively low inflation and unemployment.

Figure 15.6c The Phillips curve (PC) for the 1960s shows the economy was in a good state. The US could achieve combinations of relatively low inflation and unemployment.

Federal Reserve Bank of St. Louis. 2015. FRED.

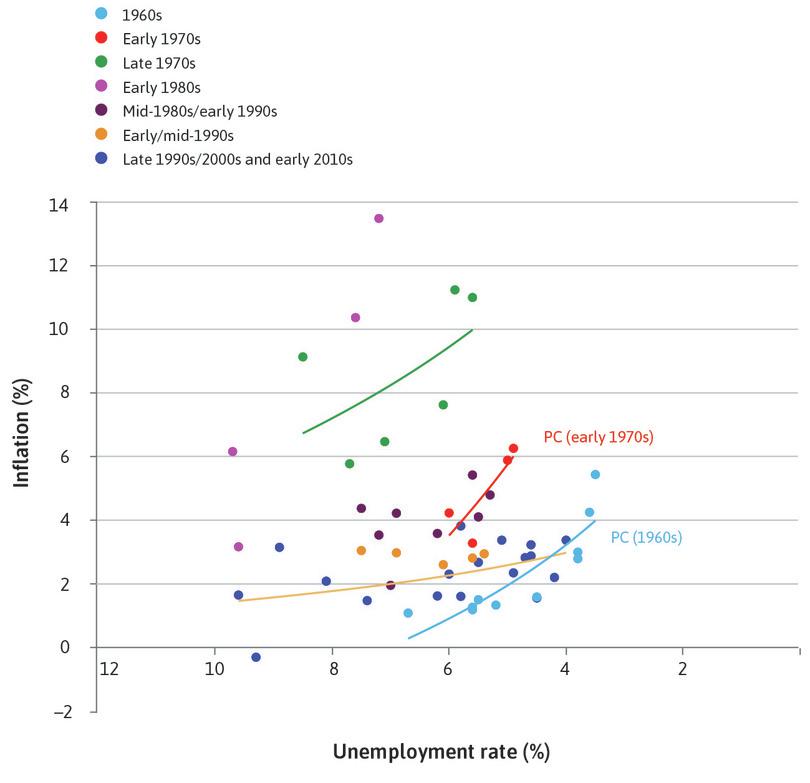

The 1970s

In the early 1970s, the Phillips curve appears to have shifted up.

Figure 15.6d In the early 1970s, the Phillips curve appears to have shifted up.

Federal Reserve Bank of St. Louis. 2015. FRED.

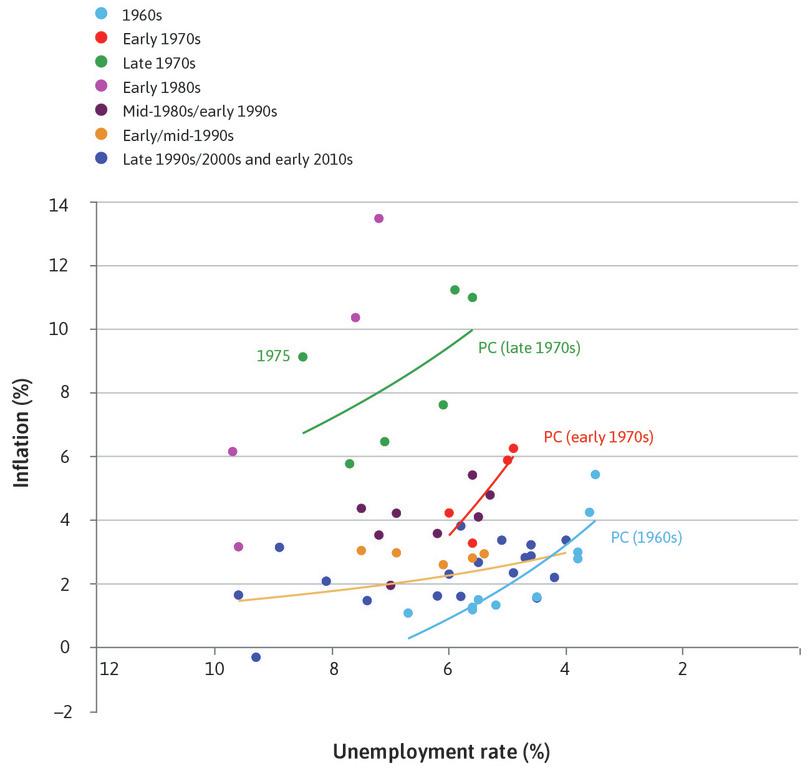

The 1970s

The curve shifts up again in the late 1970s.

Figure 15.6e The curve shifts up again in the late 1970s.

Federal Reserve Bank of St. Louis. 2015. FRED.

The 1980s

And up again in the early 1980s, further worsening the trade-off between unemployment and inflation.

Figure 15.6f And up again in the early 1980s, further worsening the trade-off between unemployment and inflation.

Federal Reserve Bank of St. Louis. 2015. FRED.

The 1990s

In the late 1990s to the present, the Phillips curve is low and flat.

Figure 15.6g In the late 1990s to the present, the Phillips curve is low and flat.

Federal Reserve Bank of St. Louis. 2015. FRED.

In his presidential address to the American Economic Association in December 1967, Milton Friedman provided an explanation for why the Phillips curve is not stable. He referred to the recent experience in the US. Since 1966 unemployment had been steady, averaging 3.7%, but inflation had increased from 3.0% to 4.2%. He said that the only way unemployment could be kept as low as 3% was by allowing inflation to keep increasing: ‘There is always a temporary trade-off between inflation and unemployment; there is no permanent trade-off,’ he claimed.3 This is what Helmut Schmidt knew, but did not want to admit to the voters, in 1972.

If there is no permanent trade-off, then the Phillips curve is not a feasible set in the same way as the feasible consumption frontier was: the feasible consumption frontier stays in place when a different point on it is chosen. By contrast, Friedman, supported by evidence from many countries from the late 1960s, showed that if a government tries to keep unemployment ‘too low’ the result will be not just higher inflation, but rising inflation as well.

Inflation means rising prices. Rising inflation means prices increasing at an ever-faster rate. This means that the Phillips curve would keep shifting upward.

15.6 Expected inflation and the Phillips curve

We now explain why the Phillips curve shifts: why does inflation keep rising when governments try to keep unemployment too low? We will show that there is only one unemployment rate at which inflation is stable, and that this is the labour market Nash equilibrium.

We need to go back to two familiar points:

- People are forward-looking: We explained this in Units 6, 9, 10 and 13. They take actions now in anticipation of things they expect to happen. To stress this, economists say that ‘expectations matter’.

- People treat prices as messages: Friedrich Hayek taught us this (see Unit 11). Therefore people also treat changes in prices as messages about what will happen in the future, just as people treat a build-up of clouds as a prediction of rain.

- expected inflation

- The opinion that wage- and price-setters form about the level of inflation in the next period. See also: inflation.

With these two building blocks, we can see why Friedman was right. As well as the battle for the pie between workers and the owners of firms that is the fundamental cause of rising prices, Friedman showed that, at low unemployment, inflation keeps increasing. This is because of the way that wage- and price-setters form their views about what will happen to inflation, which is called expected inflation. The behaviour of inflation will reflect both elements.

Introducing expected inflation

We introduce the role of expected inflation by returning to the Phillips curve.

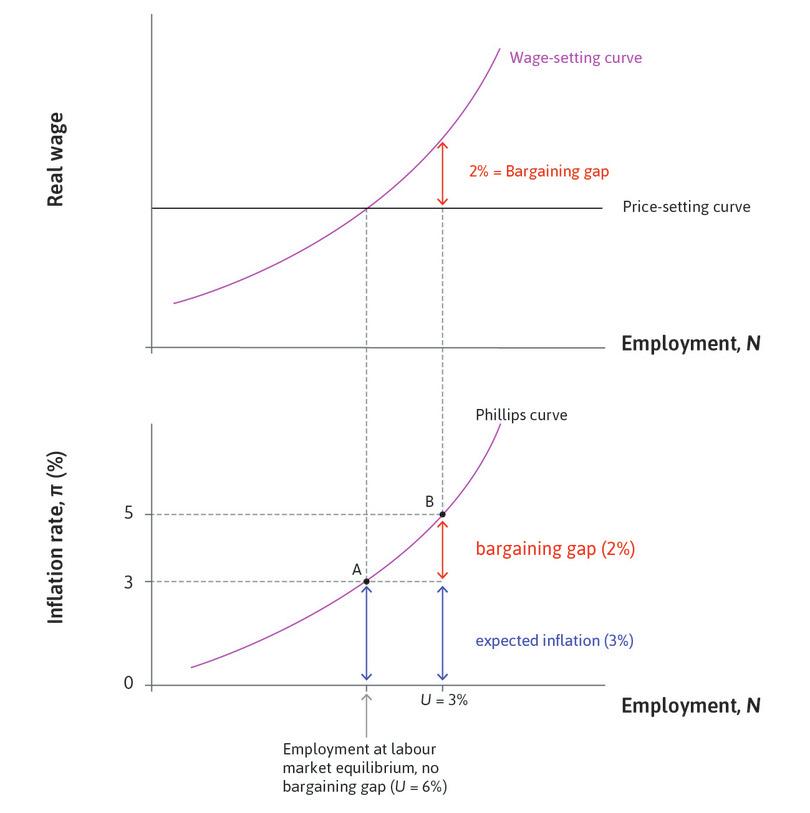

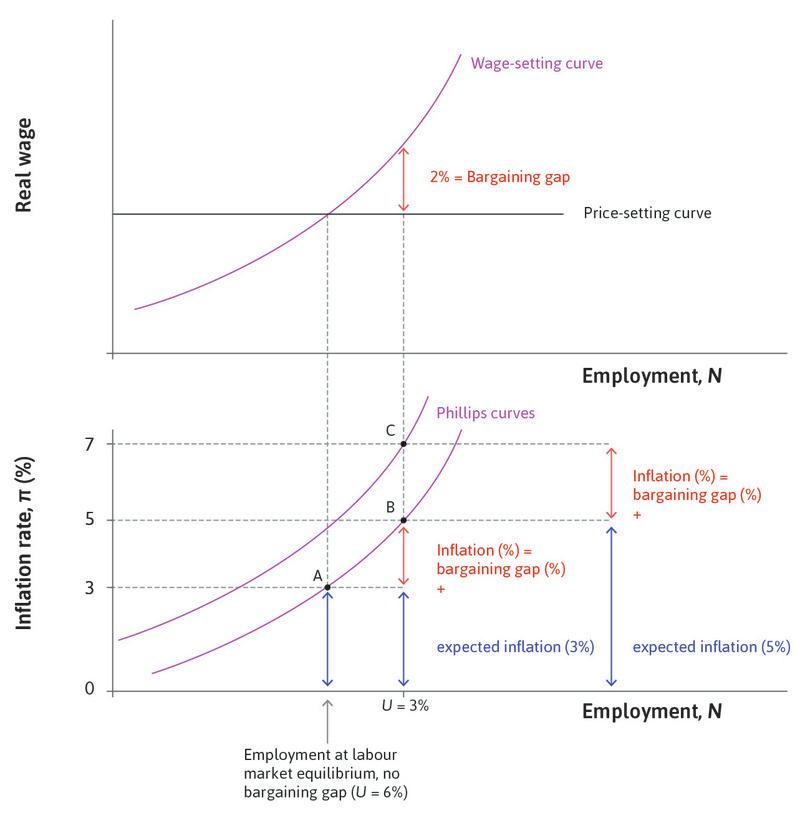

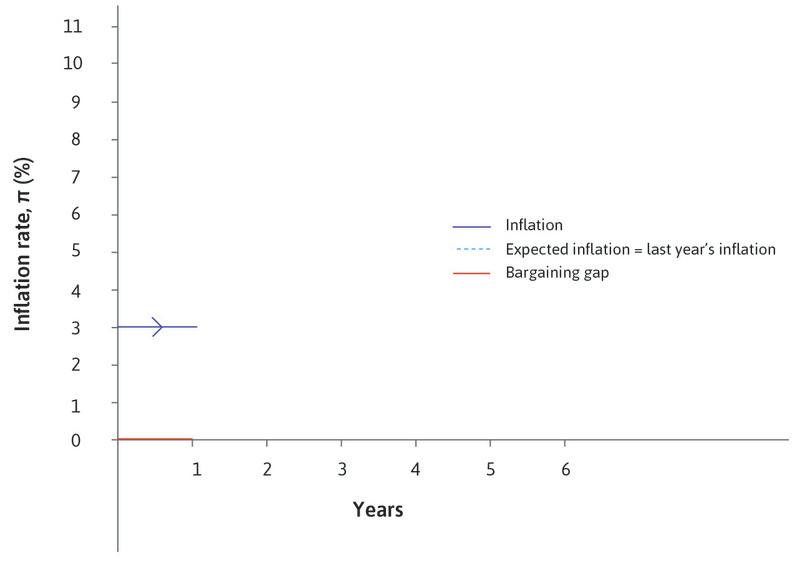

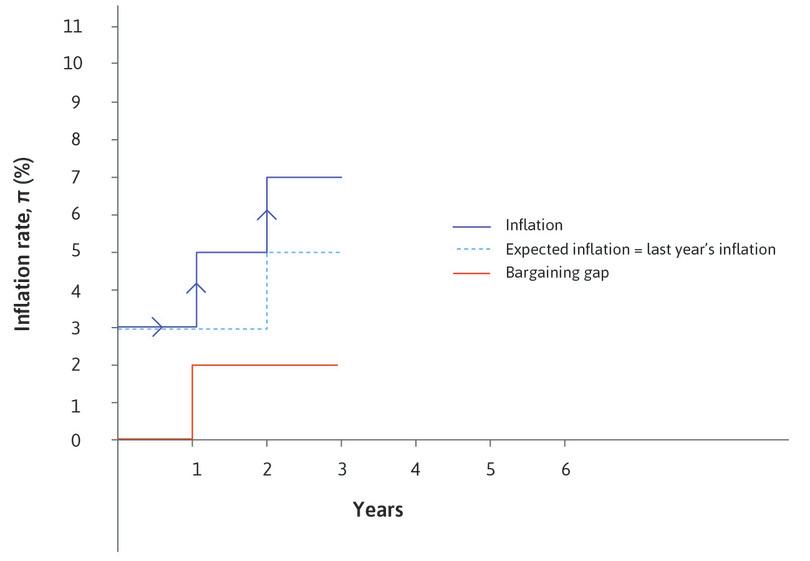

Look at Figure 15.7. You will notice that at the labour market equilibrium with an unemployment rate of 6%, the inflation rate is 3% and not zero as in Figure 15.4d.

If wage- and price-setters expect prices to rise by 3% per annum, and the level of aggregate demand is ‘normal’ and keeps unemployment at 6%, then the economy can remain at the labour market equilibrium with inflation remaining constant at 3% per annum. Every year, wages and prices will rise by 3% and the real wage will remain at the intersection of the wage- and price-setting curves. This is point A.

Bargaining gaps, expected inflation, and the Phillips curve.

Figure 15.7 Bargaining gaps, expected inflation, and the Phillips curve.

Labour market equilibrium

At labour market equilibrium, inflation is 3% as expected.

Figure 15.7a At labour market equilibrium, inflation is 3% as expected.

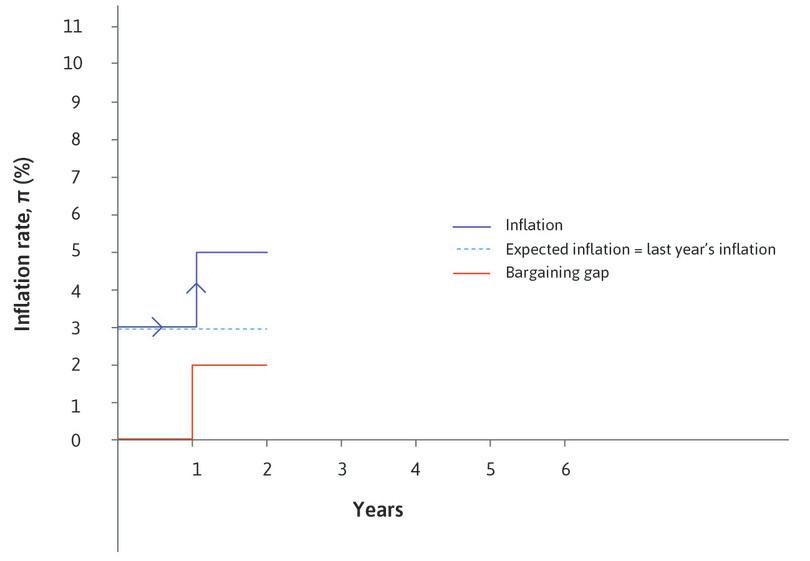

A boom

At lower unemployment, the bargaining gap is 2%.

Figure 15.7b At lower unemployment, the bargaining gap is 2%.

The new rate of inflation, 5%

At B, inflation is equal to expected inflation plus the bargaining gap.

Figure 15.7c At B, inflation is equal to expected inflation plus the bargaining gap.

Now consider a boom, which takes the economy to lower unemployment at point B. What will happen to inflation? Workers expect prices to rise by 3% and will require a nominal wage increase of 3% just to keep their real wage unchanged. But they require an additional 2% rise to give them an expected real wage rise on the wage-setting curve, so wages increase by 5%. With their costs rising by 5%, firms will increase prices by 5%. In the boom, inflation will be 5%. This gives a Phillips curve like the one we have seen before. The only difference is that inflation at labour market equilibrium is 3% rather than zero.

When inflation is not zero, we can summarize the causal chain from expected inflation and the bargaining gap to inflation like this:

To work out the inflation rate:

But Friedman pointed out that with low unemployment, inflation would not remain at 5% at point B. To see why, we ask what happens next.

The shifting Phillips curve

With low unemployment continuing, workers will be disappointed with the outcome, since they did not achieve their expected real wage. Why not? Workers expected a 2% real wage increase at B from their nominal pay rise of 5% (to give the real wage on the wage-setting curve), but they did not get this because firms raised their prices by 5%.

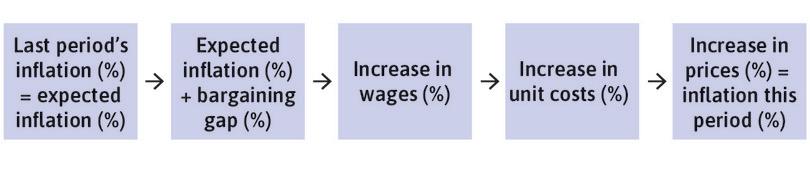

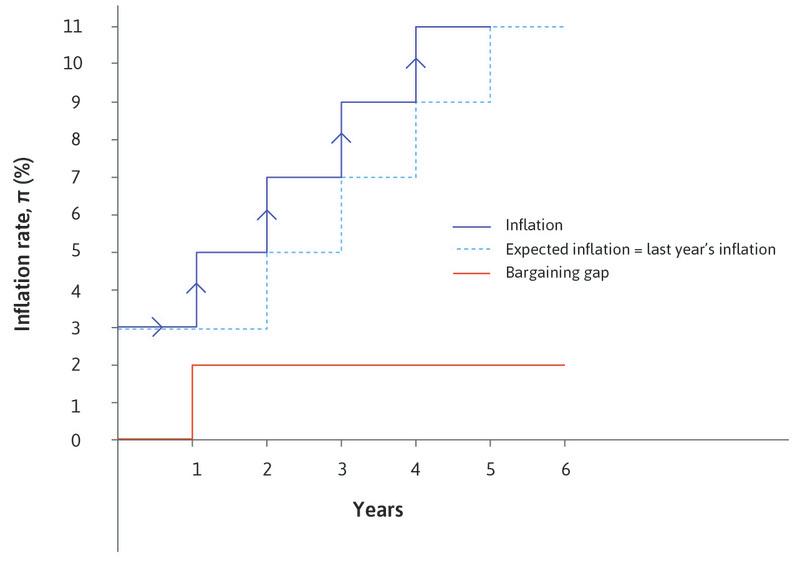

But the story does not end there. We know that both parties cannot be satisfied with the outcome at low unemployment, because their claims add up to more than the size of the pie. Now, we assume that workers expect inflation next year to be equal to inflation last year. So at the next wage-setting round, the human resources department has to take into account the fact that their employees expect prices to rise by 5%. Another interpretation is that HR includes inflation over the past year in the wage settlement, to make up for the shortfall in the real wage that workers experienced because inflation turned out to be higher than expected. So in order to achieve another real wage increase of 2%, the HR department sets a wage increase of 7%. The process continues with the rate of inflation increasing over time.

The table in Figure 15.8 summarizes the situation. We compare the situation over a three-year period with unemployment at two levels: 6% and 3%.

| Year | Expected inflation (previous year's inflation) | Unemployment | Bargaining gap | Inflation outcome: expectations plus bargaining gap | |

|---|---|---|---|---|---|

| Stable inflation | 1 | 3% | 6% | 0% | 3% |

| 2 | 3% | 6% | 0% | 3% | |

| 3 | 3% | 6% | 0% | 3% | |

| Rising inflation | 1 | 3% | 3% | 2% | 5% |

| 2 | 5% | 3% | 2% | 7% | |

| 3 | 7% | 3% | 2% | 9% |

Unstable Phillips curves: Expected inflation and the bargaining gap.

Figure 15.8 Unstable Phillips curves: Expected inflation and the bargaining gap.

The first column of Figure 15.8 reflects forward-looking behaviour. Expected inflation over the year ahead is based on the previous year’s inflation. The second column shows the unemployment rate. The third column shows the bargaining gap. The fourth column is the inflation outcome, which reflects expectations and the bargaining gap.

We can summarize the causal chain from the last period’s inflation rate to this period’s inflation rate like this:

To work out the inflation rate:

We can show the data in the table in Figure 15.8 and in the Phillips curve and labour market diagrams in Figure 15.9. The stable inflation case is at point A with unemployment of 6% and inflation of 3%, year after year. At low unemployment (3%), the Phillips curve shifts up from the one through point B to the one through point C when expected inflation rises from 3% to 5%.

Inflation expectations and Phillips curves.

Figure 15.9 Inflation expectations and Phillips curves.

Labour market equilibrium at A

Inflation is 3% as expected.

Figure 15.9a Inflation is 3% as expected.

A boom: First period at B

At lower unemployment, the bargaining gap is 2%. Inflation is equal to expected inflation plus the bargaining gap.

Figure 15.9b At lower unemployment, the bargaining gap is 2%. Inflation is equal to expected inflation plus the bargaining gap.

A boom: Next period at C

Next period, with unemployment still low at 3%, inflation is equal to expected inflation plus the bargaining gap. The Phillips curve has shifted up because expected inflation increased.

Figure 15.9c Next period, with unemployment still low at 3%, inflation is equal to expected inflation plus the bargaining gap. The Phillips curve has shifted up because expected inflation increased.

- inflation-stabilizing rate of unemployment

- The unemployment rate (at labour market equilibrium) at which inflation is constant. Originally known as the ‘natural rate’ of unemployment. Also known as: non-accelerating rate of unemployment, stable inflation rate of unemployment. See also: equilibrium unemployment.

By plotting the path of inflation over time in Figure 15.10 we can see the distinctive contributions of the bargaining gap and expected inflation to inflation. In this example, the bargaining gap opens up in year 1 because of the move to low unemployment. The assumption that unemployment remains below the inflation-stabilizing rate is reflected in the persistence of the bargaining gap. Inflation rises in every period because the previous period’s inflation feeds into expected inflation and therefore into wage and price inflation. Note that the real wage does not change, but remains on the price-setting curve.

Inflation, expected inflation, and the bargaining gap.

Figure 15.10 Inflation, expected inflation, and the bargaining gap.

A zero bargaining gap

Inflation is as expected: 3%.

Figure 15.10a Inflation is as expected: 3%.

Year 1

At the start of year 1 following the opening up of the bargaining gap and after wages and prices have been adjusted, inflation is equal to the bargaining gap (2%) plus expected inflation (3%).

Figure 15.10b At the start of year 1 following the opening up of the bargaining gap and after wages and prices have been adjusted, inflation is equal to the bargaining gap (2%) plus expected inflation (3%).

Year 2

At the start of year 2, with no change in the bargaining gap, inflation goes up to 7%, equal to the bargaining gap plus expected inflation.

Figure 15.10c At the start of year 2, with no change in the bargaining gap, inflation goes up to 7%, equal to the bargaining gap plus expected inflation.

… and each year afterwards

As long as the bargaining gap remains unchanged, inflation rises each year.

Figure 15.10d As long as the bargaining gap remains unchanged, inflation rises each year.

Exercise 15.4 A negative aggregate demand shock with high unemployment

Copy Figure 15.9, making sure you leave plenty of space to the left of the 6% unemployment marker. Assume that from an initial position at A, there is a negative shock to private sector demand such as depressed private investment, which raises unemployment to 9%.

- Show the inflation, expected inflation, and the bargaining gap at the new level of unemployment on your diagram.

- What do you predict will happen to inflation over the following two years, assuming there is no further change in unemployment?

- Draw the Phillips curves and write a brief explanation of your findings.

Exercise 15.5 Inflation, expected inflation, and the bargaining gap

Use the same axes as in Figure 15.10 to plot inflation, expected inflation, and the bargaining gap in a single diagram. Assume that the price level is constant in period zero. The economy is hit by a recession at the beginning of period 1 and unemployment remains at a constant high level until the beginning of period 6.

- Plot the path of the bargaining gap.

- Plot the path of inflation and expected inflation.

- Give a brief explanation of why the bargaining gap might have disappeared and state any other assumptions you are making. Summarize your findings.

Question 15.6 Choose the correct answer(s)

Figure 15.6 is a scatter plot of the inflation rate and the unemployment rate for the US for each year between 1960 and 2014.

Based on this information, which of the following statements is correct?

- This is clearly not true from the graph.

- The Phillips curve shifted higher until the 1980s, but shifted lower in the 1990s-2010s.

- This reflects the slope of the Phillips curve in the 1960s.

- On the contrary, a flatter Phillips curve means that a small fall in the inflation rate is associated with a large rise in the unemployment rate. However this also means that a relatively large fall in the unemployment rate is associated with only a small rise in the inflation rate.

Question 15.7 Choose the correct answer(s)

Figure 15.9 depicts the diagrams of the labour market model and the Phillips curve that incorporates inflation expectations.

Based on this information, which of the following statements is correct?

- In this diagram the labour market equilibrium occurs at 3% inflation on the lower of the two Phillips curves. But at the labour market equilibrium of 6% unemployment, inflation will be constant whatever level it starts at. The Phillips curve will not shift up when the economy is at labour market equilibrium.

- With unemployment at 3%, initially the wage rises to 5% along the Phillips curve. The shift in the curve occurs in the next stage when the previous period’s inflation feeds into the next period’s expected inflation.

- With the unemployment rate stable at 3%, the bargaining gap remains at 2%. This causes the further rises in the inflation rate.

- The Phillips curve continues to shift upwards as long as there is a positive bargaining gap, caused by the low unemployment rate.

15.7 Supply shocks and inflation

Friedman was correct in two ways:

- Expected inflation shifts the Phillips curve.

- Policymakers were wrong to think of the Phillips curve as a feasible set from which they could simply select the most electorally popular combination of inflation and unemployment.

But there are other causes of high and rising inflation. The Phillips curve will shift up if the price-setting curve shifts down or the wage-setting curve shifts up. Recall Figure 15.2: if the power of owners of firms relative to consumers increases, the marketing department raises prices and kicks off a wage-price spiral. In that example, owners of firms in the home economy became more powerful because the government adopted policies that made it more difficult for foreign firms to enter the economy. Similarly, a wage-price spiral can begin if the power of employees increases relative to owners—as would be the case if trade unions become more powerful and exercise that power to achieve higher wage increases from the HR department.

- supply shock

- An unexpected change on the supply side of the economy, such as a rise or fall in oil prices or an improvement in technology. See also: wage-setting curve, price-setting curve, Phillips curve.

- demand shock

- An unexpected change in aggregate demand, such as a rise or fall in autonomous consumption, investment, or exports. See also: supply shock.

Shocks that move the Phillips curve by changing the labour market equilibrium are described as supply shocks, because the labour market represents production or supply in the economy. They are different from demand shocks, like a change in investment or in consumption, which work via their effect on aggregate demand. While a negative demand shock will increase unemployment and reduce inflation, a negative supply shock can lead to increased unemployment and inflation at the same time.

Changes in the global economy can also cause supply shocks that trigger inflation. A particularly important change for understanding the shifts in Phillips curves, such as those for the US economy shown in Figure 15.6, is a change in the world oil price (we look at other possible causes in Units 16 and 17). The labour market model and the Phillips curve can explain why a one-off increase in the world oil price can lead to a combination of:

- a one-off increase in the price level (inflation) at the time of the shock, and

- rising inflation over time

To do this, we show that a rise in the oil price:

- Shifts the price-setting curve down: This leads to a positive bargaining gap and inflation.

- Shifts the Phillips curve up: It will continue to shift up as expected inflation rises.

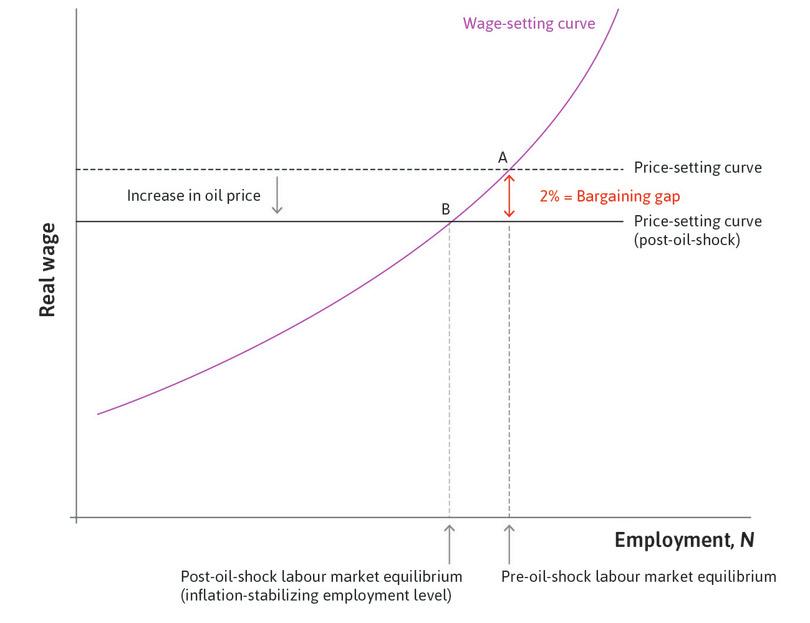

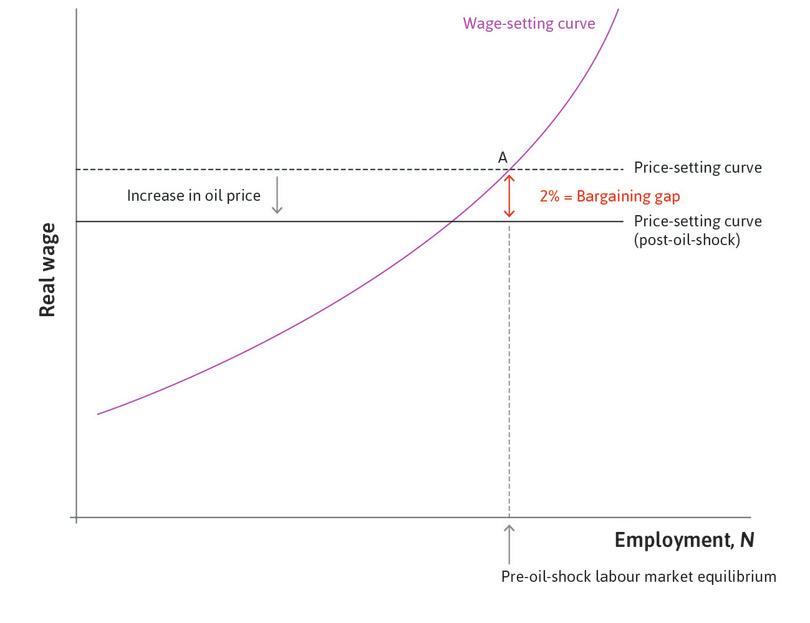

An increase in the oil price pushes down the price-setting curve. A typical firm uses imported oil in the production process. With increased costs for oil, the firm’s profits can only remain unchanged if real wages fall. At the level of the economy as a whole, the national pie to be divided between owners and employees shrinks when more has to be paid for imports.

We show in the Einstein at the end of this section how to modify the price-setting curve once firms in the economy use imported materials in production.

A rise in the oil price creates a bargaining gap and triggers a wage-price spiral through its effect on the price level. Firms raise their prices to protect their profit margins when the cost of imported oil rises. Firms across the economy will behave this way so the price level will rise. This reduces the real wage of employees, so the price-setting curve shifts down (to see how firms set their prices following an oil price rise, see the Einstein at the end of this section). At the initial employment level this opens up a bargaining gap between the real wage on the price-setting curve and the real wage on the wage-setting curve. That is, the rise in prices satisfies firms, but the corresponding fall in real wages does not satisfy workers.

In Figure 15.11, the price-setting curve shifts down following the oil shock. In this example, a bargaining gap of 2% opens up between the wage-setting curve and the post-shock price-setting curve. This fits the scenario in Figure 15.10, where a bargaining gap of 2% appears at the beginning of year 1. This increases inflation from its pre-existing level of 3% to 5% and as expected inflation adjusts, inflation rises thereafter every year. The Phillips curve shifts up year by year.

An oil shock and the price-setting curve.

Figure 15.11 An oil shock and the price-setting curve.

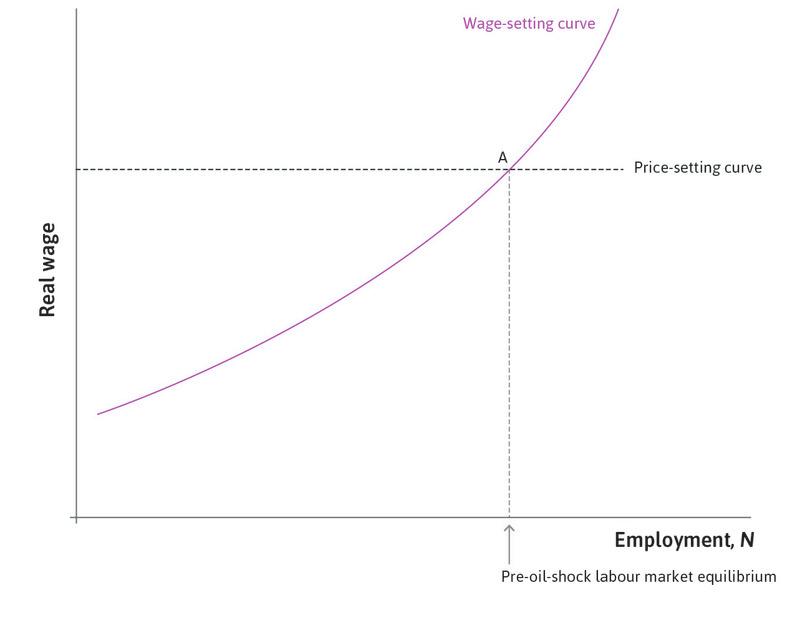

Labour market equilibrium

The economy is initially at point A.

Figure 15.11a The economy is initially at point A.

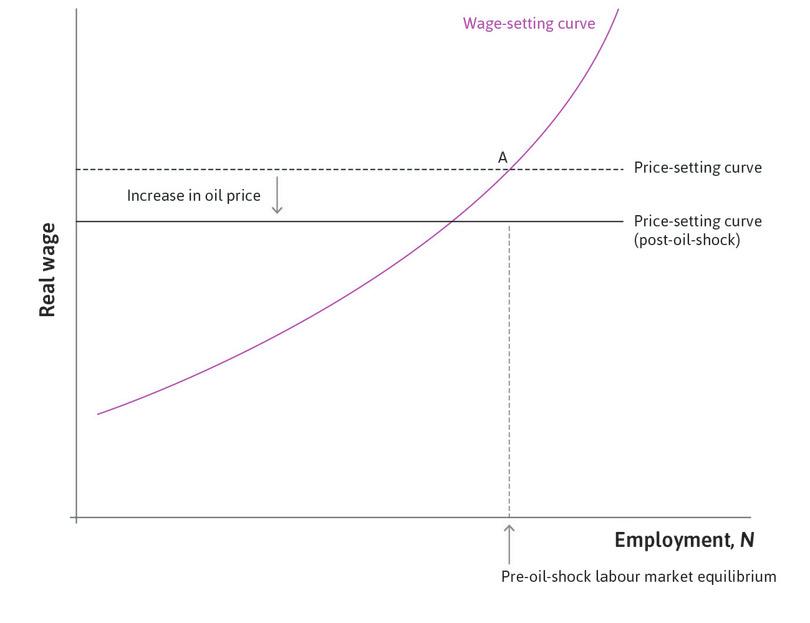

An oil shock

The oil price increases and shifts the price-setting curve down.

Figure 15.11b The oil price increases and shifts the price-setting curve down.

The bargaining gap

If aggregate demand is maintained to keep the economy at A, there is a positive bargaining gap. Inflation will increase year by year.

Figure 15.11c If aggregate demand is maintained to keep the economy at A, there is a positive bargaining gap. Inflation will increase year by year.

A new equilibrium

There is a new labour market equilibrium at B with higher unemployment.

Figure 15.11d There is a new labour market equilibrium at B with higher unemployment.

As long as employment remains at its pre-oil-shock level, inflation will increase every period, as illustrated in Figure 15.10. The new labour market equilibrium and post-shock inflation-stabilizing employment level is shown in Figure 15.11. Unemployment is higher at the new labour market equilibrium where the post-shock price-setting curve intersects the wage-setting curve.

Shocks to the world oil price are a major source of macroeconomic disturbance.

Following the early 1970s oil shock, for example, US inflation jumped from 6.2% in 1973 to 9.1% in 1975 and unemployment went from 4.9% to 8.5% at the same time.

This pattern was common across the developed world. For example, in the same period, inflation in Spain rose from 11.4% to 17% and unemployment increased from 2.7% to 4.7%.

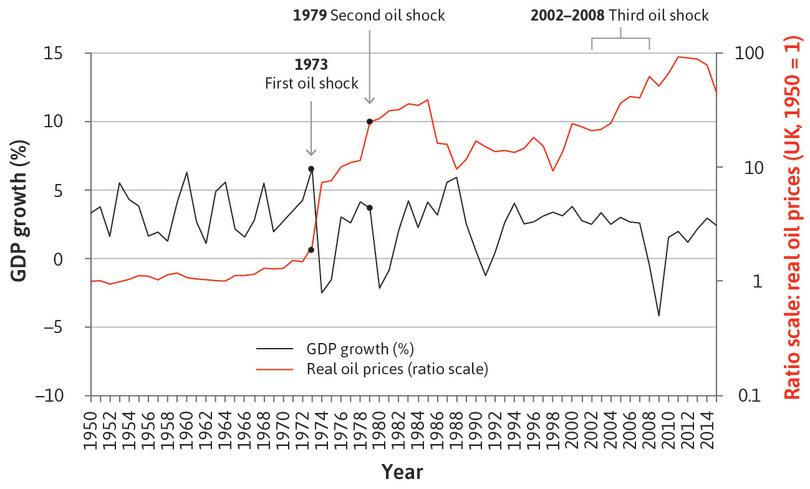

We can see from Figure 15.12 that there were two big recessions in the UK in the 1970s. They were due to the oil shocks of 1973–74 and 1979–80, which were associated with a rise in both unemployment and inflation to their highest levels since the Second World War (you can see the effect on inflation in Figure 13.19a and Figure 13.19b).

UK GDP growth and real oil prices (1950–2015).

Figure 15.12 UK GDP growth and real oil prices (1950–2015).

UK Office for National Statistics; Ryland Thomas and Nicholas Dimsdale. (2017). ‘A Millennium of UK Data’. Bank of England OBRA dataset.

High inflation in the 1970s and early 1980s was associated with high unemployment in many countries. Unemployment in the UK peaked at nearly 12% in the mid-1980s.

The model helps us to understand why the rise in the oil price led to rising inflation and high unemployment. But it also helps to explain the role that high unemployment played in bringing inflation down.

In the model, the only ways that high inflation can be brought down are:

- a reduction in the bargaining gap

- a fall in expected inflation

If unemployment is sufficiently high, then there will be a negative bargaining gap and inflation will fall. Remember that for the bargaining gap to be negative, unemployment has to rise above the new higher inflation-stabilizing unemployment rate. Once inflation begins to fall, it will continue to fall as the Phillips curve shifts downwards and the economy follows the path shown in Figure 15.10 in reverse.

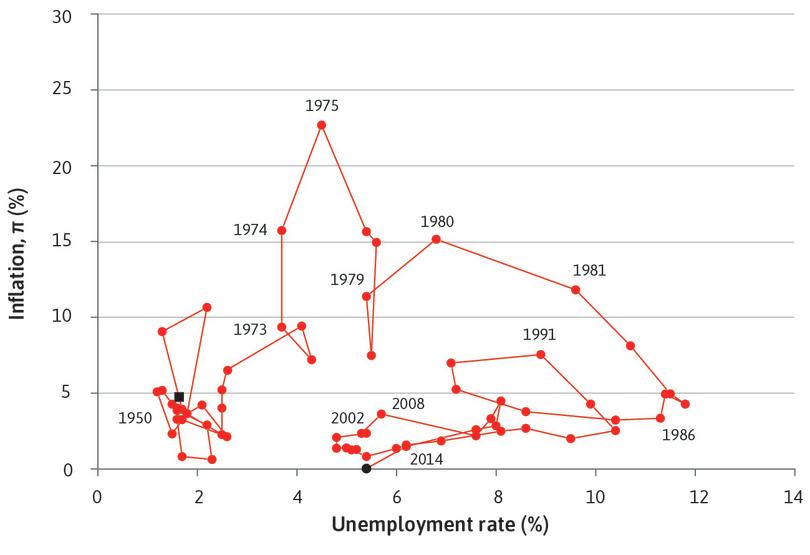

UK Inflation and unemployment rate (1950–2015).

Figure 15.13 UK Inflation and unemployment rate (1950–2015).

UK Office for National Statistics; Ryland Thomas and Nicholas Dimsdale. (2017). ‘A Millennium of UK Data’. Bank of England OBRA dataset.

Figure 15.13 shows a scatterplot of unemployment and inflation for the British economy from 1950 to 2014. Instead of fitting Phillips curves to the observations, as in Figure 15.6, the points are joined and dated. This helps us to follow the path taken by the economy. Notice the large increase in unemployment in the 1980s associated with bringing inflation down. This is sometimes referred to as the cost of disinflation.

But there’s a puzzle here: why did the third oil shock from 2002–08 not lead to increased inflation, just like the earlier ones? This section should have provided you with some starting points to investigate this, and a speech given in 2006 by David Walton, an economist, will help you.4 If you read both carefully, you might ask the following questions:

- Was the unit cost increase smaller due to less energy-intensive production? This would have made the increase in the materials cost per unit of output smaller and reduced the size of the initial downward shift in the price-setting curve.

- Did the wage-setting curve shift downwards at the same time as the third oil price shock? This also would have reduced or perhaps even eliminated the bargaining gap opened up by the oil price shock.

- Did a wage-price spiral fail to develop because expected inflation did not adjust upward, as in the past oil shocks?

What could stop expected inflation rising? In the next section, we examine the role of monetary policy.

Exercise 15.6 An oil shock

Think about the three questions related to oil shocks that we listed above. In each case:

- Explain the mechanism linking the oil shock to inflation using a diagram.

- Identify some evidence (for example, data or commentary in the economics press) that is consistent with the hypothesis proposed.

Einstein The price-setting curve with imported materials

In the Einstein in Unit 9, we explained how the price-setting curve for the economy as a whole results from the decisions of individual firms. Here we take a shortcut and go straight to the economy as a whole. Firms in the economy use both the products of other firms in the economy and imported products as inputs. The cost of these inputs will be affected by wage costs and costs of imported materials. Once we put together all the firms in an economy, we have only two types of cost: labour and imported materials. (Here we are setting aside the opportunity cost of the capital goods used in production that are the property of the firm owners and the basis of their profits.)

In Unit 9, we assumed that other than the firm’s own capital goods, there were no inputs other than labour and hence no costs other than wages. In this case, the value of a firm’s output was the same as the firm’s value added. Expressed on a per worker basis this was divided into wage and profits:

Here, there are imported materials such as oil that are necessary to produce the output. As a result, the firm’s costs include not only wages but also the costs of purchasing these imported materials.

This makes it clear that unlike in Unit 9 where there were just two claimants on the value of the output (wages and profits), we now have three: labour costs, imported materials costs, and profits. This affects the price-setting curve, as we shall see.

In the Unit 9 Einstein, λ represented value added per worker, or labour productivity. Now, where we have inputs other than labour, we define q as the units of output per worker, which is not the same thing as labour productivity because output now exceeds value added by the value of imported inputs.

Since output per worker is q and the nominal wage is W, the firm’s unit labour cost (ulc) is:

Now the firm’s cost per unit is its unit labour cost (ulc) plus its unit imported materials cost (umc).

So unit costs (uc) are:

We define the markup, μ, as the share of the price that represents profits to the firm (what is left over after subtracting unit costs):

Note that umc/P is the imported materials cost as a share of the price of a unit of output, while ulc/P is the wage cost as a share of the price of a unit of output. For example, suppose the price per unit is $5, imported materials cost $1 per unit and labour costs $2.50 per unit. Then imported materials comprise 20% of the cost, wages another 50%, and the share of profit, or the markup, is:

which is 30%.

Substituting ulc = W/q gives us:

Multiplying each side by q and rearranging, and remembering that P is both the price of the individual firm’s output and the general price level in the economy, we get the price-setting curve: