Unit 14 Unemployment and fiscal policy

Themes and capstone units

How governments can moderate costly fluctuations in employment and income

- Fluctuations in aggregate demand affect GDP growth through a multiplier process, because households face limits to their ability to save, borrow, and share risks.

- An increase in the size of government following the Second World War coincided with smaller economic fluctuations.

- Governments can use changes in taxes or government spending to stabilize the economy, but bad policy can destabilize it.

- If a single household saves, its wealth necessarily increases, but if all households save this may not be true, because without additional spending by the government or firms to counteract the fall in demand, aggregate income will fall.

- Every national economy is embedded in the world economy. This is a source of shocks, both good and bad, and places constraints on the kinds of policies that can be effective.

In August 1960, three months before he was elected US president, the 43-year-old Senator John F. Kennedy found time to spend the day cruising Nantucket Sound on his boat, the Marlin. His crew for the day included John Kenneth Galbraith and Seymour Harris, both Harvard economists, and Paul Samuelson, an economist at MIT and later also a Nobel laureate. They had not been recruited for their nautical skills. In fact, apart from Harris, the senator did not even know them.

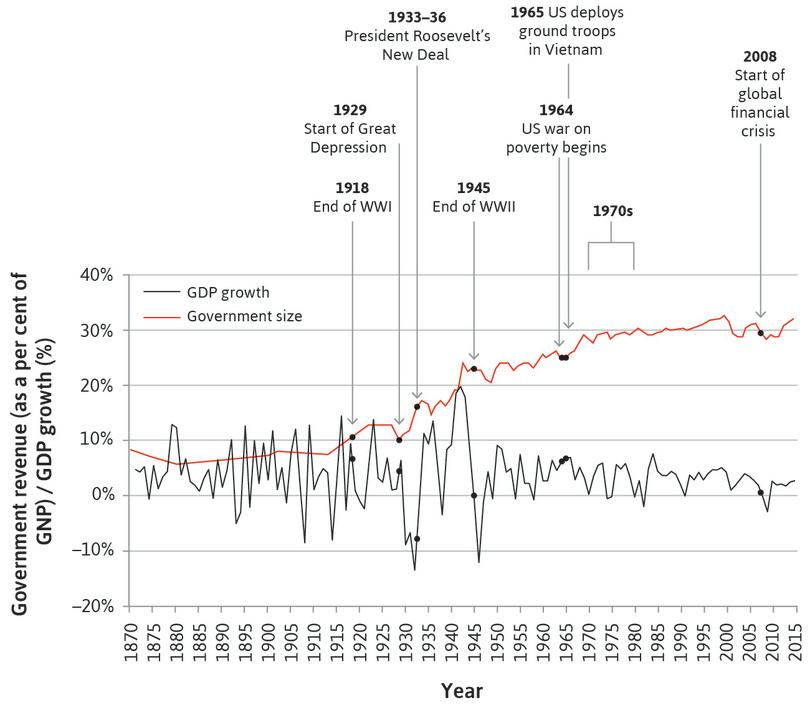

The future president wanted to learn ‘the new economics’, which John Maynard Keynes, an economist who we will learn more about in Section 14.6, had formulated in response to the Great Depression. When Kennedy was a teenager in the decade before the Second World War, the US and many other countries experienced a drastic fall in output (we can see this for the US in Figure 14.1) and massive unemployment that persisted for more than 10 years.

Kennedy had a lot to learn. He admitted that he had barely passed the only economics course he took at Harvard. He would later spend a day at the America’s Cup sailing races being tutored by Harris, who assigned texts for him to read. Harris later gave private lessons to the senator, shuttling by air between Boston, where he worked, and Washington DC.

In 1948, Samuelson had written Economics, the first major textbook to teach these new ideas. Harris promoted the same economic ideas in a book that he edited in 1948 called Saving American Capitalism, a collection of 31 essays by 24 contributors. At that time, it seemed that capitalism needed saving: the centrally planned economies of the Soviet Union and its allies, a model promoted as the alternative to capitalism, had entirely avoided the Great Depression. Kennedy needed economics to understand policies that could promote economic growth, reduce unemployment, but also avoid economic instability.

We have seen in Unit 13 that instability in the economy as a whole is characteristic not only of economies dominated by agriculture, but also of capitalist economies. Figure 14.1 shows the annual growth of real GDP in the US economy since 1870.

Fluctuations in output and the size of government in the US (1870–2015).

Figure 14.1 Fluctuations in output and the size of government in the US (1870–2015).

The Maddison Project. 2013. 2013 Version; US Bureau of Economic Analysis. 2016. GDP & Personal Income; World Bank; Wallis, John Joseph. 2000. ‘American Government Finance in the Long Run: 1790 to 1990’. Journal of Economic Perspectives 14 (1) (February): pp. 61–82.

A dramatic reduction in the severity of business cycles occurred after the end of the Second World War. Figure 14.1 shows another important development at that time: the increasing role of the government in the economy. The red line shows the share of federal (national), local, and state government tax revenue as a share of GDP. This is a good measure of the size of the government relative to that of the economy.

The share of employment in agriculture, which we have seen was one cause of volatility in the economy, fell from 50% in the 1870s to 20% by the beginning of the Second World War, yet there was no sign of the economy becoming more stable over this period. As we have seen, households try to smooth fluctuations in their consumption but they can’t always do this successfully, partially because there are limits to how much they can borrow.

The fact that the fluctuations in output growth dramatically reduced while the size of government expanded does not mean that increased government spending stabilized the economy (remember: statistical correlations do not mean causation). But there are good reasons to think that the increase in the red line was part of the reason for the smoothing of the black line. In this unit, we ask why the increased role of the government in the economy is part of the explanation for the more stable economy in the second half of the twentieth century.

What Harris taught Kennedy was influenced by the contrast between the volatility of the economy before the Second World War, and the steadier growth and absence of deep recessions afterwards. Why do economies experience unemployment, inflation, and instability in output, and what kinds of policies might address these problems?

- great moderation

- Period of low volatility in aggregate output in advanced economies between the 1980s and the 2008 financial crisis. The name was suggested by James Stock and Mark Watson, the economists, and popularized by Ben Bernanke, then chairman of the Federal Reserve.

In Unit 13, we took the household‘s viewpoint of the business cycle, which allowed us to establish why fluctuations in employment and income are costly, and how households try to limit the consequences for their wellbeing. In this unit, we take the policymaker’s viewpoint. As we saw in Figure 14.1, the big increase in the size of government after the Second World War was accompanied by a reduction in the size of business cycle fluctuations. After 1990, the business cycle in advanced economies became even smoother, until the global financial crisis in 2008. This led to the period from the early 1990s to the late 2000s being called the great moderation.

14.1 The transmission of shocks: The multiplier process

In a capitalist economy, private investment spending is driven by expectations about future post-tax profits. As we saw in Unit 13, spending on investment projects tends to occur in clusters. Two reasons for this observation are:

- Firms may adopt a new technology at the same time.

- Firms may have similar beliefs about expected future demand.

We need a tool to help us understand how decisions of firms (and households) to raise or reduce investment spending will affect the economy as a whole. You will recall that some households are able to completely smooth temporary bumps in their income, but that in credit-constrained households, higher income from getting a job or moving from part-time to full-time work will also lead to higher consumption spending.

- aggregate demand

- The total of the components of spending in the economy, added to get GDP: Y = C + I + G + X – M. It is the total amount of demand for (or expenditure on) goods and services produced in the economy. See also: consumption, investment, government spending, exports, imports.

As a result, changes in current income influence spending, affecting the income of others, so indirect effects through the economy amplify the direct effect of a shock to aggregate demand (often shortened to AD) created by an investment boom.

We will show how economists answer such questions as ‘how large would the total direct and indirect impact of a rise in investment spending be?’ or, ‘what would be the effect of lower government spending?’

A statistic called the multiplier provides one way of answering this question. Imagine there is a new technology. New spending takes place in the economy as a result; output of the new capital goods rises, as do the incomes of the people producing them. The circular flow of expenditure, income, and output previously shown in Figure 13.6 illustrates this process.

- If the total increase in GDP is equal to the initial increase in spending: We say that the multiplier is equal to 1.

- If the total increase in GDP is greater or less than the initial increase in spending: We say that the multiplier is greater than 1 or less than 1.

- multiplier process

- A mechanism through which the direct and indirect effect of a change in autonomous spending affects aggregate output. See also: fiscal multiplier, multiplier model.

- consumption function (aggregate)

- An equation that shows how consumption spending in the economy as a whole depends on other variables. For example, in the multiplier model, the other variables are current disposable income and autonomous consumption. See also: disposable income, autonomous consumption.

To see why GDP may rise by more than the initial increase in investment spending, we explain what economists call the multiplier process. We do this by combining the very different behaviour of consumption-smoothing and non-smoothing households to represent consumption spending for the economy as a whole. In this aggregate consumption function, consumption depends on current income, among other things. Recall that in the model of Unit 13, consumption-smoothing households will not increase their consumption one-for-one, or even at all, in response to a temporary €1 increase in their income. Credit-constrained and other households who do not smooth, on the other hand, will increase their current consumption by €1 in response to a temporary €1 increase in their income.

In 2008, when governments considered temporary increases in government spending and tax cuts in response to the recession that followed the global financial crisis, the size of the multiplier became the subject of a debate among policymakers and economists. We return to this debate later in the unit.

As we shall see, the multiplier is greater than 1 if the additional consumption spending resulting from a temporary €1 increase in income is greater than zero but less than €1 (say, for example, 60 cents).

After explaining how this is a consequence of the multiplier process, we will show that the validity of the assumptions we make in the multiplier model depend on the state of the economy.

14.2 The multiplier model

- consumption (C)

- Expenditure on consumer goods including both short-lived goods and services and long-lived goods, which are called consumer durables.

- investment (I)

- Expenditure on newly produced capital goods (machinery and equipment) and buildings, including new housing.

We begin with a simple model that excludes the government and foreign trade. In this model, there are two types of expenditure:

- consumption

- investment

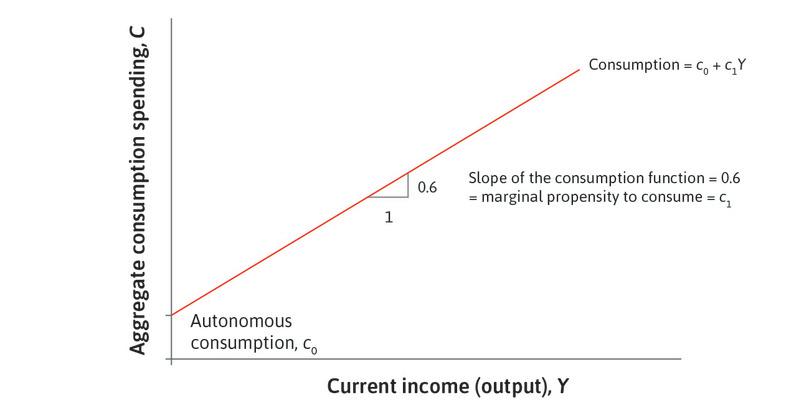

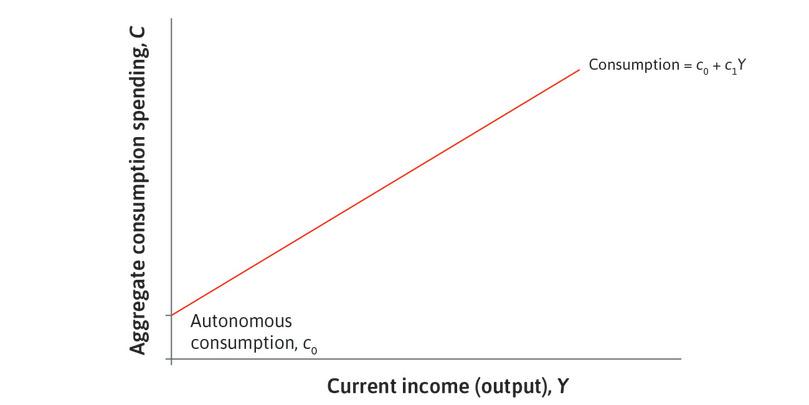

We assume that aggregate consumption spending has two parts:

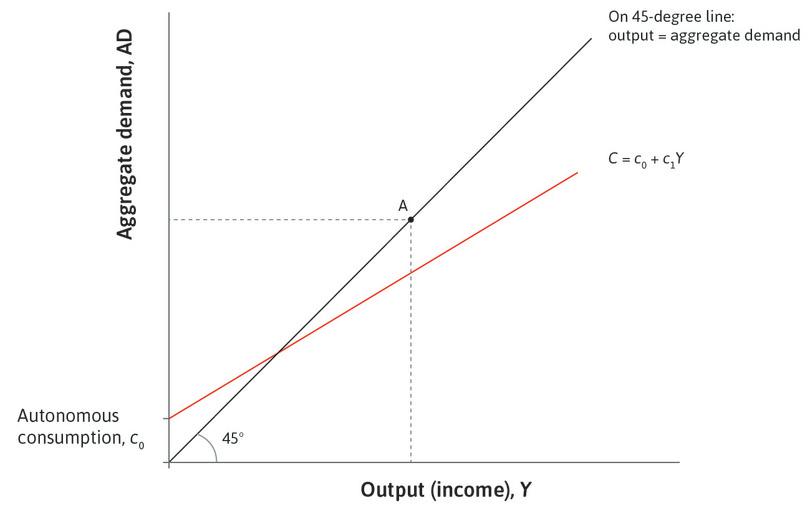

- A fixed amount: How much people will spend, independent of their income. This fixed amount, also known as autonomous consumption, is shown as c₀ on the vertical axis of Figure 14.2.

- A variable amount: This depends on current income, and is an upward-sloping red line in Figure 14.2.

- autonomous consumption

- Consumption that is independent of current income.

So we can write consumption spending in the form of an equation, which we call the aggregate consumption function:

- marginal propensity to consume (MPC)

- The change in consumption when disposable income changes by one unit.

The term c1 gives the effect of one additional unit of income on consumption, called the marginal propensity to consume (MPC). In Figure 14.2, the slope of the consumption line is equal to the marginal propensity to consume. A steeper consumption line means a larger consumption response to a change in income. A flatter line means that households are smoothing their consumption so that it does not vary much when their incomes change. We assume that the marginal propensity to consume is positive, but less than one. This means that only part of an increase in income is consumed; the rest is saved.

The aggregate consumption function.

Figure 14.2 The aggregate consumption function.

Autonomous consumption

This is the fixed amount that households will spend that does not depend on their current level of income.

Figure 14.2a This is the fixed amount that households will spend that does not depend on their current level of income.

Consumption that depends on income

The upward-sloping line denotes the part of consumption that depends on current income (and hence on current output).

Figure 14.2b The upward-sloping line denotes the part of consumption that depends on current income (and hence on current output).

The marginal propensity to consume

The slope of the consumption line is equal to the marginal propensity to consume.

Figure 14.2c The slope of the consumption line is equal to the marginal propensity to consume.

We will work with an aggregate consumption function in which the marginal propensity to consume, c1, equals 0.6. This means that an additional unit of income (Euros in this case) increases consumption by €1 × 0.6 = 60 cents.

Naturally, this average number hides large variation across households, who differ in their wealth and in the credit constraints they face. Most households have little wealth, and even in rich countries about one in four households are credit-constrained. As we saw in Unit 13, weakness of will also plays a role. So, both for households that are credit-constrained and for those that do not save ahead of anticipated declines in income, consumption closely tracks income.

Households with low wealth smooth consumption very little if their income falls sharply. The marginal propensity to consume for this group is closer to 0.8. For the small fraction of households who hold the majority of wealth, however, current income plays a very small role in determining consumption, and their marginal propensity to consume is closer to zero. This means that for rich households, an increase in current income of €1 would raise their consumption by just a few cents.

The term c₀ in the aggregate consumption function captures all the other influences on consumption that are not related to current income. Taken literally, it is how much a person with no income would consume, but this is not the best way to think about it. It is just the consumption that is independent of income, and for this reason we call it autonomous consumption.

Since the consumption function only explicitly includes current income, expectations about future income will be included in autonomous consumption. To see what this means in practice, recall from Unit 13 that consumption will change as a result of people becoming more or less optimistic about their future employment and earnings prospects.

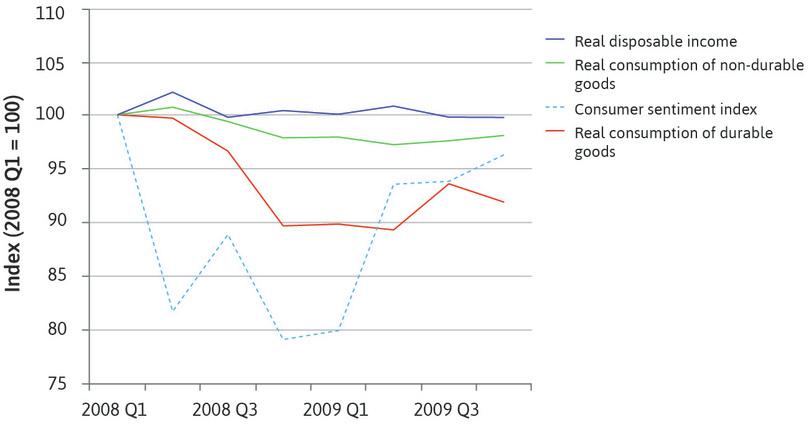

Figure 14.3 illustrates how expectations affected consumption in the financial crisis of 2008 and highlights the exceptional nature of this episode. The figure shows how consumer confidence changed in the US over the course of the crisis. The consumer sentiment index that we have used is the University of Michigan Surveys of Consumers. It is based on monthly interviews with 500 households, and asks how they view prospects for their own financial situation and for the general economy over the short and long term. The figure also plots the evolution of a number of key macroeconomic indicators: disposable income, consumption of durable goods like cars and home furnishings, and consumption of non-durable goods, such as food. All of the series in Figure 14.3 are shown as index numbers, with the first quarter of 2008 as the base year.

Fear and household consumption in the US during the global financial crisis (2008 Q1–2009 Q4).

Figure 14.3 Fear and household consumption in the US during the global financial crisis (2008 Q1–2009 Q4).

Federal Reserve Bank of St. Louis. 2015. FRED.

We notice:

- Consumption of non-durable goods went down slightly more than disposable income: It fell by 3% during the period. Contrary to the predictions of consumption smoothing, households were sufficiently worried about their future prospects that they made adjustments to their spending on non-durables.

- Consumption of durables decreased much more dramatically than disposable income: It decreased by 10% in the first year.

Why the sudden drop in consumption of consumer durables? An important reason is that households were suddenly fearful about the future of their jobs, as shown by the sharp decline in the consumer sentiment index in Figure 14.3. The collapse of the investment bank Lehman Brothers in September 2008, worries about the stability of the banking system, and a higher burden of household debt due to falling house prices led households with mortgages to postpone purchases of expensive items like cars and fridges. It’s important to remember that spending on consumer durables can easily be postponed. In this sense it is more like an investment than a consumption decision (even though consumer durables are counted as part of consumption in the national accounts). As a result, we would expect the series for consumer durables to be more volatile than for non-durable consumption.

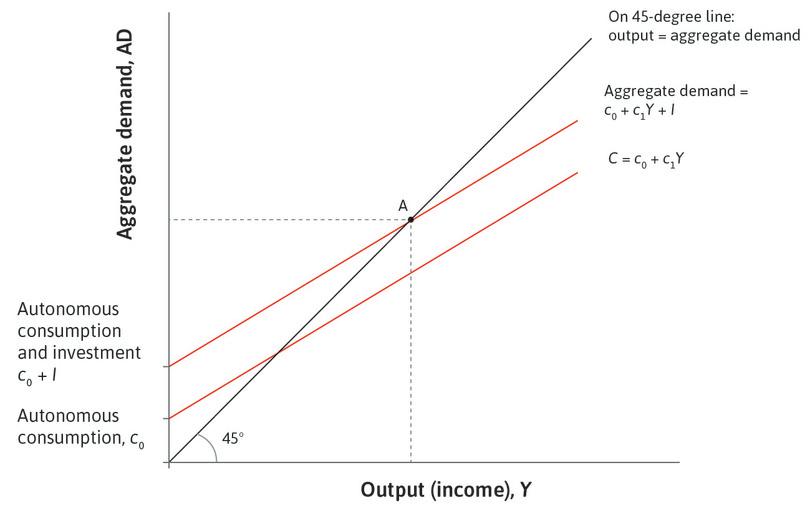

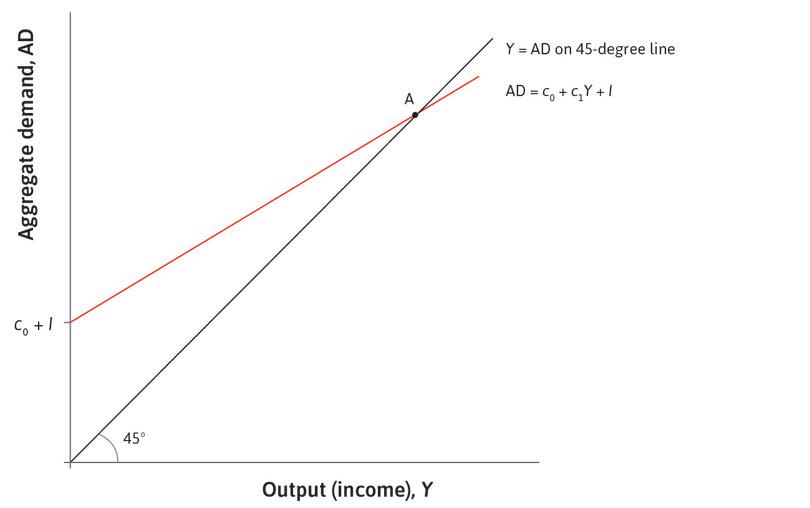

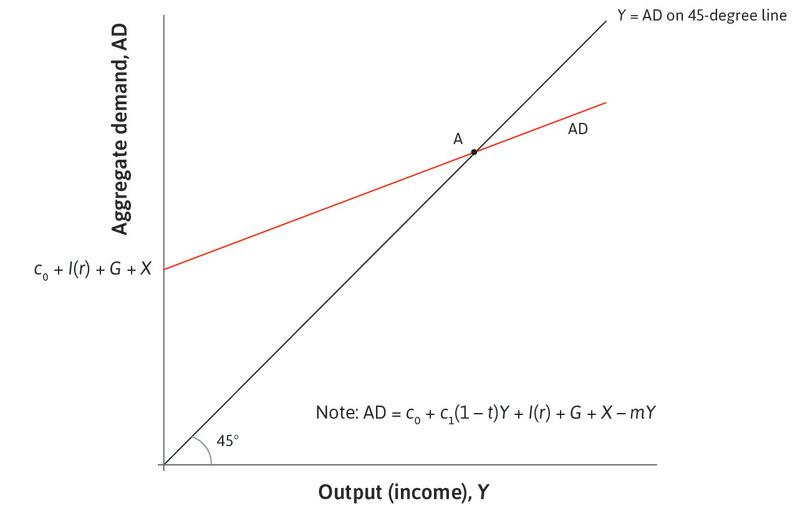

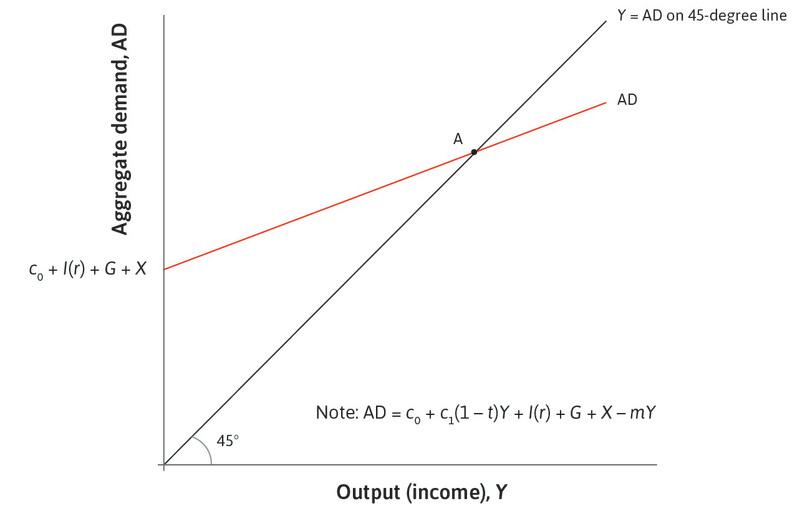

We now show how a shock is transmitted through the economy. In Figure 14.4 we show the amount of output produced by the economy (on the horizontal axis) and the demand for output (on the vertical axis). Everything is measured in real terms because we are interested in how changes in aggregate demand create changes in output and employment.

Goods market equilibrium: The multiplier diagram.

Figure 14.4 Goods market equilibrium: The multiplier diagram.

Goods market equilibrium

Point A is called a goods market equilibrium: the economy will continue producing at that output level unless something changes spending behaviour.

Figure 14.4a Point A is called a goods market equilibrium: the economy will continue producing at that output level unless something changes spending behaviour.

The 45-degree line

The 45-degree line from the origin of the diagram shows all the combinations in which output is equal to aggregate demand, meaning the economy is in goods market equilibrium.

Figure 14.4b The 45-degree line from the origin of the diagram shows all the combinations in which output is equal to aggregate demand, meaning the economy is in goods market equilibrium.

Consumption

The first component of aggregate demand is consumption, which is represented by the consumption line introduced in Figure 14.2.

Figure 14.4c The first component of aggregate demand is consumption, which is represented by the consumption line introduced in Figure 14.2.

Investment

Adding investment to the consumption line simply leads to a parallel upward shift of the aggregate demand line.

Figure 14.4d Adding investment to the consumption line simply leads to a parallel upward shift.

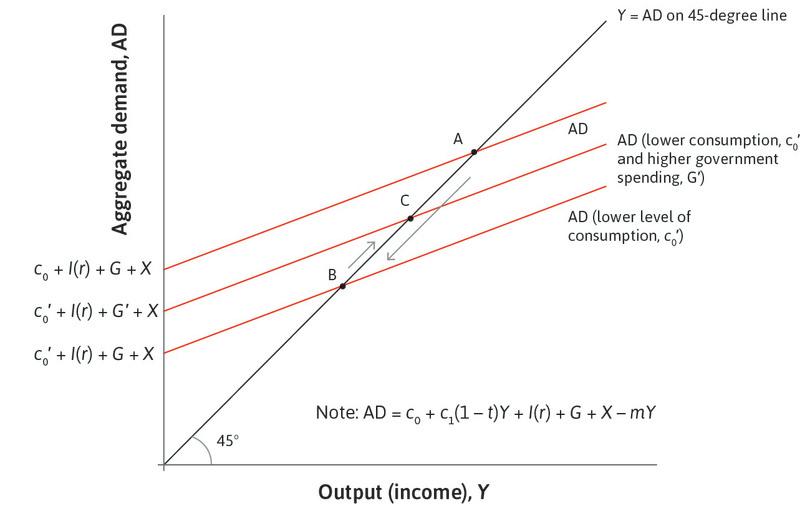

The 45-degree line from the origin of the diagram shows all the combinations in which output is equal to aggregate demand. This corresponds to the circular flow discussed in Unit 13, where we saw that spending on goods and services in the economy (aggregate demand) is equal to production of goods and services in the economy (aggregate output). You can see this because with a 45-degree line the horizontal distance (output) is equal to the vertical distance (aggregate demand). We can therefore say that:

- goods market equilibrium

- The point at which output equals the aggregate demand for goods produced in the home economy. The economy will continue producing at this output level unless something changes spending behaviour. See also: aggregate demand.

- capacity utilization rate

- A measure of the extent to which a firm, industry, or entire economy is producing as much as the stock of its capital goods and current knowledge would allow.

But how do we know where the economy is on the 45-degree line? Is it at a position of low output, which would mean high unemployment, or is it at a position of high output, which would mean low unemployment?

We determine this position by analysing the individual components of aggregate demand. We assume that firms are willing to supply any amount of the goods demanded by those making purchases in the economy; they are not operating at full capacity utilization. Because we have assumed that there is no government spending or trade with other economies, in this model there are just two components of aggregate spending:

- Consumption: We take the consumption line introduced in Figure 14.2. Because the marginal propensity to consume is less than one, the consumption line is flatter than the 45-degree line, which has a slope of one.

- Investment: We assume investment does not depend on the level of output.

The equation for aggregate demand is therefore:

So adding investment to the consumption line simply leads to a parallel upward shift. In this respect, investment is similar to autonomous consumption. We can see from Figure 14.4 that the aggregate demand line has an intercept of c₀ + I, a slope of c1, and is flatter than the 45-degree line.

In Figure 14.4 we now have a picture showing how the level of output in the economy is determined. Output is equal to aggregate demand (the 45-degree line), and aggregate demand is equal to c₀ + c1Y + I (the flatter line), so the economy must be at point A where the two lines cross.

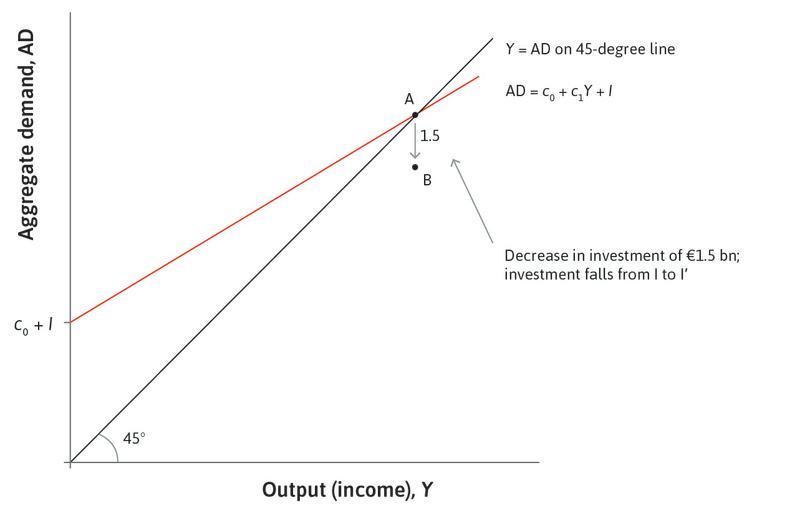

The same figure tells us the effect of a change in autonomous consumption (c₀) or investment. We study this change exactly as we did the changes in supply and demand in Unit 11: we see how the change makes the old outcome no longer an equilibrium, and then we locate the new equilibrium. The expected change is the movement from the old to the new equilibrium.

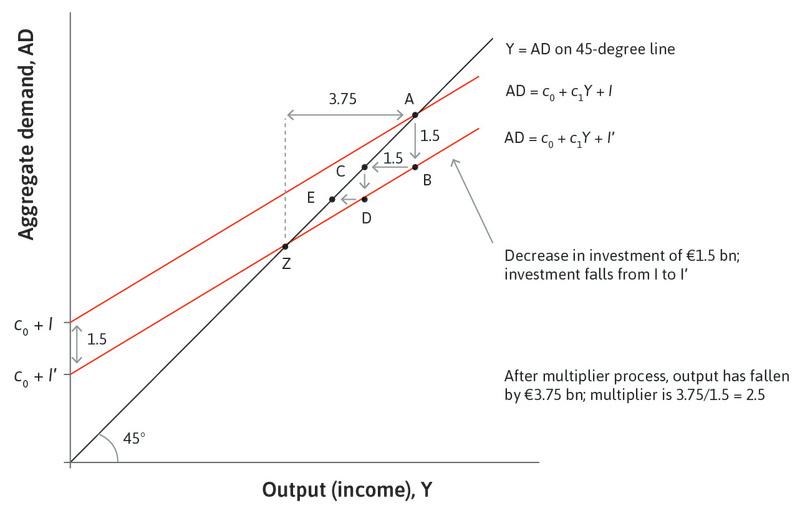

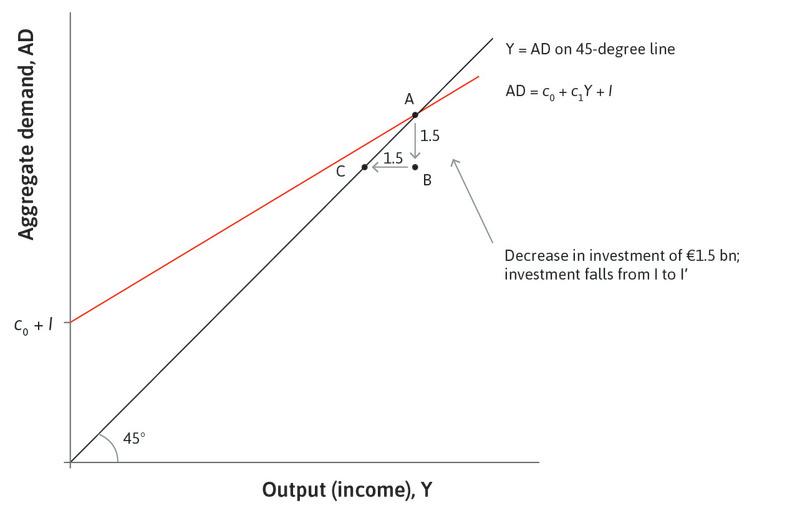

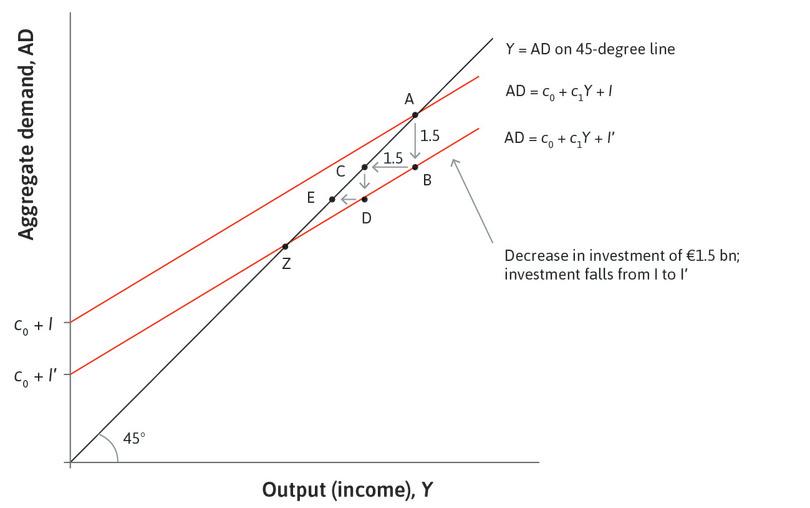

Changes in autonomous consumption or investment displace the old equilibrium because they change aggregate demand, which in turn alters the level of output and employment. In Figure 14.5, we take the multiplier diagram and reduce investment. We choose a reduction in investment of €1.5 billion. Follow the steps in Figure 14.5 to see what happens.

The multiplier in action: An investment-led recession.

Figure 14.5 The multiplier in action: An investment-led recession.

Goods market equilibrium

The economy starts at point A, in goods market equilibrium.

Figure 14.5a The economy starts at point A, in goods market equilibrium.

A fall in investment

The fall in investment cuts aggregate demand by €1.5 billion, and the economy moves vertically downward from point A to point B.

Figure 14.5b The fall in investment cuts aggregate demand by €1.5 billion, and the economy moves vertically downward from point A to point B.

Firms cut back

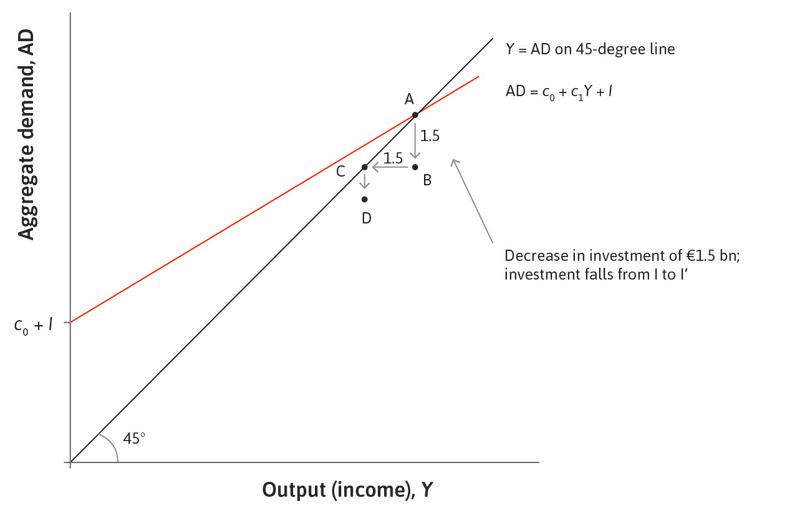

With demand lower, firms cut back production and reduce employment. With output and employment lower, incomes fall by €1.5 billion. This is the move from B to C.

Figure 14.5c With demand lower, firms cut back production and reduce employment. With output and employment lower, incomes fall by €1.5 billion. This is the move from B to C.

A fall in consumption

Once households’ incomes fall, they reduce their consumption, because they may be credit-constrained. The consumption equation tells us that this kind of behaviour initially leads to a fall in aggregate consumption of 0.6 times the fall in income. This is the distance from point C to point D.

Figure 14.5d Once households’ incomes fall, they reduce their consumption, because they may be credit-constrained. The consumption equation tells us that this kind of behaviour initially leads to a fall in aggregate consumption of 0.6 times the fall in income. This is the distance from point C to point D.

Firms cut back again

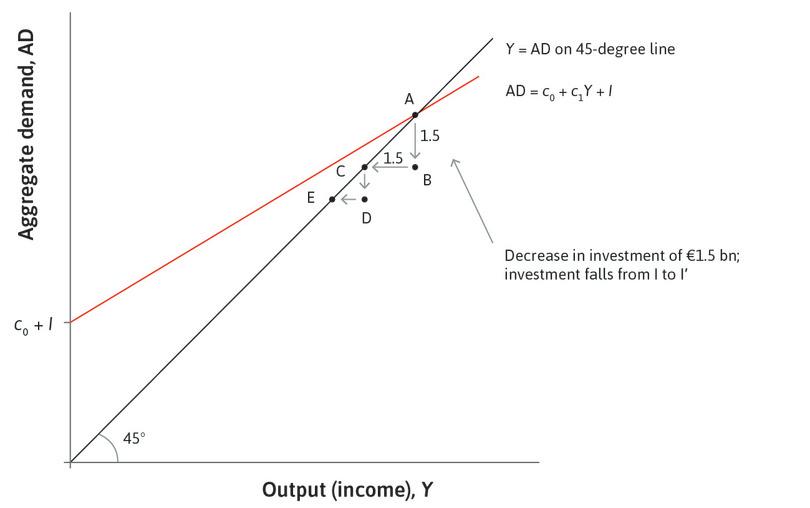

Firms respond by cutting production, output falls, and the economy moves from point D to point E.

Figure 14.5e Firms respond by cutting production, output falls, and the economy moves from point D to point E.

… and so on

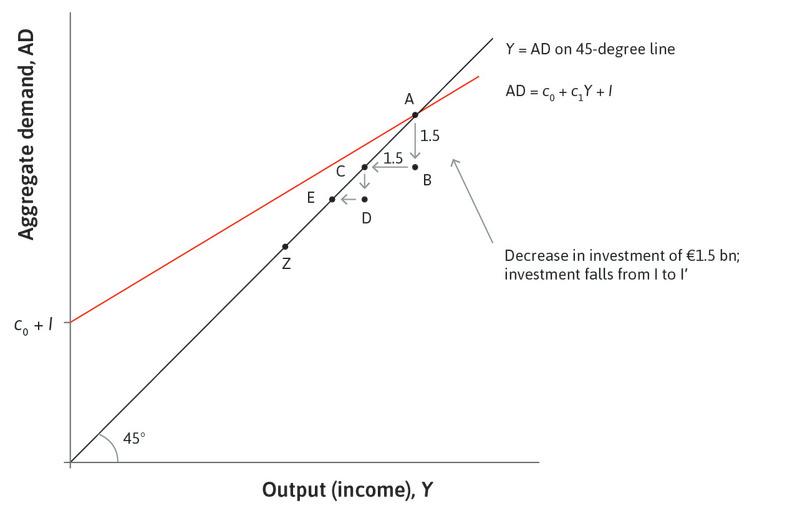

The process will go on until the economy reaches point Z.

Figure 14.5f The process will go on until the economy reaches point Z.

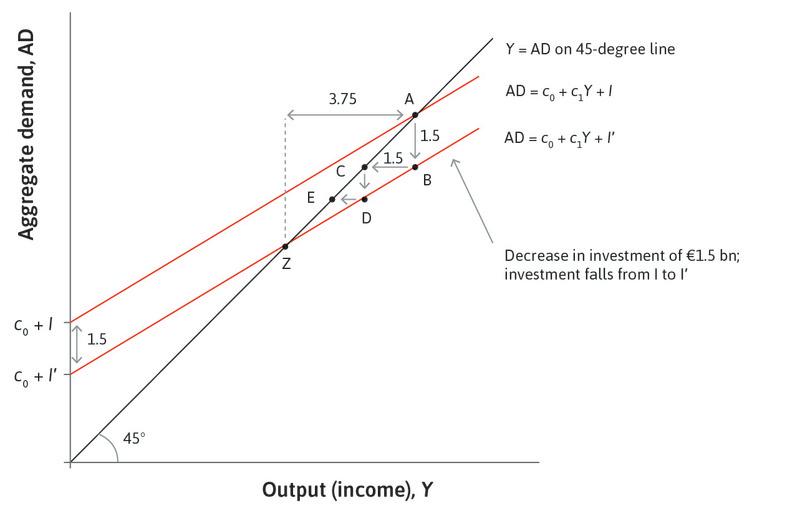

The new aggregate demand line

This goes through point Z and shows the new goods market equilibrium of the economy following the investment shock.

Figure 14.5g This goes through point Z and shows the new goods market equilibrium of the economy following the investment shock.

The fall in output as a result of the shock

The total fall in output exceeds the initial size of the decline in investment; output has fallen by €3.75 billion.

Figure 14.5h The total fall in output exceeds the initial size of the decline in investment; output has fallen by €3.75 billion.

The multiplier is equal to 2.5

The total change in output is 2.5 times larger than the initial change in investment.

Figure 14.5i The total change in output is 2.5 times larger than the initial change in investment.

We trace the effect of the fall in investment through the economy in Figure 14.5. The first-round effect is that the fall in investment cuts aggregate demand by €1.5 billion. But lower spending also means lower production and lower incomes, and firms will fire workers as a result, leading to a further decline in spending. Think of credit-constrained households where some members lose their job: they would like to keep consumption stable, but when their income falls they are unable to borrow enough to sustain that level of consumption, so they reduce their spending, which leads to further cuts in production and incomes. The consumption equation tells us that this kind of behaviour leads to a fall in aggregate consumption of 0.6 times the fall in income. The process will go on until the economy reaches point Z.

Following the investment shock, the intercept of the line has moved down by €1.5 billion, causing a parallel shift in the aggregate demand line. Output has fallen by €3.75 billion, more than the fall in investment of €1.5 billion: this is the multiplier process.

In this case, the multiplier is equal to 2.5, because the total change in output is 2.5 times larger than the initial change in investment. A multiplier of 2.5 is unrealistically large. As we shall see in the next section, once taxes and imports are introduced in the model, the multiplier shrinks.

- multiplier model

- A model of aggregate demand that includes the multiplier process. See also: fiscal multiplier, multiplier process.

We call the model of aggregate demand that includes the multiplier process the multiplier model. This is a summary:

- A fall in demand leads to a fall in production and an equivalent fall in income: This leads to a further (smaller) fall in demand, which leads to a further fall in production, and so on.

- The multiplier is the sum of all these successive decreases in production: Eventually, output has fallen by a larger amount than the initial shift in demand. Output is a multiple of the initial shift.

- Production adjusts to demand: Firms supply the amount of goods demanded at the prevailing price. When demand falls, firms adjust production down. The model assumes that they do not adjust their prices.

Note that the economy we are studying is one in which we assume there are underutilized resources in the form of spare capacity in production facilities and underemployed labour. We also assume that wages are not affected by changes in the level of output. For the multiplier process to work in the same way in response to a rise in investment, the assumption of spare capacity and fixed wages means that costs will not rise when output goes up, so firms will be happy to supply the extra output demanded without adjusting their prices. Otherwise some of the increased spending will translate into higher prices or wages rather than higher real output—as we discuss in the next unit.

If the economy is not characterized by spare capacity and constant wages, the multiplier will be smaller than what we find here.

We can also show the effect on output by combining the two equations that determine the lines in the multiplier diagram. The 45-degree line is simply the equation Y = AD. Combining this with the equation for AD gives us:

Collecting terms on the left hand side,

We then divide through by (1 − c1):

- autonomous demand

- Components of aggregate demand that are independent of current income.

We can now calculate how much output will increase or decrease using the value of the multiplier times the change in autonomous demand.

Discover another way to summarize our findings from the diagram algebraically in the Einstein at the end of this section.

The change in output in Figure 14.5 is 2.5 times greater than the initial shock to investment, which means that the shock has been amplified. In algebra, we write this as ΔY = kΔI, and say it as ‘delta Y (the change in output) is equal to k, the multiplier, times delta I (the change in investment)’.

Question 14.1 Choose the correct answer(s)

Figure 14.2 depicts a consumption function of an economy, where C is the aggregate consumption spending and Y is the current income of the economy.

Based on this information, which of the following statements is correct?

- The MPC is the proportion of the additional income received that is spent on consumption. Here it is given by c1. C/Y is the average propensity to consume.

- The slope of the line gives the MPC.

- Households that smooth consumption will increase spending by less than the amount their income increases.

- C is c0 + c1Y, that is, $60 trillion plus the fixed (or autonomous) consumption c0.

Question 14.2 Choose the correct answer(s)

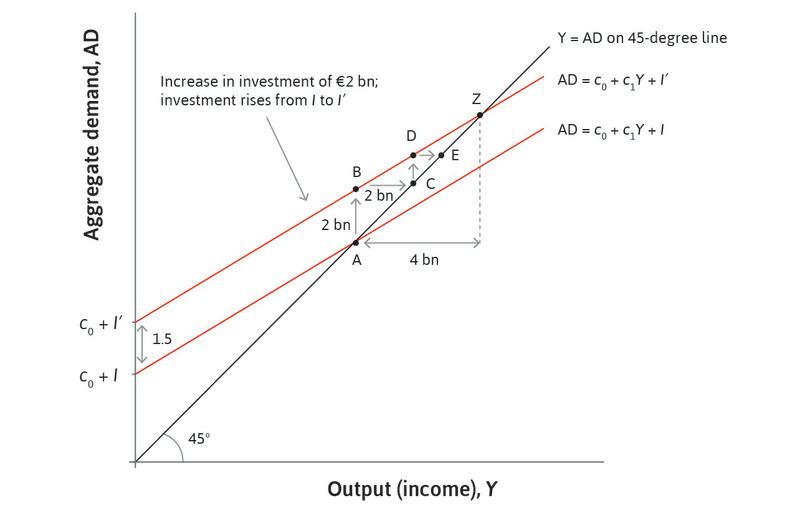

The following diagram depicts the change in the aggregate goods market equilibrium when there is a €2 billion increase in investment.

The aggregate goods market when there is a €2 billion increase in investment.

The economy’s marginal propensity to consume is 0.5. Based on this information, which of the following statements is correct?

- The equilibrium is where the aggregate consumption line intersects with the 45-degree line. Therefore the new equilibrium is Z.

- The diagram shows that the increase in investment results in a €4 billion increase in aggregate demand.

- The multiplier is equal to 1/(1 − 0.5) = 2.

- The distance between A and B is the initial increase in investment of €2 billion. At C, the output Y has increased by €2 billion compared with B, which results in an increase in the aggregate demand of ΔY (change in Y) × MPC, that is, €2 billion × 0.1 = €1 billion.

Einstein Calculating the multiplier

We consider the effect of an increase in investment of €1.5 billion. We can summarize our findings from the multiplier diagram by doing some algebra. To get the multiplier, we can calculate the total increase in production after n + 1 rounds of the process. Each round of the process matches the circular flow diagram. The first-round increase in demand and production is €1.5 billion. The second-round increase in demand and production is (c1 × €1.5 billion), the third-round increase in demand and production is c1 × (c1 × €1.5 billion) = (c12 × €1.5 billion), and so on.

Following this logic, the total increase in demand and production after n + 1 rounds is the total sum of these changes:

Because the marginal propensity to consume is lower than one, we can show that the total sum in the brackets reaches a limit of 1/(1 − c1) as n gets large. This is because the term in the brackets is, mathematically, a geometric series. We show this as follows.

If k is the multiplier, we have:

Now multiply both sides by (1 – c1) to get:

Now divide again by (1 − c1):

As n gets large, assuming c1 < 1, the numerator tends to 1. So, in the limit:

In the example, the marginal propensity to consume is, on average, 0.6. This implies that the multiplier is equal to:

We can then apply the multiplier to the initial change in investment of €1.5 billion to find the sum of all the successive increases in production triggered by the initial hike in investment and aggregate demand: 2.5 × €1.5 billion = €3.75 billion.

14.3 Household target wealth, collateral, and consumption spending

From Unit 13, we know that consumption is the largest component of GDP in most economies. Therefore an important part of understanding changes in output and employment is understanding why consumption changes.

We saw that a shock to investment shifts the aggregate demand curve, and is transmitted through the economy as households adjust their spending in response to changes in income. We focused on incomplete consumption smoothing, such as credit constraints. This behaviour is reflected in the size of the multiplier and the slope of the aggregate demand curve. But consumption and saving behaviour can also shift the aggregate demand curve.

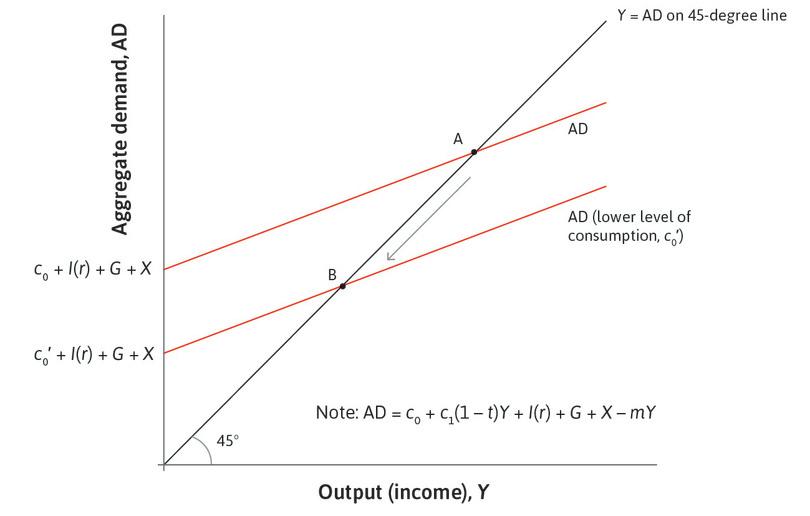

A shift in aggregate demand can be caused by a shift in autonomous consumption, represented by the term c₀ in the aggregate consumption function, C = c₀ + c1Y. A change in c₀ will in turn produce a multiplier response of output and employment through the circular flow of expenditure, output, and income in the same way as the fall in investment in the previous section was multiplied.

- mortgage (or mortgage loan)

- A loan contracted by households and businesses to purchase a property without paying the total value at one time. Over a period of many years, the borrower repays the loan, plus interest. The debt is secured by the property itself, referred to as collateral. See also: collateral.

- precautionary saving

- An increase in saving to restore wealth to its target level. See also: target wealth.

- target wealth

- The level of wealth that a household aims to hold, based on its economic goals (or preferences) and expectations. We assume that households try to maintain this level of wealth in the face of changes in their economic situation, as long as it is possible to do so.

Think about a family with a mortgage on its house. If the price of houses falls, the family will be concerned that its wealth, too, has fallen. A likely reaction to this is for the household to save more. This is called precautionary saving. One way to analyse this behaviour is to assume that households have in mind a target wealth that they aim to hold.

When something happens to affect the stock of the household’s wealth relative to this target, it reacts by either increasing or decreasing its savings to restore wealth back to its target level. If this adjustment involves precautionary saving, it is modelled as a fall in autonomous consumption.

- Great Depression

- The period of a sharp fall in output and employment in many countries in the 1930s.

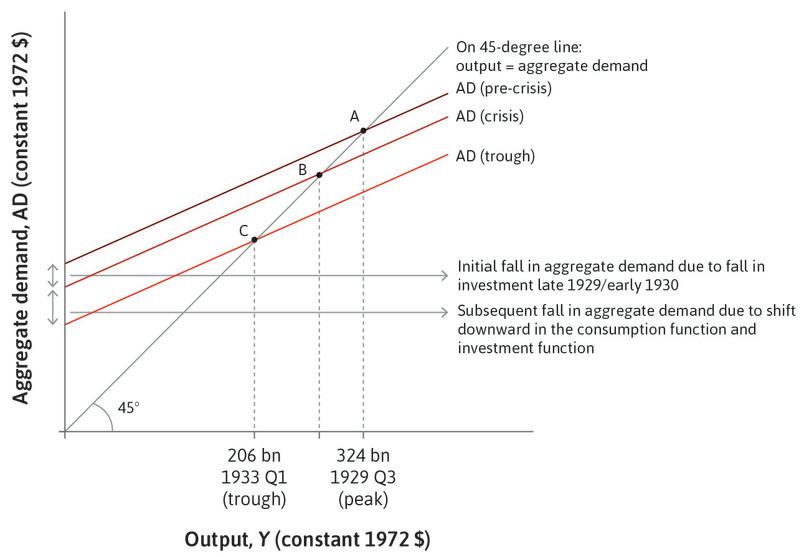

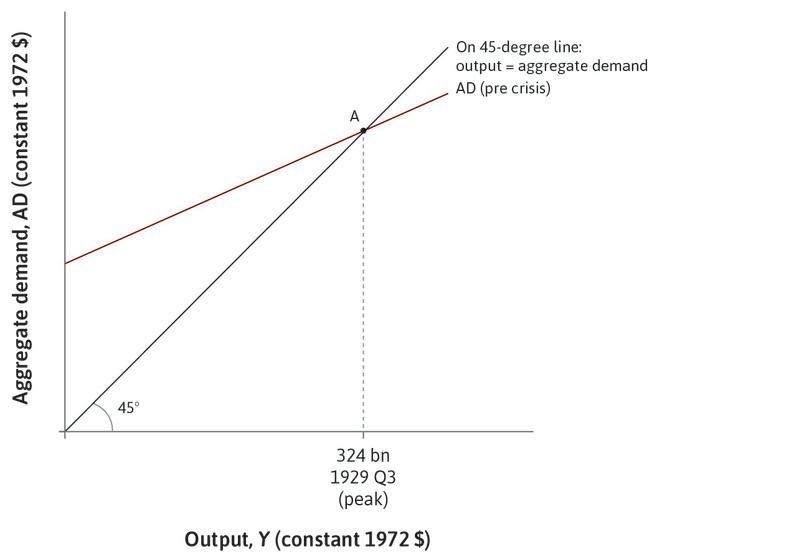

In 1929, a downturn in the US business cycle that initially appeared similar to others in the preceding decade turned into a large-scale economic disaster—the Great Depression.1

The fall in output and employment during the Great Depression highlights two ways in which aggregate consumption might fall—credit constraints in the multiplier process, and changes in wealth relative to target wealth.

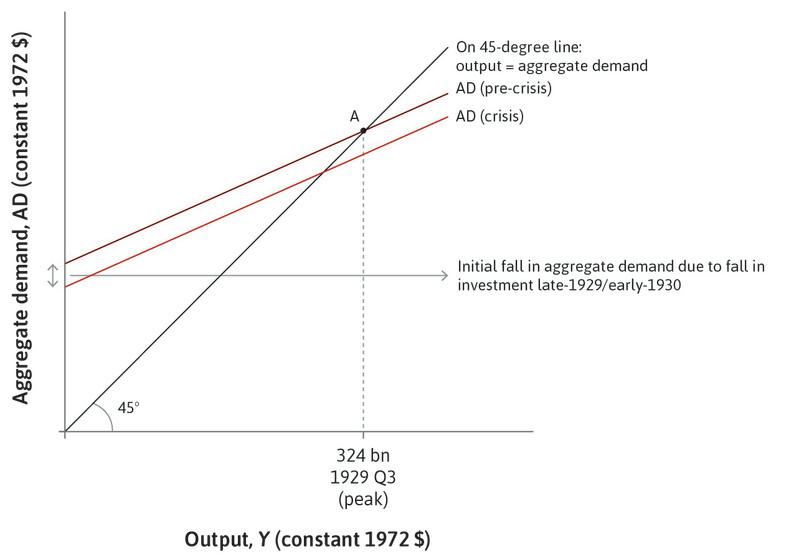

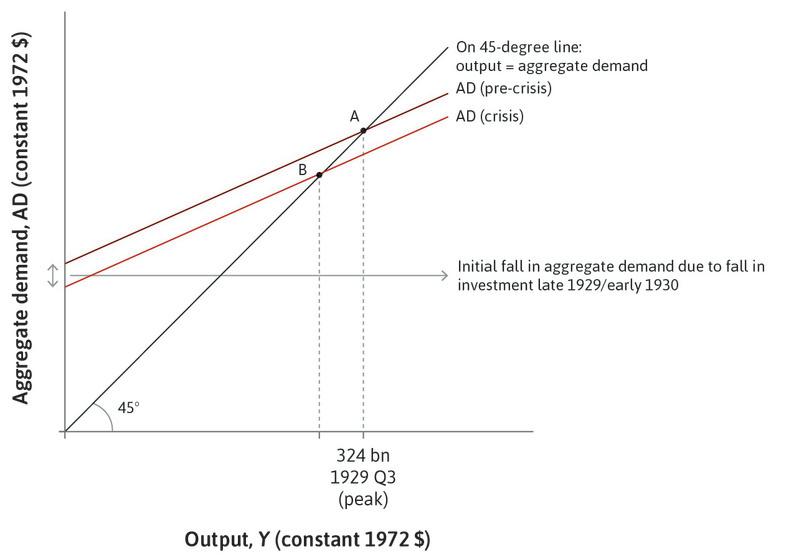

To understand the economic mechanisms at work in the Great Depression, we use the multiplier diagram shown in Figure 14.6. Point A shows the initial situation of the economy in the third quarter of 1929. There was then a fall in investment. This shifts the aggregate demand curve from the pre-crisis to the crisis level. The dotted line from point B shows the level of output that would have been observed in the business cycle trough if the usual multiplier process had been at work. There would have been a recession, but no Great Depression. But the downturn was made much worse because there was a fall in the demand for consumer goods, even by those who kept their jobs.

Aggregate demand in the Great Depression

Figure 14.6 Aggregate demand in the Great Depression

Robert J. Gordon. 1986. The American Business Cycle: Continuity and Change. Chicago, Il: University of Chicago Press.

The 1929 peak

Point A shows the initial situation of the economy.

Figure 14.6a Point A shows the initial situation of the economy.

Robert J. Gordon. 1986. The American Business Cycle: Continuity and Change. Chicago, Il: University of Chicago Press.

A fall in investment

This shifts the aggregate demand curve from the pre-crisis to the crisis level.

Figure 14.6b This shifts the aggregate demand curve from the pre-crisis to the crisis level.

Robert J. Gordon. 1986. The American Business Cycle: Continuity and Change. Chicago, Il: University of Chicago Press.

A normal recession

The economy would normally be at point B.

Figure 14.6c The economy would normally be at point B.

Robert J. Gordon. 1986. The American Business Cycle: Continuity and Change. Chicago, Il: University of Chicago Press.

The 1933 trough

However, instead of a typical downswing (from A to B), output fell by much more than can be explained by the multiplier process alone, which is shown by the move from B to C.

Figure 14.6d However, instead of a typical downswing (from A to B), output fell by much more than can be explained by the multiplier process alone, which is shown by the move from B to C.

Robert J. Gordon. 1986. The American Business Cycle: Continuity and Change. Chicago, Il: University of Chicago Press.

Consumption was cut back through two mechanisms:

- The shift from A to B: As output and employment fell, some households cut spending on housing and consumer durables because they were credit-constrained, and therefore unable to borrow in the deteriorating conditions. Some economists have estimated that the size of the multiplier at the time was about 1.8.

- The shift from B to C: Even households that remained in work cut back spending because it became increasingly clear that the downturn was the new reality, not a temporary shock. This shifted the consumption function down and pulled the economy further into depression from B to C in Figure 14.6.

Research done since the Great Depression (which we examine in more depth in Unit 17) provides a number of explanations for the fall in autonomous consumption in the US:

- Uncertainty: Uncertainty about the state of the economy provoked by the dramatic stock market crash of October 1929 made both firms and households more cautious, prompting them to postpone purchases of machinery and equipment and consumer durables.

- Pessimism and the desire to save more: Households also became more pessimistic about their ability to maintain current levels of spending, as they feared unemployment and lower earnings in the future. Their assessment of their material wealth was also affected as the prices of houses and financial assets fell. The 1920s had seen a build-up of debt by households, as they were able to use instalment agreements for the first time to buy consumer durables.

- The banking crisis and the collapse of credit: A third factor that shifted the aggregate demand line down to the level labelled ‘trough’ was the banking crisis of 1930 and 1931, which affected both consumption and investment. There was a wave of failures of small, weak, and largely unregulated banks across the US. The system of small banks was vulnerable to panic. Savers began to fear that they would not be able to get access to their deposits. As explained in Unit 10, as panic spread from bank to bank, bank runs affected the entire banking system. With the collapse of the banking system, households lost deposits and small firms lost their access to credit.

- human capital

- The stock of knowledge, skills, behavioural attributes, and personal characteristics that determine the labour productivity or labour earnings of an individual. Investment in this through education, training, and socialization can increase the stock, and such investment is one of the sources of economic growth. Part of an individual’s endowments. See also: endowment.

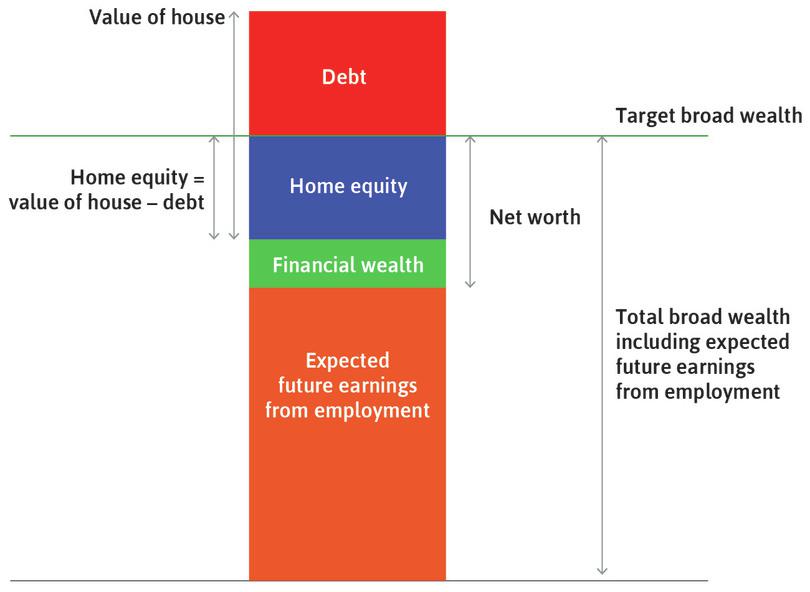

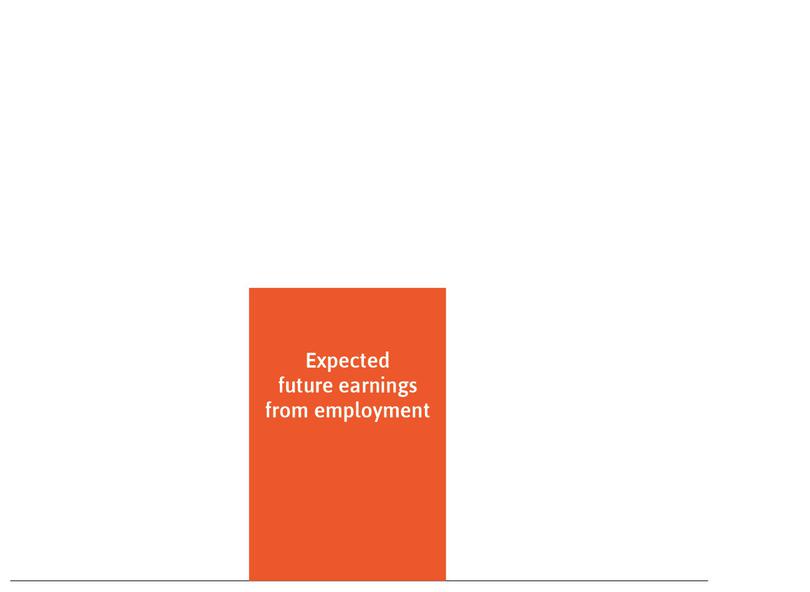

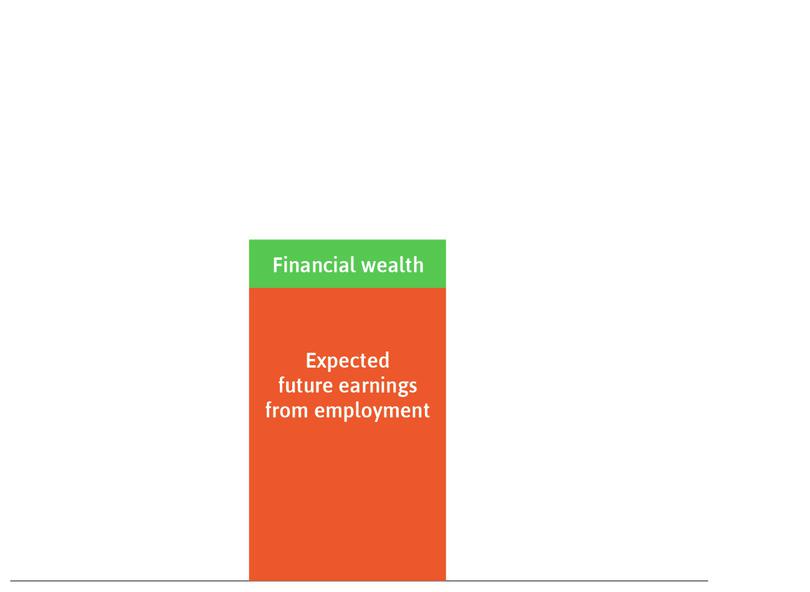

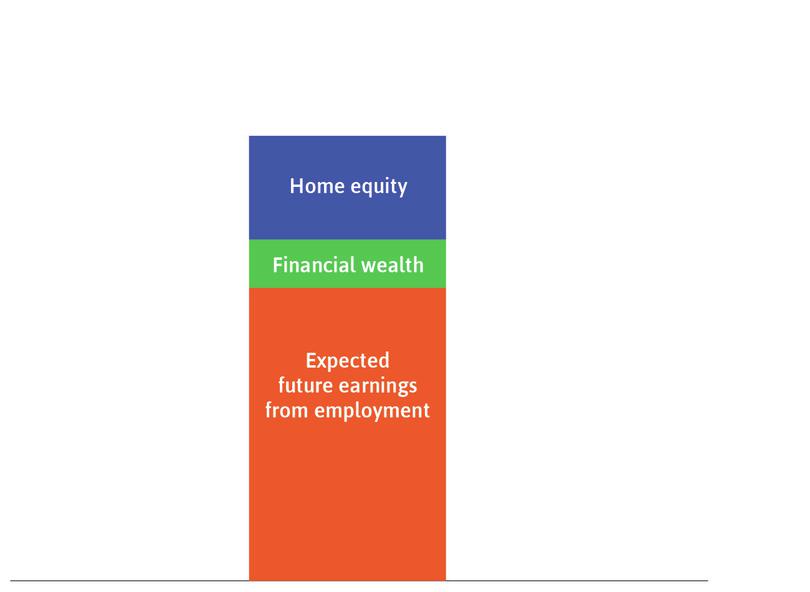

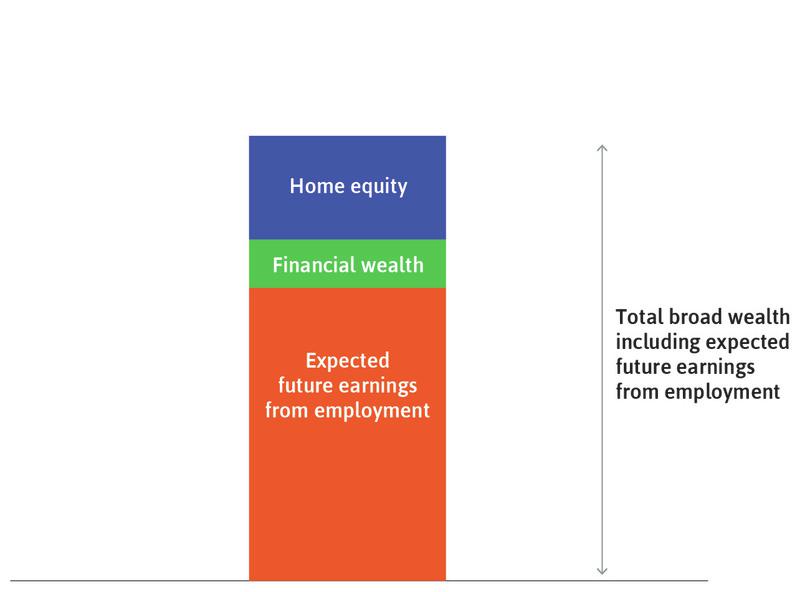

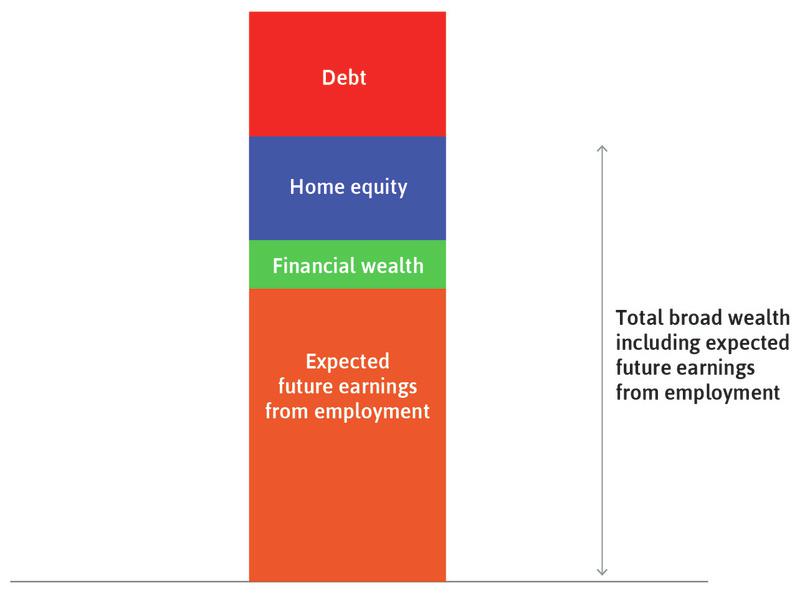

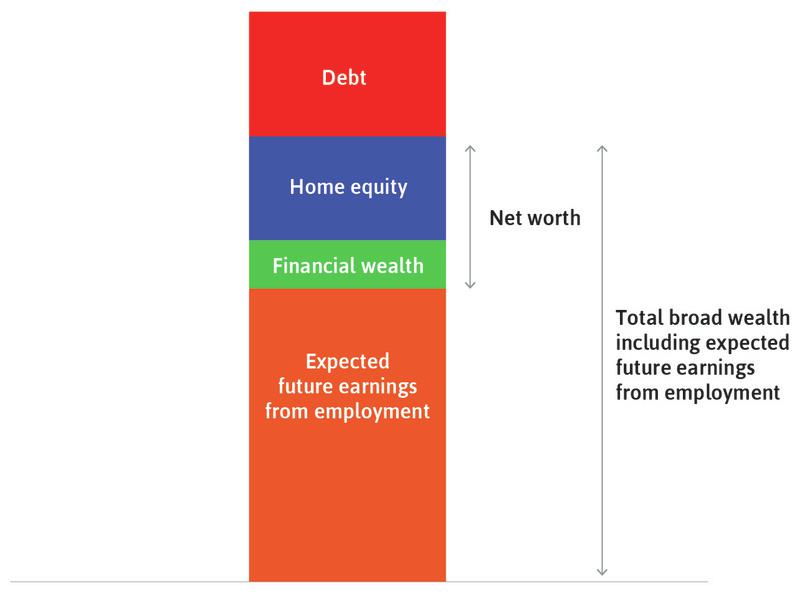

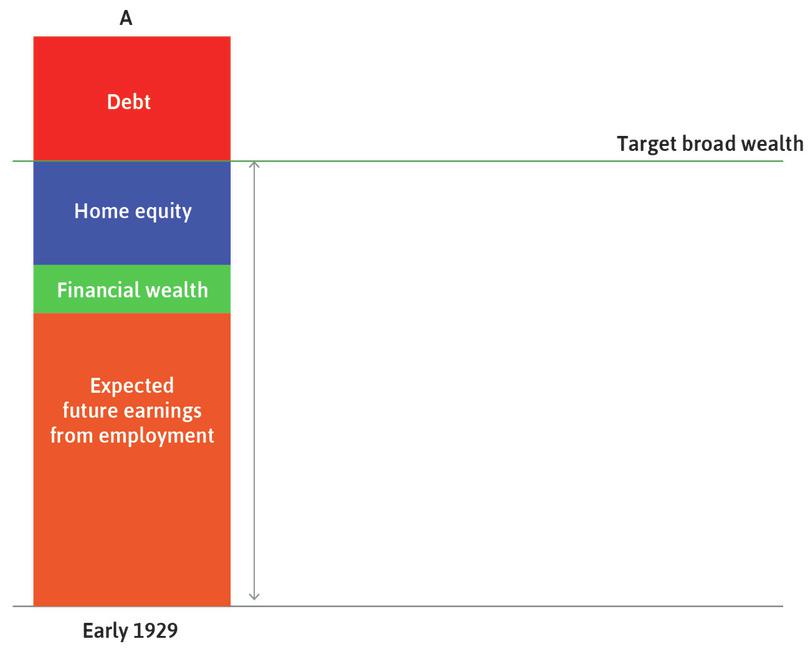

To illustrate why households who were not affected by credit constraints nevertheless cut consumption, we look at the composition of a household’s wealth or assets. In Unit 10 we introduced the concept of wealth by comparing it with the volume of water in a bathtub. At that time we focused on material wealth. In Figure 14.7 we extend the concept of wealth to broad wealth so as to include the household’s expected future earnings from employment, known as the value of its human capital.

Follow the analysis in Figure 14.7 to see the composition of the household’s broad wealth, which is equal to the value of all its assets, minus its debt (which we assume is a mortgage on the house).

- equity

- An individual’s own investment in a project. This is recorded in an individual’s or firm’s balance sheet as net worth. See also: net worth. An entirely different use of the term is synonymous with fairness.

Household wealth: Key concepts.

Figure 14.7 Household wealth: Key concepts.

Expected future earnings from employment

These are represented by the orange rectangle.

Figure 14.7a These are represented by the orange rectangle.

Financial wealth

This is the green rectangle.

Figure 14.7b This is the green rectangle.

The household’s ownership stake in the house

This is the blue rectangle.

Figure 14.7c This is the blue rectangle.

The household’s total broad wealth

This is the sum of the green, blue, and orange rectangles.

Figure 14.7d This is the sum of the green, blue, and orange rectangles.

Households also hold debt

This is shown by the red rectangle.

Figure 14.7e This is shown by the red rectangle.

The household’s net worth

Also called material wealth. We find it by taking the total assets (excluding expected future earnings), which is the value of the house plus financial wealth, and then subtracting the debt it owes.

Figure 14.7f Also called material wealth. We find it by taking the total assets (excluding expected future earnings), which is the value of the house plus financial wealth, and then subtracting the debt it owes.

The value of the house

This is equal to the household’s equity in the house, plus what it owes to the bank (the mortgage).

Figure 14.7g This is equal to the household’s equity in the house, plus what it owes to the bank (the mortgage).

Target wealth

For the household shown in the figure, expected broad wealth (orange + green + blue) is equal to target wealth.

Figure 14.7h For the household shown in the figure, expected broad wealth (orange + green + blue) is equal to target wealth.

As we shall see:

- If target wealth is above expected wealth: The household will increase savings and decrease consumption.

- If target wealth is below expected wealth: The household will decrease savings and increase consumption.

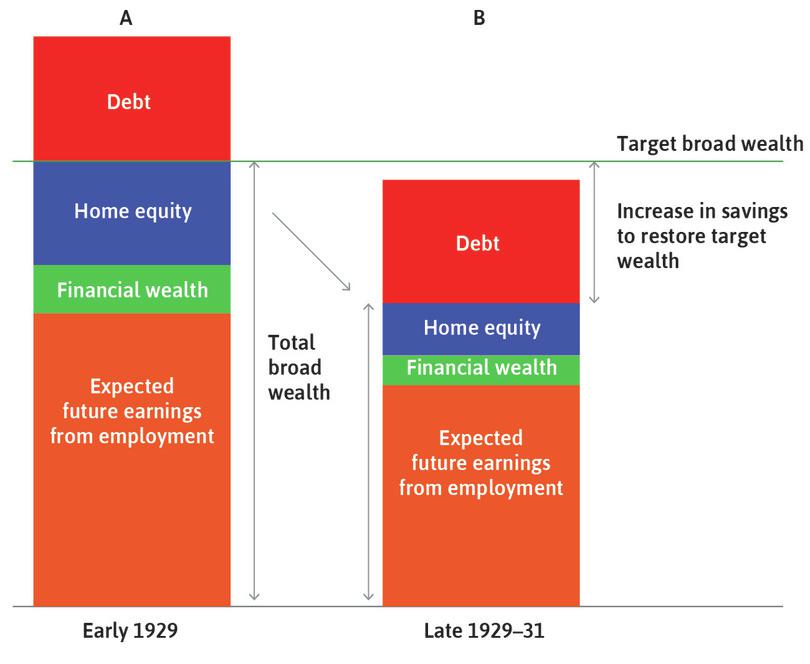

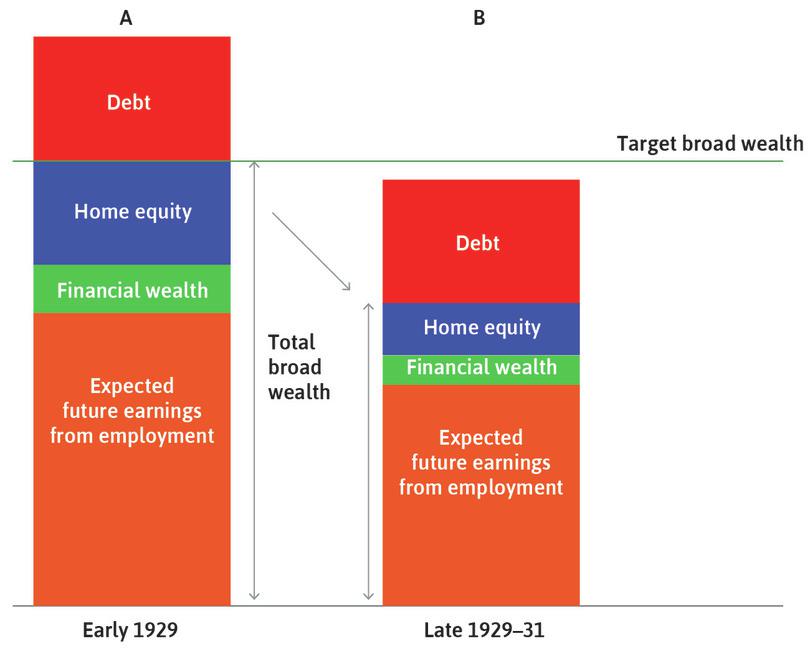

In early 1929, how would a household with the wealth position shown in column A of Figure 14.8 have interpreted news about factory closures, the collapse of the stock market, and bank failures? How would it have adjusted spending on consumer durables, housing, and non-durables? Answers to these questions help tell us why the Great Depression happened.

The Great Depression: Households cut consumption to restore their target broad wealth.

Figure 14.8 The Great Depression: Households cut consumption to restore their target broad wealth.

Before the Depression

Households are making consumption decisions in line with their expectations about their net worth and future earnings from employment. This is shown by the fact that total wealth is equal to target wealth.

Figure 14.8a Households are making consumption decisions in line with their expectations about their net worth and future earnings from employment. This is shown by the fact that total wealth is equal to target wealth.

The Depression

In late 1929, column B, the downturn was underway and beliefs had changed.

Figure 14.8b In late 1929, column B, the downturn was underway and beliefs had changed.

Precautionary saving

The result was a gap between the household’s target wealth and expected wealth. Households increased their savings.

Figure 14.8c The result was a gap between the household’s target wealth and expected wealth. Households increased their savings.

- financial accelerator

- The mechanism through which firms’ and households’ ability to borrow increases when the value of the collateral they have pledged to the lender (often a bank) goes up.

- Before the Depression: Viewed from early in 1929 (column A in Figure 14.8), households are shown as making consumption decisions in line with their expectations: total wealth is equal to target wealth.

- The Depression: By late 1929 (column B), the downturn was underway and beliefs had changed. With job losses throughout the economy, households revised expected earnings downward. Falling asset prices (of shares and houses) reduced the value of the household’s material wealth. The result was a gap between the household’s target wealth and expected wealth. This helps to explain the cutback in consumption by households who could (and in an ordinary downturn, would) have helped to smooth a temporary fall in aggregate demand. Instead, these households increased their saving. This fall in autonomous consumption is part of the explanation for the downward shift of the aggregate demand curve from crisis to trough in Figure 14.6.

- The financial accelerator, collateral, and credit constraints: Changes in household wealth affect consumption through another channel. In Unit 10, we saw that having collateral may enable a household to borrow. An important example is the case of home loans, where the bank extends a loan using the value of the house as collateral. If the value of your house falls, the bank will be willing to lend less, making you more credit-constrained, which may reduce your consumption.

The same mechanisms are at work if house prices increase, which will tend to increase consumption:

- For those who are not credit-constrained: If the value of your house increases, this improves your net worth and raises your wealth relative to target. We would predict that this would reduce your precautionary savings, increasing consumption.

- For those who are credit-constrained: A rise in the price of your house can lead you to increase your consumption spending because the higher collateral enables you to borrow more.

Exercise 14.1 A household’s balance sheet

Consider a family of two parents and two children who have a mortgage on their home. They have paid off half the mortgage. The family also owns a car and a portfolio of shares in companies. They spend their income on food, clothing, and private school fees, and have retirement savings held in a pension fund.

- Which of these items would be on a balance sheet for the household?

- Using the example of the bank’s balance sheet in Figure 10.16 as a guide, construct an annual balance sheet for your hypothetical household. You may want to research the typical values for these items for a family of this type.

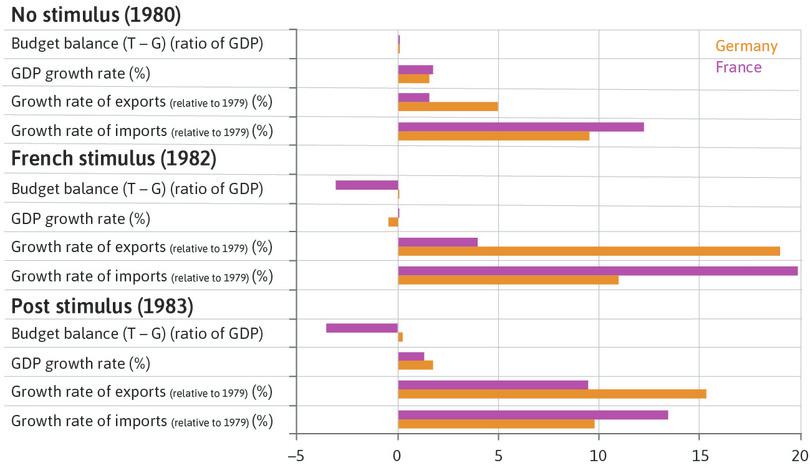

Exercise 14.2 Housing in France and Germany

In France and Germany, it is difficult for a household to increase its borrowing based on an increase in the market value of the house. In addition, large down-payments (as a percentage of the house price) are required for house purchases.

- On the basis of this information, how would you expect a rise in house prices in France or Germany to affect spending by households?

- In the US or UK, loans are more easily available based on a rise in home equity and only a small down-payment is required. How would you expect your answer to question 1 to change when considering the US or UK?

- What do you conclude about the role of the financial accelerator in France and Germany compared with the UK and the US?

Note: A December 2014 VoxEU article, ‘Combatting Eurozone deflation: QE for the people’, tells you more about the influence of a change in house prices on spending in Europe and the US.

Question 14.3 Choose the correct answer(s)

Which of the following statements is correct regarding household wealth?

- The material wealth is the net worth, that is, financial wealth plus value of house minus its debt.

- This is the definition of broad wealth.

- A household adjusts its precautionary saving in response to the gap (positive or negative) between its actual and target wealth.

- If the target wealth is above its expected wealth, then the household will increase its savings to fill the gap, reducing its consumption as a result.

14.4 Investment spending

In Unit 13, we contrasted the volatility of investment with the smoothness of consumption spending. But how do firms make investment decisions? Think of the manager or owner of a firm deciding what to do with their accumulated profits. There are four choices:

- Dividends: Allocate the funds to managerial or employee salaries, or to dividends for owners.

- Saving: Buy an interest-bearing financial asset such as a bond, or retire (pay off) existing debt.

- Investment abroad: Build new productive capacity in another country.

- Investment at home: Build new capacity in the home country.

The fourth choice is called investment in our model (the third choice is also investment, but since it is spent in the foreign country it is measured in the foreign country’s national accounts as part of its I, not in the home country’s).

If we assume that there is no reason to change salaries then we can also break down the owner’s decision as we did Marco’s decision in Unit 10:

- The owner has the choice to consume now or consume later: Taking the revenue as dividends means the owner can, if desired, simply consume the extra income now.

- If the decision is to consume later: The owner can either save (lend by buying a financial asset such as a bond or retire debt) or invest in a new project.

- If the decision is to invest: Whether the owner does it in the home country or abroad will depend on the expected rate of profit for the potential investment projects in the two locations.

The desirability of consuming more now rather than later depends on the owner’s discount rate (ρ), as discussed in Unit 10. The owner will compare this to the return they can get by not consuming now. If the firm saves by buying a financial asset then the return is the interest rate r. If the firm invests in productive capacity then the return will be the profit rate on investment, which we will call Π as in Unit 10:

- If ρ is greater than both r and Π: The owner will keep the funds and increase consumption spending.

- If r is greater than ρ and Π: The decision will be to repay debt or purchase a financial asset.

- If Π is greater than ρ and r: The owner will invest (either at home or abroad).

- monetary policy

- Central bank (or government) actions aimed at influencing economic activity through changing interest rates or the prices of financial assets. See also: quantitative easing.

Because of these options, the interest rate is one of the factors determining whether investment takes place. We saw in Unit 10 that this can be altered by central bank policy (monetary policy). The interest rate is the opportunity cost of purchases of machinery, equipment, and structures that increase the capital stock—if you have money available, you could save it with a return of r instead of investing it. Alternatively, if you do not have money available, then the cost of borrowing for investment is also r. If we rank investment projects by their expected post-tax rate of profit, then a lower interest rate raises the number of projects for which the expected rate of profit is greater than the interest rate. We saw this when Marco faced the decision of whether or not to invest (Figure 10.10). Thus a higher interest rate reduces investment, and a lower interest rate increases it.

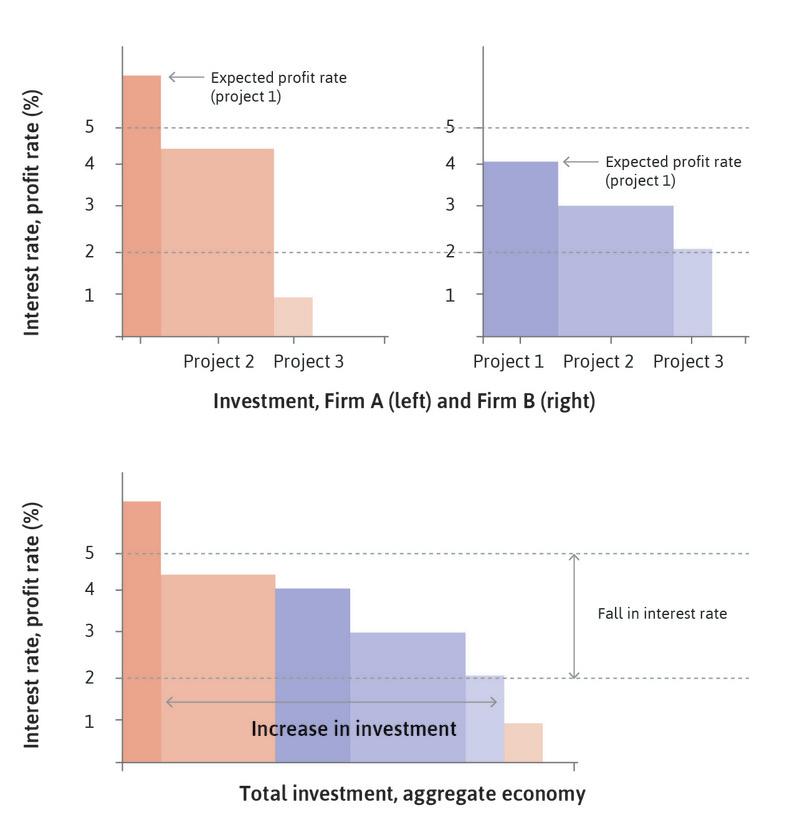

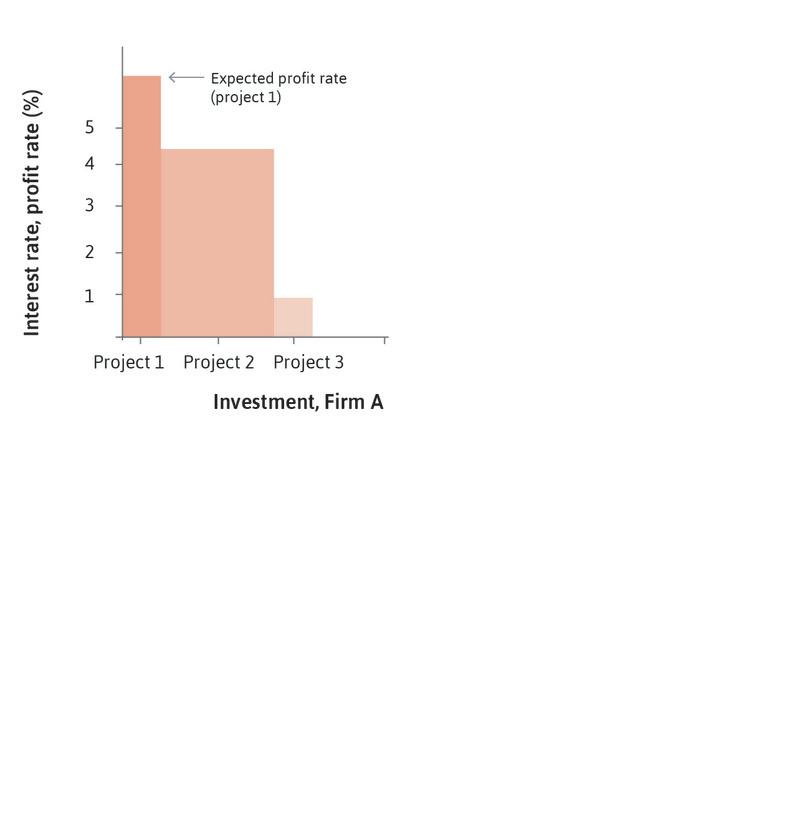

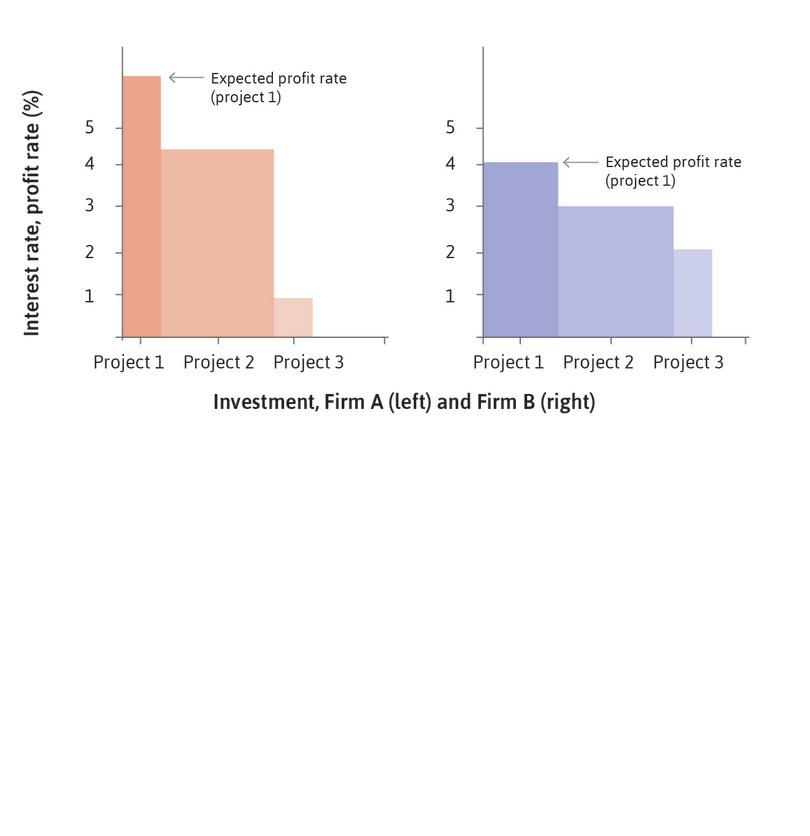

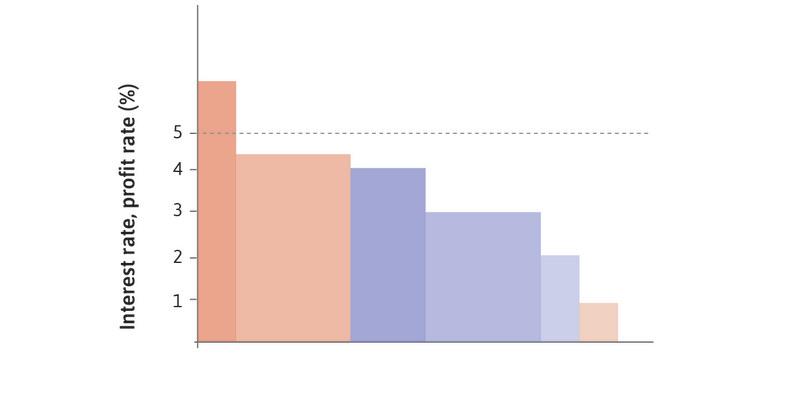

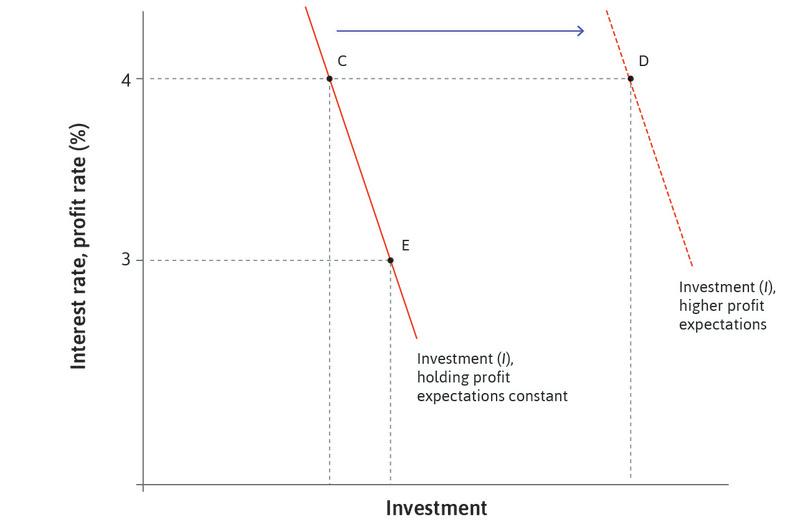

Figure 14.9 illustrates this fact for an economy consisting of two firms, A and B. For each firm in this example, there are three investment projects of different scale and rate of return. They are shown in decreasing order of the expected rate of profit. Follow the analysis in Figure 14.9 to see how the interest rate determines which investment projects go ahead. The lower panel aggregates the two firms to show how investment in the economy as a whole responds to a change in the interest rate.

Investment, expected rate of profit, and the interest rate in an economy with two firms.

Figure 14.9 Investment, expected rate of profit, and the interest rate in an economy with two firms.

Firm A

Firm A has three investment projects of different scale and rate of profit. They are shown in decreasing order of the expected rate of profit.

Figure 14.9a Firm A has three investment projects of different scale and rate of profit. They are shown in decreasing order of the expected rate of profit.

Firm B

Firm B also has three different investment projects.

Figure 14.9b Firm B also has three different investment projects.

The decision to invest

If the interest rate remains at 5%, Firm A goes ahead with project 1 and Firm B does not invest at all. But if the interest rate was 2%, A would undertake projects 1 and 2 and B would undertake all three of its projects.

Figure 14.9c If the interest rate remains at 5%, Firm A goes ahead with project 1 and Firm B does not invest at all. But if the interest rate was 2%, A would undertake projects 1 and 2 and B would undertake all three of its projects.

The decision to invest

The lower panel aggregates the potential investments of the two firms, arranged by the expected profit rate as before.

Figure 14.9d The lower panel aggregates the potential investments of the two firms, arranged by the expected profit rate as before.

Aggregate investment increases

Investment in the economy increases after a fall in the interest rate. Five projects go ahead, instead of just one.

Figure 14.9e Investment in the economy increases after a fall in the interest rate. Five projects go ahead, instead of just one.

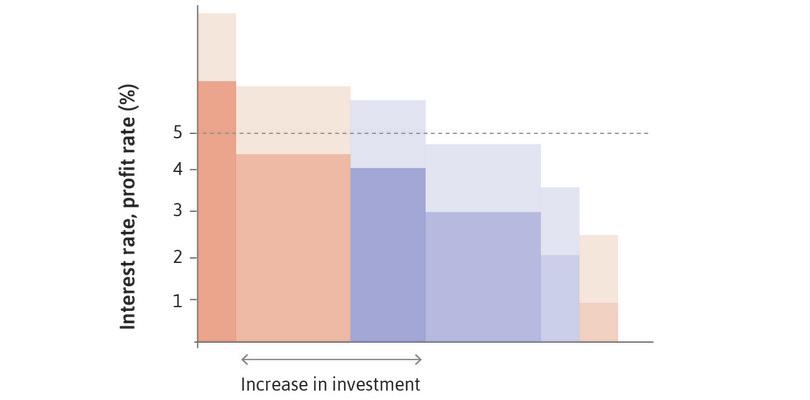

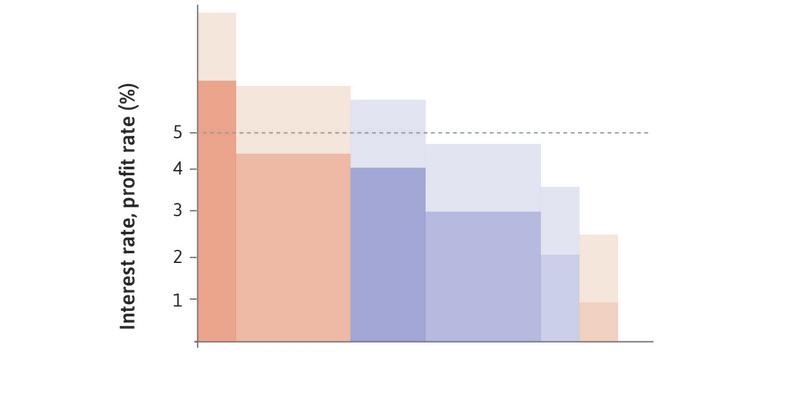

In Figures 14.10a–c, we look at how a change in profit expectations affects investment.

In the two-firm economy in Figure 14.10a, the expected rate of profit for each project rises because of an improvement in the supply-side conditions in the economy. The height of each column rises, and as a result, there is more investment at a given interest rate.

The aggregate economy, where the expected rate of profit rises for a given set of projects (supply effect).

Figure 14.10a The aggregate economy, where the expected rate of profit rises for a given set of projects (supply effect).

Interest rate at 5%

With the interest rate equal to 5%, only one project will go ahead.

Figure 14.10aa With the interest rate equal to 5%, only one project will go ahead.

Improvement in supply conditions

The improvement in supply conditions increases the expected rate of profit for each project.

Figure 14.10ab The improvement in supply conditions increases the expected rate of profit for each project.

Effect on investment

For the same interest rate, investment rises: two more projects go ahead.

Figure 14.10ac For the same interest rate, investment rises: two more projects go ahead.

An upward shift can be caused by a fall in expected input prices, such as a forecast fall in the price of energy or wages, or a fall in taxation over the life of the project.

- expropriation risk

- The probability that an asset will be taken from its owner by the government or some other actor.

Another example of a positive supply effect is an improvement in the security of property rights so that there is a smaller chance that the government or another powerful actor (such as a landowner, like Bruno in Unit 5, who might threaten a smallholder) will take over ownership of the investment project. This is called a fall in the risk of expropriation and is an example of an improvement in the business environment.

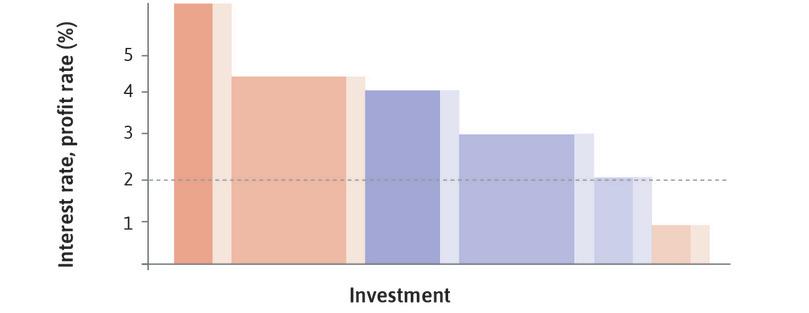

In Figure 14.10b, the height of the columns remains unchanged, but their width (representing the amount of investment that is profitable in many projects) has increased. This is the result of a permanent increase in demand and the lack of sufficient capacity to meet forecast sales.

The aggregate economy, where the desired capacity rises for each project (demand effect).

Figure 14.10b The aggregate economy, where the desired capacity rises for each project (demand effect).

Interest rate at 2%

With the interest rate equal to 2%, and the initial desired capacity, investment is shown by the darker coloured blocks.

Figure 14.10ba With the interest rate equal to 2%, and the initial desired capacity, investment is shown by the darker coloured blocks.

Higher forecast demand

Pressure on existing capacity from higher forecast demand raises the desired size of each project, so investment rises to include the lighter coloured blocks.

Figure 14.10bb Pressure on existing capacity from higher forecast demand raises the desired size of each project, so investment rises to include the lighter coloured blocks.

- investment function (aggregate)

- An equation that shows how investment spending in the economy as a whole depends on other variables, namely, the interest rate and profit expectations. See also: interest rate, profit.

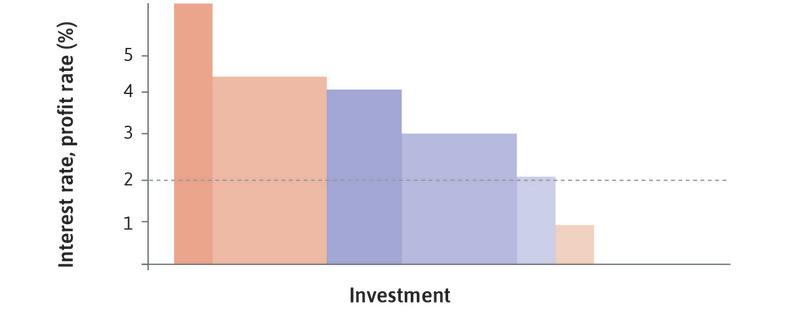

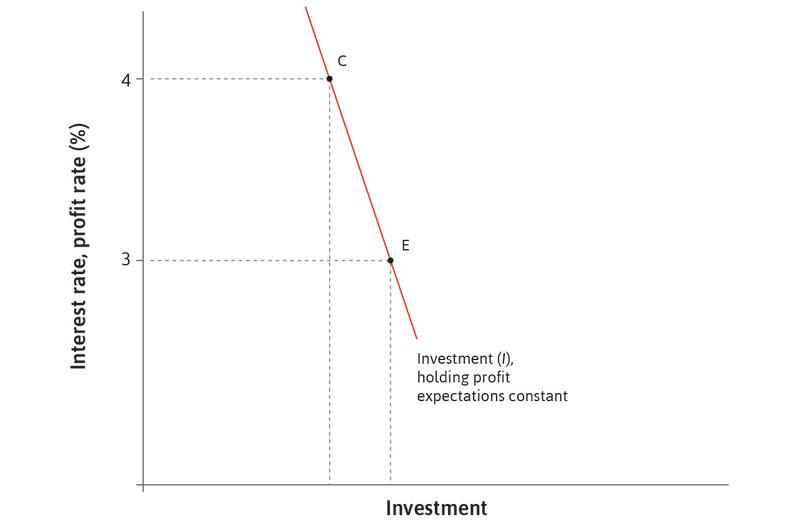

In an economy with many thousands of firms, a downward-sloping line (as in Figure 14.10c) represents the potential investment projects. This is called the aggregate investment function. The response of investment to a change in the interest rate is shown as a shift from C to E. Figure 14.10c also shows the effect of a change in the profitability of investment, which arises from supply and demand effects and raises investment from C to D for the same interest rate.

Aggregate investment function: Effects of the interest rate and profit expectations.

Figure 14.10c Aggregate investment function: Effects of the interest rate and profit expectations.

Potential investment projects

In an economy with many thousands of firms, all their potential investment projects are represented by a downward-sloping aggregate investment function.

Figure 14.10ca In an economy with many thousands of firms, all their potential investment projects are represented by a downward-sloping aggregate investment function.

Investment increases

In response to a fall in the interest rate, investment increases from C to E.

Figure 14.10cb In response to a fall in the interest rate, investment increases from C to E.

An increase in profit expectations

This shifts the investment function to the right: if the interest rate is held constant at 4%, investment increases from C to D.

Figure 14.10cc This shifts the investment function to the right: if the interest rate is held constant at 4%, investment increases from C to D.

The empirical evidence suggests that business spending on machinery and equipment is not very sensitive to the interest rate. The limited effect of changes in the interest rate on business investment (illustrated by the steepness of the lines in the figure) highlights the importance of the supply- and demand-side factors that shift the investment function (Figures 14.10a and 14.10b).

The interest rate affects investment spending outside the business sector through its effects on households’ decisions to purchase new or larger homes, which influence new housing construction. The interest rate also has substantial effects on the demand for durable consumer goods, such as cars and home appliances, which are often purchased using credit.

Question 14.4 Choose the correct answer(s)

Figure 14.9 depicts possible investment projects for Firms A and B.

Based on this information, which of the following statements is correct?

- For Firm B, the expected profit rate from its project 1 is less than 5%. Therefore only Firm A undertakes its project 1.

- At an interest rate of 1.5%, Firm A will not undertake project 3.

- With a permanent positive demand shock, the heights of the columns remain unchanged but the amount of investment that is profitable increases. This increases the widths of the columns, leading to higher investment (for any given interest rate).

- The fall in energy prices reduces costs for firms so expected profits increase, implying that more projects have an expected profit rate greater than the interest rate.

Question 14.5 Choose the correct answer(s)

Figure 14.10c depicts the aggregate investment function of an economy.

Based on this information, which of the following statements is correct?

- The investment line represents the relationship between investment and interest rate, ceteris paribus. Therefore the fall in investment would be shown by a movement up the original line (from E to C for example), not a shift of the line.

- A rise in corporate tax would decrease the expected profit rate, shifting the investment line inwards. This results in a fall in investment.

- Higher demand makes it profitable to invest in larger projects, increasing investment at a given interest rate.

- A steeper line means smaller changes in investment when the interest rate moves, that is, lower sensitivity of investment to the interest rate.

14.5 The multiplier model: Including the government and net exports

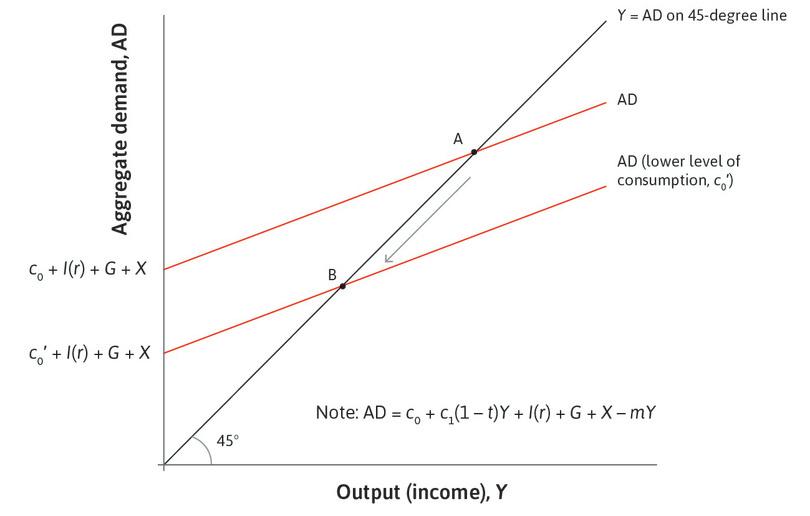

Here we add governments and central banks to the model so that we can show how they can stabilize (or destabilize) the economy after a shock. As before, we assume that firms are willing to supply any amount of goods demanded, so:

We saw in Unit 13 that when we include the government and interactions with the rest of the world through exports and imports, aggregate demand can be split into these components:

To understand the aggregate demand function as shown above, it is useful to go through each component in turn:

Consumption

Household consumption spending depends on post-tax income. The government charges a tax t, which we assume is proportional to income. The income left after the payment of tax, (1 − t)Y, is called disposable income. The marginal propensity to consume, c1, is the fraction of disposable income (not pre-tax income) consumed. This means that in the aggregate consumption function:

- Spending on consumption is written as: C = c₀ + c1(1 − t)Y.

- All of the influences on consumption apart from current disposable income are included in autonomous consumption, c₀, and will therefore shift the consumption function in the multiplier diagram. These include wealth and target wealth, collateral effects, and changes in the interest rate.

Investment

We have just seen that investment spending will be influenced by the interest rate and the expected post-tax rate of profit. In the aggregate investment function:

- Spending on investment is a function of the interest rate and the expected post-tax rate of profit.

- Ceteris paribus, a higher interest rate reduces investment spending, shifting down the aggregate demand curve.

- A higher expected post-tax rate of profit raises investment spending, shifting up the aggregate demand curve.

Government spending

- exogenous

- Coming from outside the model rather than being produced by the workings of the model itself. See also: endogenous.

Much of government spending (excluding transfers) is on general public services, health, and education. Government spending does not change in a systematic way with changes in income. It is referred to as exogenous.

An increase in government spending shifts the aggregate demand curve up in the multiplier diagram.

Net exports

- marginal propensity to import

- The change in total imports associated with a change in total income.

The home economy sells goods and services abroad, which are its exports. The amount of foreign goods the home economy demands (its imports) will depend on domestic incomes. The fraction of each additional unit of income that is spent on imports is termed the marginal propensity to import (m), which must be between 0 and 1. So we have:

- exchange rate

- The number of units of home currency that can be exchanged for one unit of foreign currency. For example, the number of Australian dollars (AUD) needed to buy one US dollar (USD) is defined as number of AUD per USD. An increase in this rate is a depreciation of the AUD and a decrease is an appreciation of the AUD.

If a country’s costs of production fall so that it can sell its goods at a lower price on world markets compared to the prices of other countries, the demand for its exports will increase, and domestic demand for imports will fall. We will see in the next unit that the exchange rate affects the prices of a country’s goods on world markets. Growth in world markets also increases exports. For now, however, we will ignore these effects and assume that exports are also exogenous.

Putting together each of the components of aggregate demand we have:

Both taxes and imports reduce the size of the multiplier. Recall that the multiplier tells us the amount by which an increase in spending (such as a rise in autonomous consumption, investment, government spending, or exports) raises GDP in the economy. When we include taxation and imports in the model, the indirect multiplier effect of a given rise in spending on GDP is smaller. This is because some household income goes straight to the government as taxation, and some is used to buy goods and services produced abroad. Because we assume that the government does not increase its spending when taxes go up, and foreign buyers do not import more of our goods when we import more of theirs, this means that some of an autonomous increase in income does not lead to further indirect increases in income in the domestic economy. Like saving, taxation and imports are referred to as leakages from the circular flow of income. The result is to reduce the indirect effects of an autonomous change in spending on aggregate demand, output, and employment.

To summarize:

- A higher marginal propensity to import reduces the size of the multiplier: This makes the aggregate demand curve flatter.

- An increase in exports shifts the aggregate demand curve up in the multiplier diagram.

- An increase in the tax rate reduces the size of the multiplier: This makes the aggregate demand curve flatter.

The Einstein at the end of this section shows you how to calculate the size of the multiplier in the model once the tax rate and imports are included. To illustrate, we assume a tax rate of 20% (0.2) and a marginal propensity to import of 0.1. Before we introduced the government, we set the marginal propensity to consume, c1, at 0.6. If we use these numbers in the formula for the multiplier that we calculate in the Einstein, we get the result that the value of the multiplier is k = 1.6, compared to 2.5 without including taxation and imports. In the next section we look at how economists have estimated the size of the multiplier from data, why their estimates differ, and why it matters.

Exercise 14.3 The multiplier model

Consider the multiplier model discussed above.

- Compare two economies, which differ only in their share of credit-constrained households but are identical otherwise. In which economy is the multiplier larger? Illustrate your answer using a diagram.

- On the basis of your comparison of the two economies, would you expect the multiplier in an economy to vary over its business cycle?

- Some economists estimated the size of the multiplier in the Great Depression to be equal to 1.8. Explain how the following characteristics of the US economy at the time could have affected its value:

- the size of government (see Figure 14.1)

- the fact that there were no unemployment benefits

- the fact that the share of imports was small

Question 14.6 Choose the correct answer(s)

The aggregate demand of an open economy is given by the after-tax domestic consumption C, the investment I (which depends on the interest rate r), the government spending G and net exports X − M:

c₀ is autonomous consumption, c₁ is the marginal propensity to consume, and m is the marginal propensity to import. In the economy’s equilibrium this equals its output: AD = Y. Solving for Y yields:

Given this equation, which of the following increases the multiplier?

- G affects the level of AD but not the multiplier.

- r affects I(r), which in turn affects the level of AD but not the multiplier.

- A fall in m increases the multiplier. This is because it reduces leakages in the economy.

- A rise in t reduces the multiplier.

Einstein The multiplier in an economy with a government and foreign trade

We can again use the fact that there is equilibrium in the goods market when output is equal to aggregate demand to find the multiplier (equilibrium is where the aggregate demand line crosses the 45-degree line in the multiplier diagram). The aggregate demand equation can be rearranged to solve for output and consequently the multiplier:

Therefore:

We can see that the multiplier is smaller when we introduce the government and foreign trade:

The reason is that the denominator on the left-hand side is larger than on the right:

14.6 Fiscal policy: How governments can dampen and amplify fluctuations

There are three main ways that government spending and taxation can dampen fluctuations in the economy:

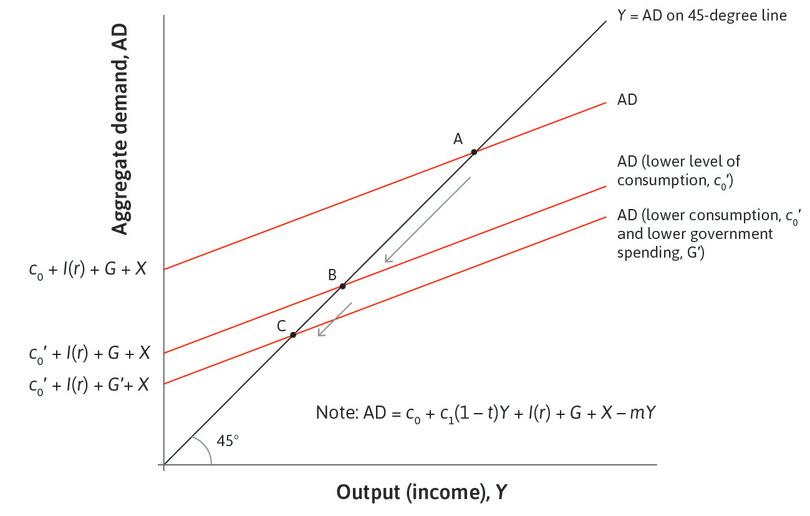

- The size of government: Unlike private investment, government spending on consumption and investment is usually stable. Spending on health and education, which are the two largest government budget items in most countries, does not fluctuate with capacity utilization or with business confidence. These kinds of government spending stabilize the economy. As we have also seen, a higher tax rate dampens fluctuations because it reduces the size of the multiplier.

- The government provides unemployment benefits: Although households save to smooth fluctuations in income, few households save enough (that is, self-insure) to cope with an extended period of unemployment. So unemployment benefits help households to smooth consumption. Other programs to redistribute income to the poor have the same smoothing effect.

- The government can intervene: It can intervene deliberately to stabilize aggregate demand using fiscal policy.

- fiscal policy

- Changes in taxes or government spending in order to stabilize the economy. See also: fiscal stimulus, fiscal multiplier, aggregate demand.

- co-insurance

- A means of pooling savings across households in order for a household to be able to maintain consumption when it experiences a temporary fall in income or the need for greater expenditure.

- hidden actions (problem of)

- This occurs when some action taken by one party to an exchange is not known or cannot be verified by the other. For example, the employer cannot know (or cannot verify) how hard the worker she has employed is actually working. Also known as: moral hazard. See also: hidden attributes (problem of).

Could workers insure privately against job loss? There are also three reasons why the private market fails, and therefore governments provide unemployment insurance in the form of unemployment benefits:

- Correlated risk: In a recession, job loss will be widespread. This means that there will be a surge in insurance claims across the economy and a private provider may be unable to pay out on the scale required. It also means co-insurance among a group of neighbours or family members may be of limited use, as the need for help may arise in many households at the same time.

- Hidden actions: As we saw in Unit 12, the insurance company cannot observe the reason for the job loss so it would have to insure the employee against a firm cutting back employment due to lack of demand, as well as the worker being fired for inadequate work. This creates a moral hazard, because a well-insured person is expected to make less of an effort on the job.

- Hidden attributes: Suppose you learn that your firm is in difficulty, but the insurance company does not. This is another example of asymmetric information. You will therefore buy insurance when you learn of the likely closure of the firm, and it will be provided at good rates because the insurance company does not know that you are likely to make a claim on them. Workers who know their firm is performing well will not buy insurance. The hidden attributes problem will be true about individuals (hardworking or lazy), as well as firms (successful or failing). The good prospects (those who enjoy working hard, for example) will shun the insurance and the insurer will be left with those likely to face the extra risks of losing their job.

The system of unemployment benefits is part of the automatic stabilization that characterizes modern economies. We have already seen another automatic stabilizer: a proportional tax system reduces the size of the multiplier and dampens the business cycle.

- moral hazard

- This term originated in the insurance industry to express the problem that insurers face, namely, the person with home insurance may take less care to avoid fires or other damages to his home, thereby increasing the risk above what it would be in absence of insurance. This term now refers to any situation in which one party to an interaction is deciding on an action that affects the profits or wellbeing of the other but which the affected party cannot control by means of a contract, often because the affected party does not have adequate information on the action. It is also referred to as the ‘hidden actions’ problem. See also: hidden actions (problems of), incomplete contract, too big to fail.

- hidden attributes (problem of)

- This occurs when some attribute of the person engaging in an exchange (or the product or service being provided) is not known to the other parties. An example is that the individual purchasing health insurance knows her own health status, but the insurance company does not. Also known as: adverse selection. See also: hidden actions (problem of).

- asymmetric information

- Information that is relevant to the parties in an economic interaction, but is known by some but not by others. See also: adverse selection, moral hazard.

- automatic stabilizers

- Characteristics of the tax and transfer system in an economy that have the effect of offsetting an expansion or contraction of the economy. An example is the unemployment benefits system.

- paradox of thrift

- If a single individual consumes less, her savings will increase; but if everyone consumes less, the result may be lower rather than higher savings overall. The attempt to increase saving is thwarted if an increase in the saving rate is unmatched by an increase in investment (or other source of aggregate demand such as government spending on goods and services). The outcome is a reduction in aggregate demand and lower output so that actual levels of saving do not increase.

- fallacy of composition

- Mistaken inference that what is true of the parts (for example a household) must be true of the whole (in this case the economy as a whole). See also: paradox of thrift.

In our list, the third role of government in dampening fluctuations is the use of fiscal policy in deliberate stabilization policies: an increase in government spending or cuts in taxation to support aggregate demand in a downturn; or trimming spending and raising taxes to rein in a boom. It can be cumbersome to have these fiscal policy measures approved by a parliament, which has power over budgetary decisions, which is one reason why stabilization policy is often handled through monetary, rather than fiscal, policy. But fiscal policy can also play an important role in stabilization, as we now consider, especially in particularly large downturns.

The paradox of thrift and the fallacy of composition

By comparing a household with the economy as a whole, we better understand the nature of an increase in the government’s deficit in a recession. Faced with a household budget deficit, a family worried about their falling wealth cuts spending and saves more. We saw exactly this behaviour in Figure 14.8 when households increased their savings in 1929. Keynes showed that the wisdom of family precautionary saving does not apply to the government when the economy is in a recession.

Compare the attempt to save more by a single household and by all households in the economy simultaneously. Think of a single household cutting expenditures and putting its additional savings in a sock. The money is in the sock for when the household decides it is wise to spend it.

Now, assume that all households cut expenditures and put additional savings in their socks. Assuming nothing else in the economy changes, the additional saving causes lower aggregate consumption spending in the economy. What happens? From the previous section, we can model this as a fall in autonomous consumption, c₀: the aggregate demand curve shifts down. The economy moves through the multiplier process to a lower level of output, income, and employment. The aggregate attempt to increase savings led to a fall in aggregate income, which is known as the paradox of thrift. The fact that what is true for one part of the economy is not true of the whole economy is known as the fallacy of composition.

A single household can increase its savings if it anticipates bad luck, and the saving will be there if it is unlucky—for example, if someone becomes ill or loses a job. However, if every household does this when the economy is in a recession, this behaviour causes the bad luck: more people lose their jobs. The reason is that in the economy as a whole, spending and earning go together. My spending is your income. Your spending is my income.